المجلة: Maritime Economics & Logistics، المجلد: 26، العدد: 1

DOI: https://doi.org/10.1057/s41278-024-00287-z

تاريخ النشر: 2024-02-20

DOI: https://doi.org/10.1057/s41278-024-00287-z

تاريخ النشر: 2024-02-20

أزمة البحر الأحمر: التداعيات على عمليات السفن، شبكات الشحن، وسلاسل الإمداد البحرية

تم القبول: 14 فبراير 2024 / تم النشر على الإنترنت: 20 فبراير 2024

© المؤلفون، بموجب ترخيص حصري لشركة سبرينجر ناتشر المحدودة 2024

© المؤلفون، بموجب ترخيص حصري لشركة سبرينجر ناتشر المحدودة 2024

1 المقدمة

لقد تصدرت أخبار الهجوم الذي شنته حماس على إسرائيل في 7 أكتوبر 2023، والرد العسكري الأخير في غزة عناوين الأخبار لمعظم الربع الأخير من عام 2023 وأوائل عام 2024. وقد حاولت المجتمع الدولي منع التصعيد وانتشار النزاع إلى أجزاء أخرى من الشرق الأوسط والعالم الأوسع. على الرغم من تلك الجهود، ظهرت حالة أمنية كبيرة في منتصف نوفمبر في البحر الأحمر ومضيق باب المندب بشكل أكثر تحديدًا (انظر الخريطة في الشكل 1)، عندما بدأت ميليشيات الحوثي المتمركزة في اليمن باستهداف الشحن الدولي الذي يمر عبر المنطقة. في غضون أسابيع، تصاعدت الحالة، مما أثر سلبًا على كل من الشحن والتجارة.

تعتبر أزمة البحر الأحمر اضطرابًا كبيرًا آخر يؤثر على الديناميات في الشحن واللوجستيات. في السنوات القليلة الماضية، تأثرت الممرات والطرق بين المحيطات بشكل كبير بسلسلة من الشذوذات الجوية (مثل الجفاف الذي قلل من قدرة قناة بنما بـ

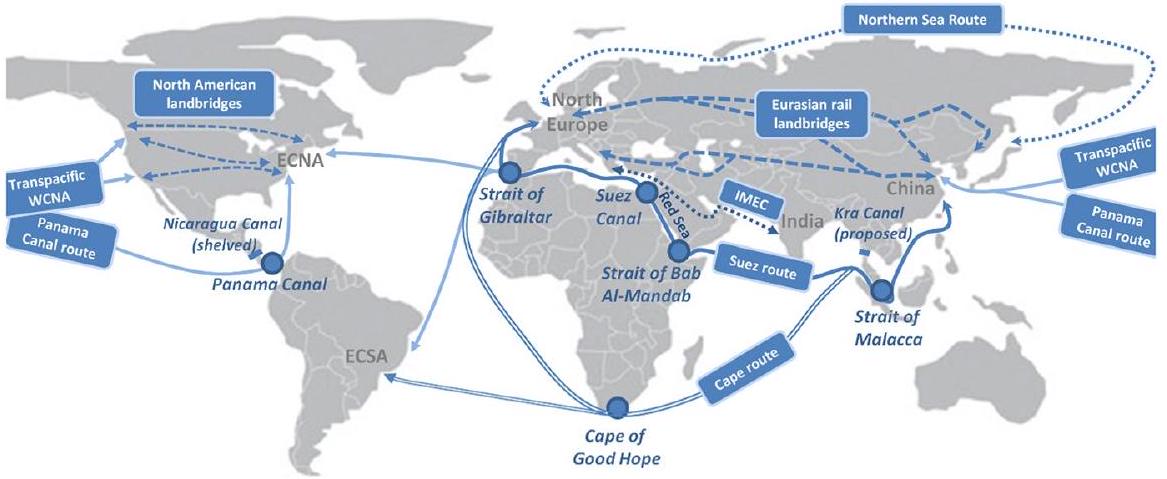

الشكل 1 البحر الأحمر ومضيق باب المندب كجزء من بدائل التوجيه في تجارة آسيا-شمال أوروبا وتجارة آسيا-الأمريكتين. IMEC ممر الهند-الشرق الأوسط-أوروبا، ECNA الساحل الشرقي لأمريكا الشمالية، ECSA الساحل الشرقي لأمريكا الجنوبية، WCNA الساحل الغربي لأمريكا الشمالية. المصدر المؤلفون

الحوادث ووقوع السفن (مثل حادثة ‘إيفر غيفن’، عندما تم إغلاق قناة السويس لمدة ستة أيام في مارس 2021، بتكلفة للتجارة قدرها 10 مليارات دولار يوميًا).

يوفر هذا الافتتاحي رؤى ليس فقط حول مجريات الأحداث التي وقعت خلال أزمة البحر الأحمر، ولكنه أيضًا يحلل التأثيرات قصيرة المدى – وربما طويلة المدى – لأزمة البحر الأحمر على عمليات السفن وشبكات الشحن؛ وأسعار الشحن وممارسات التسعير؛ وعلى سلاسل الإمداد العالمية. تم الانتهاء من الافتتاحية في 13 فبراير 2024. نظرًا لأن أزمة البحر الأحمر لا تزال تتكشف في وقت كتابة هذه السطور، تركز الافتتاحية بشكل أساسي على التأثيرات المبكرة للأزمة على صناعة الشحن وسلاسل الإمداد العالمية. يمكن معرفة التأثيرات الكاملة بدقة معينة فقط بمجرد انتهاء الأزمة أو احتوائها بطريقة تقلل من مستويات عدم اليقين وانعدام الأمن التي تواجهها الشحن والتجارة إلى مستويات مقبولة. ومع ذلك، لا يزال من غير الواضح تحت أي ظروف ستعتبر خطوط الشحن البحر الأحمر ممرًا آمنًا. هل سيستأنفون عبور السفن عندما يكون البحر الأحمر خاليًا من الحوادث لمدة

2 مقدمة ومسار الأحداث

لقد كانت الأزمة الحالية في البحر الأحمر تتصاعد منذ بعض الوقت، مع جذورها في الحرب الأهلية المستمرة في اليمن بين الحكومة المعترف بها دوليًا، التي تعمل من السعودية، وميليشيات الحوثي. بينما تدعم الأولى بشكل أساسي السعودية وتحالف دولي، فإن الأخيرة تحظى بدعم كل من إيران والجنود الموالين للرئيس السابق علي عبد الله صالح (غوزانسكي وإيران 2018).

جذور الحرب الأهلية في اليمن معقدة للغاية لتحليلها في هذه الافتتاحية؛ سيكون هذا خارج نطاقنا على أي حال. ومع ذلك، قد لا يكون من الخطأ تمامًا رؤية هذا النزاع الذي، على مدى عشر سنوات، أودى بحياة أكثر من ربع مليون شخص بسبب الأعمال العدائية وعواقبها، كأرضية للتنافس السعودي-الإيراني. مع قبول البلدين في مجموعة البريكس

في عام 2014، نجحت ميليشيات الحوثي في السيطرة على الموانئ والمدن الرئيسية على طول ساحل البحر الأحمر في اليمن. ما بدأ كحرب أهلية، محصورة فقط في اليمن، سرعان ما تصاعد إلى نزاع إقليمي، مع تدخل عسكري بقيادة السعودية دعمًا للحكومة في مارس 2015 (هوكاييم وروبرتس 2016). كان هذا التدخل يهدف بشكل أساسي إلى ضمان أمن مضيق باب المندب: نقطة اختناق عند المدخل الجنوبي للبحر الأحمر (انظر الشكل 1). تشترك في مضيق باب المندب اليمن وإريتريا وجيبوتي، وهو نقطة الاختناق التي ‘تحرس’ مدخل البحر الأحمر. عرض المضيق أقل من 30 كم وينقسم إلى قناتين بواسطة جزيرة بريم (اليادومي 1991). يجعل المضيق الأهمية الاستراتيجية لخليج عدن أكثر وضوحًا، حيث تحافظ معظم القوى الكبرى، بدءًا من الصين (في جيبوتي) والولايات المتحدة، على وجود عسكري في الخليج الذي تقليديًا يعاني من مستويات عالية من نشاط القرصنة وتهريب الأسلحة غير القانونية عبر الويب المظلم وطرق أخرى. كانت مبادرات التعاون الدولي والقوانين الإقليمية (مثل قانون جيبوتي) غير ناجحة إلى حد كبير في تحسين الوضع الأمني في الخليج.

ومع ذلك، لم يمنع النجاح النسبي للتدخل العسكري السعودي في عام 2015 ميليشيات الحوثي من الانخراط في انتقامات بحرية منذ ذلك الحين. باستخدام قوارب مسيرة، وصواريخ كروز، وزوارق سريعة، وألغام (نايتس وميلو 2015؛ عبد الله وسينغ 2018)، تم استغلال ضيق مضيق باب المندب من قبل ميليشيات الحوثي لبدء هجمات متقطعة بشكل رئيسي، ولكن ليس حصريًا،

عندما بدأت إسرائيل عملها العسكري ضد حماس في غزة في منتصف أكتوبر 2023، لم تعلن الدول والجماعات الإسلامية مثل حزب الله الحرب على إسرائيل. الاستثناء الملحوظ كان مجموعة أنصار الله (حزب الله): ميليشيات الحوثي التي تسيطر على غرب اليمن بما في ذلك معظم ساحل البحر الأحمر بالقرب من مضيق باب المندب. في أوائل نوفمبر 2023، أطلق الحوثيون صواريخ باليستية بعيدة المدى على إسرائيل، لكن جميعها تم اعتراضها من قبل الجيش الأمريكي والسعودي. من

منتصف نوفمبر 2023، بدأت ميليشيات الحوثي تركز أكثر على مهاجمة السفن التجارية. في البداية، تم تنفيذ عمليات اختطاف مثل تلك التي حدثت للسفينة التجارية غالاكسي ليدر. تلا ذلك قريبًا هجمات على السفن التجارية التي تسافر عبر البحر الأحمر السفلي ومضيق باب المندب، باستخدام الطائرات المسيرة، والصواريخ، والمسلحين على الزوارق السريعة. بينما ادعى الحوثيون في البداية أنهم يستهدفون فقط السفن التجارية المتجهة إلى أو من إسرائيل أو المملوكة لإسرائيل، أصبح من الواضح بسرعة أن السفن التابعة لدول تدعم الأعمال الإسرائيلية في غزة كانت تتعرض أيضًا للهجوم.

بحلول منتصف ديسمبر 2023، تصاعدت التهديدات الأمنية إلى درجة جعلت شركة ميرسك، وMSC، وBP، ومجموعات الشحن الأخرى توقف مرور السفن عبر القناة أو تبدأ في إعادة توجيه الحركة عبر كيب هورن. في الوقت نفسه، تم بدء تحالف بحري للدفاع عن الشحن ضد الهجمات. يوفر الجدول 1 نظرة عامة على الحوادث والأحداث الرئيسية خلال أزمة البحر الأحمر، مع سرد العديد من الهجمات (التي فشلت في الغالب) على السفن التجارية. عندما بدأ نقص الأمن في المنطقة يؤثر سلبًا على الشحن والتجارة الدولية، ظهرت ردود فعل دولية متزايدة، بقيادة الولايات المتحدة. تم الإدلاء ببيان رئيسي في 18 ديسمبر 2023، من قبل وزير الدفاع الأمريكي لويد أوستن، مشيرًا بشكل صريح إلى حرية الملاحة مما أدى إلى إنشاء عملية حارس الازدهار:

إن التصعيد الأخير في الهجمات المتهورة التي يشنها الحوثيون من اليمن يهدد التدفق الحر للتجارة، ويعرض البحارة الأبرياء للخطر، وينتهك القانون الدولي. البحر الأحمر هو ممر مائي حيوي كان أساسياً لحرية الملاحة وممراً تجارياً رئيسياً يسهل التجارة الدولية. يجب على الدول التي تسعى إلى دعم المبدأ الأساسي لحرية الملاحة أن تتكاتف لمواجهة التحدي الذي يمثله هذا الفاعل غير الحكومي الذي يطلق صواريخ باليستية وطائرات مسيرة (UAVs) على السفن التجارية من العديد من الدول التي تعبر المياه الدولية بشكل قانوني. (وزارة الدفاع الأمريكية، 2023).

تصاعدت الوضعية أكثر في أوائل يناير 2024، مع هجوم ضخم للحوثيين في 10 يناير، تلاه في 12 يناير أول ضربة مضادة جوية على الأراضي اليمنية من قبل القوات العسكرية الأمريكية والبريطانية. بين منتصف نوفمبر ومنتصف فبراير، تم تنفيذ حوالي 40 هجومًا للحوثيين على السفن العابرة في البحر الأحمر الجنوبي وخليج عدن. كانت الأضرار على السفن ضئيلة في معظم الحالات، وذلك بفضل اعتراض وتحييد عدد كبير من صواريخ الحوثيين والطائرات المسيرة والزوارق السريعة من قبل السفن الحربية في المنطقة. بحلول الأسبوع الثالث من يناير، كانت الهجمات تنتشر من حيث الجغرافيا (أي لم تعد فقط في الجزء الجنوبي من البحر الأحمر ولكن أيضًا في خليج عدن) ونطاق الأهداف (أي تستهدف أيضًا السفن البحرية). إن توسيع نطاق المخاطر الجغرافية يجعل من الصعب بشكل متزايد على القوات البحرية، التي تضطر إلى توزيع مواردها المحدودة بالفعل على منطقة أوسع.

الجدول 1 الحوادث والأحداث الرئيسية خلال أزمة البحر الأحمر (الوضع حتى 12 فبراير 2024).

| أفعال من قبل الحوثيين | مسار الأحداث أزمة البحر الأحمر | إجراءات مضادة |

| أواخر أكتوبر 2023 | HR يعلن الحرب على إسرائيل | |

| بداية نوفمبر 2023 | هجمات صاروخية باليستية بعيدة المدى غير فعالة على إسرائيل | |

| 19 نوفمبر 2023 | سفينة رورو غالاكسي ليدر (NYK): اختطاف، 25 فردًا من الطاقم محتجزين كرهائن | |

| 3 ديسمبر 2024 | ثلاث سفن (من بينها ناقلة البضائع Unity Explorer وسفينة الحاويات التابعة لـ OOCL): هجوم صاروخي ضخم | |

| 13 ديسمبر 2023 | ناقلة المواد الكيميائية أردمور إنكاونتر: مسلحون على قارب سريع وصاروخان | |

| عدد من شركات نقل الحاويات تعلن عن (توقف مؤقت) عن عبور البحر الأحمر أو تحويل السفن عبر طريق كيب. | 13 ديسمبر 2023 | |

| 14 ديسمبر 2023 | سفينة الحاويات ميرسك جبل طارق: هجوم صاروخي قريب | |

| 15 ديسمبر 2023 | سفينة الحاويات الجسر (هاباك-لويد): حريق على متنها بسبب ضربة صاروخية؛ سفينة الحاويات MSC Palatium III: تعرضت لضربة صاروخية | |

| تأسيس “عملية حارس الازدهار”، وهي مبادرة متعددة الجنسيات تركز على الأمن في البحر الأحمر (الولايات المتحدة، المملكة المتحدة، البحرين، كندا، فرنسا، إيطاليا، هولندا، النرويج، سيشيل وإسبانيا) | 18 ديسمبر 2023 | |

| البحرية الفرنسية تبدأ مرافقة السفن التجارية الفرنسية عبر البحر الأحمر | 22 ديسمبر 2023 | |

| 23 ديسمبر 2023 | ناقلات ساي بابا (ضربت)، إم في كيم بلوتو (ضربت) وبلامانن (قريبة من الضربة): هجمات بالطائرات المسيرة | |

| 27 ديسمبر 2024 | سفينة الحاويات MSC United VIII: هجوم غير ناجح؛ تم إسقاط 12 طائرة مسيرة هجومية، و3 صواريخ مضادة للسفن، و2 صاروخ كروز موجه ضد الأرض | |

| 28 ديسمبر 2023 | طائرة مسيرة واحدة وصاروخ باليستي مضاد للسفن تم اعتراضهما بواسطة البحرية الأمريكية | |

| 30/31-ديسمبر-2023 | سفينة الحاويات مايرسك هانغتشو: هجمات صاروخية وهجمات قوارب سريعة غير ناجحة على مدار يومين متتاليين | |

| وزير الدفاع البريطاني يلمح إلى اتخاذ إجراءات عسكرية مباشرة ضد الحوثيين في اليمن | 1 يناير 2024 | |

| 2 يناير 2024 | تزداد التوترات العسكرية في المنطقة مع وصول الفرقاطة ألبرز الإيرانية | |

| 3 يناير 2024 | سفينة الحاويات CMA CGM Tage: هجوم غير ناجح بصاروخين باليستيين مضادين للسفن | |

| ائتلاف من 12 دولة يصدر تحذيراً قوياً إذا استمرت حقوق الإنسان في الهجمات | 4 يناير 2024 | |

| 5 يناير 2024 | قارب طائرات مسيرة مزود بالمتفجرات انفجر: لا إصابات أو أضرار | |

| 7 يناير 2024 | طائرة مسيرة تم إسقاطها بواسطة مدمرة أمريكية؛ اقتراب مشبوه لقوارب صغيرة | |

| كوسكو تعلن أنها علقت خدمات الشحن إلى الموانئ الإسرائيلية في الوقت الحالي | 8 يناير 2024 | |

| أخبار غير مؤكدة تفيد بأن بعض خطوط الشحن تدخل في اتفاقيات مع الموارد البشرية لتجنب الهجمات | 9 يناير 2024 |

| الجدول 1 (مستمر) | ||

| أفعال من قبل الحوثيين | مسار الأحداث أزمة البحر الأحمر | إجراءات مضادة |

| 10 يناير 2024 | تم تحييد هجوم كبير على الموارد البشرية بواسطة الجيش الأمريكي: 18 طائرة مسيرة، و2 صاروخ كروز مضاد للسفن، وصاروخ باليستي مضاد للسفن واحد | منذ 12 يناير 2024 |

| أول سلسلة من الهجمات الجوية والصاروخية التي شنتها القوات العسكرية الأمريكية والبريطانية على مواقع الحوثيين في اليمن تستهدف أنظمة الرادار ومواقع تخزين وإطلاق الطائرات المسيرة والصواريخ. | ||

| 12 يناير 2024 | خليصة: هجوم صاروخي محتمل | |

| 13 يناير 2024 | تعتبر إدارة الموارد البشرية جميع السفن الأمريكية والبريطانية أهدافًا معادية، وليس فقط السفن المرتبطة بإسرائيل. | |

| 14 يناير 2024 | مدمرة البحرية الأمريكية يو إس إس لابون: هجوم صاروخي مضاد للسفن غير ناجح | |

| 15 يناير 2024 | ناقلة البضائع غيبالتار إيجل: تعرضت لضربة من صاروخ مضاد للسفن | |

| 16 يناير 2024 | زوغرافيا: هجوم صاروخي محتمل | |

| 17 يناير 2024 | ناقلة البضائع العامة جينكو بيكاردى: تعرضت لهجوم بطائرة مسيرة | |

| 19 يناير 2024 | ناقلة المواد الكيميائية Chem Ranger: هجوم صاروخي غير ناجح ضد السفن. الشركاء 2M MSC ومايرسك يغيرون شبكة آسيا-أوروبا والشبكة عبر المحيط الهادئ مع دورات جديدة حول كيب. | |

| 24 يناير 2024 | ||

| 24 يناير 2024 | سفن الحاويات المرفوعة تحت العلم الأمريكي مايرسك ديترويت ومايرسك تشيسابيك: هجوم صاروخي غير ناجح على السفن؛ ناقلة البضائع تومهوك: هجوم طائرة مسيرة غير ناجح | |

| 26 يناير 2024 | ناقلة المنتجات مارلين لواندا: هجوم صاروخي في خليج عدن؛ حريق كبير على متن السفينة تم إخماده بعد يوم. | |

| 1 فبراير 2024 | سفينة الحاويات كوي (CMA CGM): هجوم صاروخي أعلنته HR | |

| 6 فبراير 2024 | ناقلة البضائع ستار نازيا وسفينة الشحن مورنينغ تايد: هجوم صاروخي؛ أضرار طفيفة لستار نازيا | |

| 12 فبراير 2024 | ناقلة البضائع ستار إيريس: تعرضت لهجوم صاروخي | |

المصدر: المؤلفون، استنادًا إلى تقارير الأخبار الرئيسية والمتخصصة.

الشكل 2 مؤشر العبور اليومي لقناة السويس حسب نوع السفينة 2016-2024 (القيمة المتوسطة

لقد جلب تهديد الانتقام من كلا الجانبين مخاوف أمنية إلى مرحلة جديدة. قد تهدف ميليشيا الحوثي – كما يتوقع بعض المحللين – حتى إلى مواجهة مباشرة مع الولايات المتحدة. يمكن أن تقوض مثل هذه التصعيدات في أزمة البحر الأحمر المحادثات السلمية الجارية بين الحوثيين والسعودية الذين، كما ذُكر سابقًا، كانوا متورطين في حرب دموية منذ عام 2015. كما تستمر المخاوف من أن الوضع قد يتصاعد أكثر إذا أسفر هجوم ناجح للحوثيين عن وقوع إصابات على متن السفن و/أو غرق سفن الشحن التي تعبر البحر الأحمر. ومع ذلك، قد يتحسن الوضع الأمني بشكل كبير بين عشية وضحاها، في حال تم التوصل إلى اتفاق بين جميع الأطراف المعنية على وقف إطلاق نار طويل الأمد في غزة.

3 تأثيرات سلسلة التوريد

البحر الأحمر هو واحد من الممرات التجارية بين المحيطات الرئيسية في العالم وله مدخلان: قناة السويس في الشمال ومضيق باب المندب في الجنوب. وفقًا لإدارة معلومات الطاقة الأمريكية (2023)، يمر عبر مضيق باب المندب في المتوسط السنوي 8.8 مليون برميل من شحنات النفط يوميًا، مما يمثل

الجدول 2 تأثير إعادة توجيه كيب على مسافة الإبحار، وإجمالي وقت الرحلة الدائرية للسفينة، والانبعاثات لخدمة الحاويات الأسبوعية النموذجية بين آسيا وشمال أوروبا

| الوحدة | مسار البحر الأحمر/ قناة السويس | مسار كيب | الزيادة (%) | |

| إجمالي مسافة الإبحار الدائرية | ميل بحري | 24000 | 31000 | 29.2 |

| متوسط سرعة الإبحار | عقدة | 16 | 17 | 6.3 |

| متوسط الوقت الكلي في الميناء لكل زيارة | أيام | 1.7 | 1.7 | |

| عدد الزيارات للموانئ الآسيوية | عدد. | 5 | 5 | |

| عدد الزيارات للموانئ الأوروبية الشمالية | عدد. | 4 | 4 | |

| إجمالي وقت الإبحار | أيام | 62.5 | 76.0 | 21.6 |

| إجمالي وقت الميناء | أيام | 15.3 | 15.3 | |

| إجمالي وقت الرحلة الدائرية | أيام | 77.8 | 91.3 | 17.3 |

| عدد السفن المطلوبة للخدمة الأسبوعية | عدد. | 11 | 13 | 17.3 |

زيادة سرعة السفينة من 16 إلى 17 عقدة تؤدي عادةً إلى

المصدر المؤلفون

التأثير الكامل لأزمة البحر الأحمر على الشحن وسلاسل الإمداد العالمية لم يظهر بعد، حيث تحاول الشركات وخطوط الشحن، قدر الإمكان، التخفيف من الآثار اللوجستية المحتملة للأزمة. تستكشف هذه الفقرة التأثيرات الرئيسية الحالية والمحتملة المستقبلية لأزمة البحر الأحمر من خلال فحص (أ) التأثيرات على عمليات السفن وتكوينات شبكة الشحن، (ب) التغيرات في أسعار الشحن وممارسات الرسوم الإضافية، و(ج) الآثار الأوسع على سلاسل الإمداد العالمية.

المصدر المؤلفون

التأثير الكامل لأزمة البحر الأحمر على الشحن وسلاسل الإمداد العالمية لم يظهر بعد، حيث تحاول الشركات وخطوط الشحن، قدر الإمكان، التخفيف من الآثار اللوجستية المحتملة للأزمة. تستكشف هذه الفقرة التأثيرات الرئيسية الحالية والمحتملة المستقبلية لأزمة البحر الأحمر من خلال فحص (أ) التأثيرات على عمليات السفن وتكوينات شبكة الشحن، (ب) التغيرات في أسعار الشحن وممارسات الرسوم الإضافية، و(ج) الآثار الأوسع على سلاسل الإمداد العالمية.

3.1 إعادة توجيه السفن

الهجمات التي نفذتها ميليشيا الحوثي قد خفضت بشكل واضح ودراماتيكي التجارة عبر قناة السويس، حيث اختارت خطوط الشحن إعادة توجيه سفنها في الرحلة الأطول بشكل ملحوظ حول كيب هورن. في غياب أي موانئ للرسو على الإطلاق، Seadistance.net (2024) تقترح أن الإبحار حول أفريقيا كمسار بديل لقناة السويس يضيف 4575 ميل بحري في مسافة الإبحار بين شنغهاي وروتردام و12 يومًا في وقت الإبحار الإضافي، بافتراض سرعة متوسطة تبلغ 16 عقدة. يقدم الجدول 2 تقديراتنا بناءً على خصائص خدمة الحاويات الأسبوعية النموذجية على مسار التجارة بين آسيا وشمال أوروبا، ويفترض زيادة في السرعة المتوسطة بمقدار عقدة واحدة فقط في حالة إعادة توجيه كيب. تؤدي التحويلة حول كيب إلى زيادة إجمالي مسافة الإبحار بمقدار

بغض النظر عن التكاليف الإضافية والوقت المعني، فإن الغالبية العظمى من شركات نقل الحاويات الكبيرة قد علقت عمليات البحر الأحمر، بينما تواصل أساطيل عدد من المشغلين الإقليميين والنشيطين الأصغر استخدام البحر الأحمر. كانت CMA CGM هي الشركة الكبيرة الوحيدة التي لا تزال تعبر البحر الأحمر بمساعدة مرافقة من البحرية الفرنسية. في النهاية، انتقلت الشركة الفرنسية أيضًا إلى مسار كيب في أوائل فبراير 2024.

تظهر بيانات Linerlytica أنه بين 15 ديسمبر 2024 و7 يناير 2024، تم تحويل ما مجموعه 354 سفينة حاويات إلى مسار كيب، مما يمثل سعة قدرها 4.65 مليون حاوية أو

- تأثير على سعة الأسطول تتطلب إعادة توجيه السفن بشكل جماعي عبر كيب سعة أسطول أكبر بكثير لنقل نفس الكمية من البضائع، في نفس فترة الوقت وتكرار زيارة الميناء. تتطلب خدمة الحاويات النموذجية بين شمال أوروبا وآسيا من 11 إلى 12 سفينة لضمان تكرار أسبوعي. بافتراض أن سرعات السفن التجارية تظل دون تغيير (أي 15 إلى 17 عقدة لسفينة حاويات نموذجية)، فإن الوقت الإضافي للإبحار المرتبط بتحويلة مسار كيب يعني أنه يجب إضافة ما لا يقل عن سفينتين إلى مثل هذه الحلقة للحفاظ على جدول مغادرة أسبوعي. من الجانب الإيجابي، يسمح إعادة التوجيه لشركات النقل بامتصاص بعض فائض الأسطول الذي دخل السوق منذ النصف الثاني من عام 2022. من الجانب السلبي، فإن التغيرات المفاجئة في نشر الأسطول ستؤدي حتمًا إلى قيود على السعة على المدى القصير، مع احتمال حدوث نقص في المساحة المتاحة للشاحنين في الفترة التي تسبق عيد رأس السنة الصينية (CNY). تقدر MDS Transmodal أن 2.6 مليون حاوية من المساحة المطلوبة لمعالجة النقص في السعة الناتج عن التحويلات (Nightingale 2024). وهذا يمثل حوالي 200 سفينة إضافية، مع الأخذ في الاعتبار أحجام السفن المستخدمة والمنطقة المخدومة. علاوة على ذلك، تعيد شركات النقل استئناف الخدمات التي تم تعليقها سابقًا بسبب COVID-19 (الإبحارات الفارغة). في الوقت نفسه، كنتيجة مباشرة لاندفاع طلب السفن في 2021 وأوائل 2022، من المقرر دخول الكثير من السعة الجديدة إلى السوق في 2024: 478 سفينة بإجمالي حوالي 3.1 مليون حاوية، متجاوزة الرقم القياسي السابق لعام 2023 بنسبة

. على الرغم من أنه من المتوقع أيضًا زيادة إعادة تدوير السفن، إلا أن ذلك لن يعوض النطاق الذي يتم به إضافة السعة إلى السوق: مع توقع نمو صافي يبلغ حوالي ، من المتوقع أن تتجاوز السعة الإجمالية في السوق 30 مليون مكان (Rasmussen 2024). - أثر الصدمة الأولية في شبكة الشحن العالمية أدت الاضطرابات في البحر الأحمر إلى تأثير صدمة قصير المدى في أعمال الحاويات. على سبيل المثال، تأثرت مسار آسيا-أوروبا بشدة في أواخر ديسمبر 2023 وأوائل يناير 2024 نظرًا لعدم اليقين والتقلبات المحيطة بقرارات شركات النقل لوقف عبور البحر الأحمر أو البدء في إعادة التوجيه عبر كيب. تم تأخير بعض مغادرات السفن

في آسيا، بينما غيرت أخرى مسارها خلال رحلتها (حتى عدة مرات) أو واجهت تغييرات عشوائية في تسلسل زيارات الميناء. في النهاية، قررت الغالبية العظمى من شركات نقل الحاويات الكبيرة تعليق عمليات البحر الأحمر، مما أدى في النهاية إلى وضوح أكبر بشأن المتغيرات اللوجستية الرئيسية، مثل أوقات العبور المتوقعة وسعة السفن المتاحة. على سبيل المثال، في أواخر يناير 2024، أعلنت شركتا 2 M، ميرسك وMSC، أنهما قد أعادت ضبط جداولها لخدمات الحاويات بين آسيا وUSEC حتى نهاية مارس مع تحويلة عبر مسار كيب. هذا جزء من تغييرات أوسع على شبكة آسيا-أوروبا وعبر المحيط الهادئ مع دورات جديدة حول كيب، مما يعني حلاً دائماً أكثر حول أفريقيا. - البحر الأبيض المتوسط كزقاق مؤقت إن إعادة توجيه السفن عبر كيب تعني أن دور حوض البحر الأبيض المتوسط، الذي أطلق عليه الرومان ‘ماري نوستروم’، وقد يكون بالنسبة للبعض (هارالامبيدس 2023) ‘محور المحاور’ الذي يربط بين أربع قارات، قد يتأثر بشكل خطير. لقد أصبح البحر الأبيض المتوسط فعليًا زقاقًا بحريًا، حيث تدخل السفن وتخرج عبر مضيق جبل طارق. في سوق الحاويات، قد تشجع هذه الوضعية الفريدة الناقلين على تقسيم الخدمات على الطرق الرئيسية بين آسيا وأوروبا من خلال استخدام أكثر كثافة لمراكز النقل بالقرب من مضيق جبل طارق؛ أي، ليس فقط طنجة ميد وألكسيراس، ولكن أيضًا سيني وبلنسية – ربما تواصل طريقها إلى الساحل الشرقي للولايات المتحدة -، والمراكز الكبيرة في شمال أوروبا (روتردام، أنتويرب-بروج، هامبورغ على سبيل المثال). يمكن أن تقدم الموانئ الغربية الأفريقية مثل أبيدجان، كوتونو، لاغوس ولومي (تشن وآخرون 2020) بدائل مماثلة (أي، تقسيم الخدمات إلى الساحل الشرقي للولايات المتحدة، وأوروبا الجنوبية والشمالية). ستخفف مثل هذه التدابير التشغيلية الضغط على استخدام السفن الكبيرة في أعماق البحار وتجعل من الأسهل إلى حد ما معالجة أي نقص في السعة ناتج عن إعادة التوجيه عبر كيب.

- انبعاثات السفن الأعلى إن إعادة التوجيه حول كيب والمسافات الطويلة للإبحار تزيد من إجمالي استهلاك الوقود وانبعاثات السفن. علاوة على ذلك، فإن أوقات الرحلة الأطول تعني أنه يجب إضافة سفينتين على الأقل إلى خدمة آسيا-أوروبا للحفاظ على المغادرات الأسبوعية. كما تضيف السفن الإضافية إلى إجمالي انبعاثات الأسطول لطلب الشحن المعين. بالنسبة لخدمة الحاويات الأسبوعية النموذجية بين آسيا وشمال أوروبا، يمكن تقدير الزيادة في الانبعاثات في البحر المرتبطة بإعادة توجيه كيب بـ

لسفينة فردية و للأسطول المطلوب لتشغيل خدمة أسبوعية على هذا الطريق التجاري (انظر الجدول 2 لمزيد من التفاصيل). هذه الانبعاثات الإضافية هي أخبار سيئة لصناعة يجب أن تأخذ في الاعتبار نقاط التفتيش الإرشادية للمنظمة البحرية الدولية (IMO 2023) التي تهدف إلى تقليل الانبعاثات بنسبة لا تقل عن ، والسعي لتحقيق ، بحلول عام 2030 مقارنة بمستويات عام 2008، وعلى الأقل ، والسعي لتحقيق بحلول عام 2040، والوصول إلى صافي صفر “بحلول أو حول (أي، قريب من) عام 2050.” - انخفاض إيرادات الرسوم لهيئة قناة السويس (SCA) أدت عمليات العبور الأقل عبر قناة السويس إلى انخفاض كبير في إيرادات الرسوم لمصر. في السنة المالية 2022-2023، وصلت الرسوم إلى رقم قياسي قدره 9.4 مليار دولار أمريكي (رويترز 2023)، مما يمثل

من الناتج المحلي الإجمالي للبلاد. من المفهوم أن مصر حريصة على حماية هذا المصدر الرئيسي للإيرادات. ومع ذلك، أفادت هيئة قناة السويس عن انخفاض قدره في إيرادات الرسوم في الأسبوعين الأولين من عام 2024، مقارنة بنفس الفترة في عام 2023 (رويترز 2024أ). باستخدام البيانات المذكورة أعلاه حول السفن الحاويات المعاد توجيهها، يمكن تقدير أن

هيئة قناة السويس تكبدت خسارة تتراوح بين 175 إلى 350 مليون دولار من رسوم عبور القناة، فقط من السفن الحاويات، بين 15 ديسمبر 2023 و9 يناير 2024.

تضيف أزمة البحر الأحمر إلى الدعوة لمزيد من المرونة في التوجيه في شبكة النقل العالمية. تعتبر الاختناقات (أو، بالأحرى، نقاط الاختناق) في شبكة الشحن العالمية مثل باب المندب، أو البحر الأحمر بشكل عام، كثيرة

3.2 أسعار الشحن والرسوم الإضافية

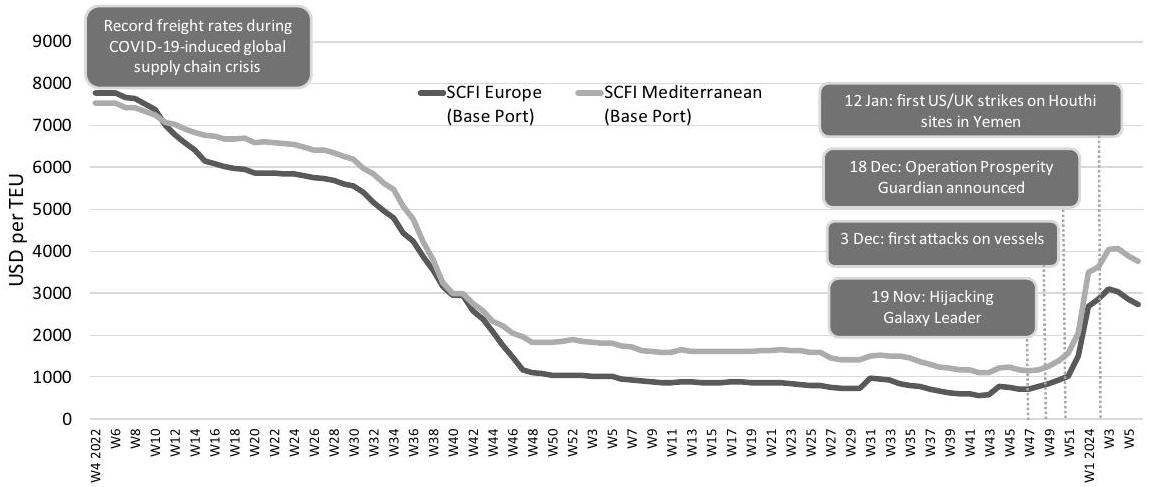

كما قد يُتوقع، كان لأزمة البحر الأحمر تأثير ملحوظ على أسعار الشحن الفورية. ارتفع مؤشر الشحن بالحاويات في شنغهاي (SCFI) لشمال أوروبا من 707 دولار أمريكي/حاوية في منتصف نوفمبر إلى 3103 دولار أمريكي/حاوية في الأسبوع الثالث (W3) من يناير 2024 (+339%)، تلاه انخفاض طفيف ليصل إلى 2723 دولار أمريكي/حاوية في الأسبوع 6 من 2024. ومع ذلك، ظلت الزيادات الضخمة في أسعار الشحن أقل بكثير من أسعار الشحن القياسية التي تم مواجهتها خلال سنوات COVID-19 (2021-أوائل 2022)، والتي اقتربت من 8000 دولار أمريكي/حاوية. سجل مؤشر SCFI للبحر الأبيض المتوسط زيادة قدرها

الشكل 3 تطور مؤشر الشحن بالحاويات في شنغهاي (SCFI)، شمال أوروبا والبحر الأبيض المتوسط، الأسبوع 4، 2022، إلى الأسبوع 6، 2024، بالدولار الأمريكي لكل حاوية.

تزايدت أسعار الشحن أيضًا جزئيًا نتيجة للمخاوف المتزايدة من عدم كفاية سعة الشحن والحاويات، لنقل المنتجات قبل عيد الربيع الصيني.

يمكن أيضًا العثور على تأثيرات الأسعار في طرق التجارة الأخرى، بشكل رئيسي في عبر المحيط الهادئ (SCFI 3974 دولار أمريكي/حاوية في منتصف يناير 2024) وطرق الصين-الساحل الشرقي لأمريكا الشمالية (ECNA) (5813 دولار أمريكي/حاوية). تأثرت الأخيرة بشدة بتأثير أزمة البحر الأحمر ومستويات المياه المنخفضة في قناة بنما التي قيدت بشدة عمليات عبور السفن اليومية منذ أوائل 2023.

قد تتأثر أيضًا أسعار العقود طويلة الأجل في شحن الحاويات بأزمة البحر الأحمر. إذا استمرت الحالة الحالية لفترة طويلة، فسيتم التفاوض على عقود جديدة بأسعار أعلى بكثير من تلك التي كانت قبل اندلاع الأزمة. أيضًا، قد لا تلتزم شركات النقل بعقود طويلة الأجل، مما يدفع الشاحنين إلى السوق الفورية. على وجه الخصوص، قد تختار شركات النقل عقودًا بأدنى الأسعار المتفق عليها، معتبرةً

أنها ذات قيمة أقل، مقارنة بأسعار السوق الفورية. يمكن أن يكون لهذا آثار تشغيلية على الشاحنين، مثل زيادة خطر انزلاق الحاويات.

تعتبر أسعار الشحن الأعلى نتيجة مشتركة لامتصاص السعة من خلال المسار الأطول حول كيب، مما يقلل من الفتحات المتاحة لكل وحدة زمنية، بالإضافة إلى التكاليف الإضافية للوقود المرتبطة بهذا المسار بسبب المسافة الأطول، وتوقعات الشاحنين السلبية بشأن (عدم) توفر السعة في المستقبل. كما زادت التكاليف الإضافية مثل التأمين. ارتفعت أقساط مخاطر التأمين للإبحار عبر المنطقة عالية المخاطر من

لقد دفعت التكاليف الصافية الإضافية لإعادة التوجيه شركات النقل إلى الإعلان عن رسوم إضافية خاصة. منذ أواخر نوفمبر 2023، قدمت معظم شركات نقل الحاويات ‘رسوم مخاطر الحرب’ للشحنات إلى ومن إسرائيل. في 20 ديسمبر 2023، قدمت CMA CGM ‘رسوم البحر الأحمر’ بقيمة 2700 دولار أمريكي لكل وحدة حاوية مكافئة (FEU) لجميع الشحنات المرسلة إلى أو من موانئ البحر الأحمر. كما نفذت الشركة ‘رسوم الطوارئ’ بقيمة 1000 دولار أمريكي لكل FEU على الطريق الغربي من آسيا إلى البحر الأبيض المتوسط و525 دولار أمريكي لكل FEU للشحنات المتجهة شرقًا من أوروبا إلى آسيا. في أوائل يناير 2024، قدمت MSC ‘رسوم تعديل الطوارئ’ بقيمة 500 دولار أمريكي لكل وحدة حاوية مكافئة (TEU) و1000 دولار أمريكي لكل FEU على طرق أوروبا-آسيا وأوروبا-الشرق الأوسط. تستخدم Hapag-Lloyd ‘رسوم استرداد العمليات’ المماثلة. تطبق Maersk ‘رسوم اضطراب العبور’ على الشحنات على السفن المتأثرة بالاضطرابات. تبلغ قيمة الرسوم 400 دولار أمريكي لكل FEU وتطبق على الحجوزات بين 21 ديسمبر 2023 و28 يناير 2024. نظرًا لأن الاضطرابات في الخدمة تؤثر على تدفق المعدات الفارغة، فقد نفذت عدد من شركات النقل أيضًا رسوم عدم توازن المعدات الفارغة. تأتي الرسوم المذكورة أعلاه بالإضافة إلى رسوم أخرى مستخدمة على نطاق واسع مثل عامل تعديل الوقود (BAF؛ رسوم وقود) أو رسوم موسم الذروة.

على الرغم من ارتفاع أسعار الشحن، لا يُتوقع أن تؤدي أزمة البحر الأحمر والتحويلات حول كيب إلى تحسين هيكلي في عدم التوازن بين الطلب والعرض في

سوق الحاويات. كما ذُكر سابقًا، ستدخل الكثير من سعة السفن الجديدة حيز التشغيل في عامي 2024 و2025، متجاوزة توقعات الطلب، حتى مع الأخذ في الاعتبار الحاجة إلى سفن إضافية لتعويض المسافات الطويلة للإبحار حول كيب. من المحتمل جدًا أن تثبت أزمة البحر الأحمر أنها مجرد عامل تأخير في الوضع المتزايد للاكتفاء الزائد في شحن الحاويات. بعبارة أخرى، فإن سوق الحاويات العالمي يتعرض لزيادة كبيرة في العرض من السفن الجديدة لدرجة أن هناك مجالًا كافيًا لتغطية النطاق الحالي للاضطرابات في البحر الأحمر. بدأت شركات النقل في إعادة جدولة خدماتها في أواخر يناير 2024، وقد تم بالفعل احتساب التأثير الذروي قبل رأس السنة الصينية. يضيف الاكتفاء الزائد مزيدًا من الضغط النزولي على أسعار الشحن على المدى المتوسط. في أوائل فبراير 2024، اقترحت شركات النقل الكبرى مثل ميرسك أنها لا تتوقع أن تحسن الأزمة بشكل كبير هوامش التشغيل في الصناعة لعام 2024. سيعتمد الكثير على مدى طول فترة أزمة البحر الأحمر.

3.3 التأثيرات الأوسع لسلسلة الإمداد

تؤثر أزمة البحر الأحمر على ظروف التجارة، ويواجه الشاحنون تحديات في بناء المرونة والعمل على خطط الطوارئ حتى يتم استعادة الثقة في أمان طريق البحر الأحمر. يحاول الشاحنون التكيف مع واقع طريق كيب الجديد من خلال تنويع سلاسل الإمداد والنظر في طرق ووسائل نقل بديلة.

تولد الأزمة اهتمامًا متزايدًا في خدمات السكك الحديدية البرية الأوراسية، التي هي أسرع ولكنها أكثر تكلفة من النقل البحري. تتراوح أوقات العبور في الممر الحديدي الشمالي الأكثر ارتباطًا بين الصين عبر كازاخستان وروسيا إلى بولندا وأوروبا الغربية عادةً بين 15 و25 يومًا، مع أسعار شحن تتراوح بين 7000 و15,000 يورو لكل حاوية. تشكل خدمات السكك الحديدية الأوراسية بشكل أساسي خيارًا متخصصًا للبضائع عالية القيمة بكميات محدودة، لذا من المتوقع أن تظل حصتها الإجمالية في تجارة آسيا-أوروبا متواضعة إلى حد ما.

بالإضافة إلى الاهتمام المتزايد بخدمات السكك الحديدية الأوراسية، هناك أيضًا اهتمام واضح في النقل المشترك بين الجو والبحر. كما شهد الطلب (وبالتالي أسعار الشحن) على نقل الشحنات الجوية ذات القيمة العالية من آسيا إلى أوروبا، وخاصة من الشرق الأوسط إلى كل من أوروبا والولايات المتحدة، زيادة ملحوظة. على سبيل المثال، أفادت شركة فريتوس أن متوسط تكلفة الشحن الجوي على مسار الشرق الأوسط إلى أوروبا قد ارتفع.

يمكن أن يؤدي تحويل السفن الضخمة عبر كيب إلى ازدحام في الطرق البديلة، مما سيؤثر بدوره على سلسلة الإمداد. لقد أدت أوقات العبور الأطول المرتبطة بطريق كيب إلى بعض التأثيرات القصيرة الأجل للشاحنين. هؤلاء يواجهون مخزونات عائمة أعلى بكثير وتأخيرات في التسليم، أي مع عدم موثوقية أعلى تضرب في صميم اللوجستيات العالمية الفعالة. تؤثر هذه الآثار بشكل خاص على الصناعات التي تعتمد على أنظمة التسليم والإنتاج في الوقت المحدد (JIT) وعند الطلب (MTO).

على سبيل المثال، في صناعة السيارات، أوقفت تسلا الإنتاج في مصنعها في برلين-براندنبورغ بين 29 يناير و11 فبراير بسبب انقطاع التدفق المستمر للمكونات من الموردين الآسيويين إلى المصنع الألماني نتيجة لإعادة توجيه السفن (رويترز 2024ب). توقفت فولفو للسيارات في غنت (بلجيكا) عن الإنتاج لمدة ثلاثة أيام في منتصف يناير، أيضًا بسبب نقص في المكونات (رويترز 2024ب). أوقفت سوزوكي موتور الإنتاج في مصنعها في هنغاريا بين 14 و21 يناير 2024 (NHK 2024). تعتبر تجارة الفواكه والخضروات قطاعًا آخر تأثر بأوقات النقل الأطول. تظهر هذه الأمثلة أن مرافق الإنتاج وسلاسل التوريد المعتمدة على الإنتاج حسب الطلب/التسليم في الوقت المحدد تشعر على الفور بتأثيرات أي اضطراب كبير في العمليات الدقيقة للأنظمة العالمية للإنتاج/التوزيع. تزيد هذه النقصات قصيرة الأجل في المكونات والمنتجات من خطر تأثير السوط (لي وآخرون 1997)، حيث يمكن أن تتضخم التقلبات الصغيرة وتسبب عواقب أكبر على طول السلسلة، مثل الموانئ البحرية. كان التحول المفاجئ إلى طريق كيب في الأسابيع الأولى من أزمة البحر الأحمر الأكثر تأثيرًا. ومع ذلك، بحلول أواخر يناير، بدأت بعض خطوط الشحن في تعديل جداولها لتناسب واقع التوجيه الجديد إلى أفريقيا. وقد أدى ذلك إلى تقليل عدم اليقين بشأن أوقات النقل البحرية بشكل كبير، مما سمح لمخططي سلاسل التوريد بتنفيذ حلول أكثر قوة لتبسيط تدفق البضائع.

على سبيل المثال، في صناعة السيارات، أوقفت تسلا الإنتاج في مصنعها في برلين-براندنبورغ بين 29 يناير و11 فبراير بسبب انقطاع التدفق المستمر للمكونات من الموردين الآسيويين إلى المصنع الألماني نتيجة لإعادة توجيه السفن (رويترز 2024ب). توقفت فولفو للسيارات في غنت (بلجيكا) عن الإنتاج لمدة ثلاثة أيام في منتصف يناير، أيضًا بسبب نقص في المكونات (رويترز 2024ب). أوقفت سوزوكي موتور الإنتاج في مصنعها في هنغاريا بين 14 و21 يناير 2024 (NHK 2024). تعتبر تجارة الفواكه والخضروات قطاعًا آخر تأثر بأوقات النقل الأطول. تظهر هذه الأمثلة أن مرافق الإنتاج وسلاسل التوريد المعتمدة على الإنتاج حسب الطلب/التسليم في الوقت المحدد تشعر على الفور بتأثيرات أي اضطراب كبير في العمليات الدقيقة للأنظمة العالمية للإنتاج/التوزيع. تزيد هذه النقصات قصيرة الأجل في المكونات والمنتجات من خطر تأثير السوط (لي وآخرون 1997)، حيث يمكن أن تتضخم التقلبات الصغيرة وتسبب عواقب أكبر على طول السلسلة، مثل الموانئ البحرية. كان التحول المفاجئ إلى طريق كيب في الأسابيع الأولى من أزمة البحر الأحمر الأكثر تأثيرًا. ومع ذلك، بحلول أواخر يناير، بدأت بعض خطوط الشحن في تعديل جداولها لتناسب واقع التوجيه الجديد إلى أفريقيا. وقد أدى ذلك إلى تقليل عدم اليقين بشأن أوقات النقل البحرية بشكل كبير، مما سمح لمخططي سلاسل التوريد بتنفيذ حلول أكثر قوة لتبسيط تدفق البضائع.

أحد الآثار المباشرة لأزمة البحر الأحمر هو القلق بشأن توفر الحاويات. تعني أوقات الرحلات الأطول والمسارات البحرية المعدلة أن عددًا كبيرًا من الحاويات الفارغة ينتهي بها المطاف في المكان الخطأ في الوقت الخطأ. وقد قدرت بورصة البلطيق (2024) نقصًا يبلغ حوالي 780,000 حاوية قياسية في آسيا قبل عيد رأس السنة الصينية. لتخفيف بعض الضغط، زادت إنتاجية الحاويات الجديدة (بشكل رئيسي في الصين) منذ أواخر ديسمبر 2023.

لقد رأى عدد من المعلقين أن توقيت أزمة البحر الأحمر هو مقدمة لعاصفة ‘مثالية’ في سلاسل الإمداد العالمية: ارتفاع سريع في أسعار الشحن والرسوم الإضافية؛ أوقات عبور أطول للسفن المطلوبة بشكل عاجل في آسيا للتحميل قبل رأس السنة الصينية؛ ومشاكل توفر الحاويات، وكلها تتفاقم بسبب القيود المستمرة في السعة التي شهدها قناة بنما، مما يشير إلى ‘عاصفة مثالية’ مجازية. في مثل هذه الحالة، يشعر الشاحنون بالقلق لتأمين سعة السفن والحاويات من وكلاء الشحن والناقلين، ويأتي ذلك بتكلفة. ومع ذلك، هناك شعور عام بأن الأزمة الحالية أكثر قابلية للإدارة بكثير مقارنة بما كان يجب أن تتحمله سلاسل الإمداد خلال اضطرابات COVID-19. بطريقة ما، يمكن تفسير ذلك جزئيًا من خلال وضع سعة الأسطول، من حيث (عدم) التوفر، الذي كان أسوأ بكثير حينها (انظر Notteboom et al. 2021؛ Cullinane و Haralambides 2021؛ Cullinane et al. 2023 لمزيد من التحليل التفصيلي).

4 إلى أين تذهب: التكيف المؤقت أم التعديل الهيكلي؟

تعمل الشحنات واللوجستيات العالمية والموانئ في بيئة متقلبة تتسم بعدم اليقين والمخاطر المفروضة على أصحاب المصلحة لديهم ليس فقط من البيئة الخارجية، ولكن أيضًا من أفعالهم وقراراتهم التجارية.

ليس من غير المعقول أنه، خلال عام 2024، ستتزامن أزمة البحر الأحمر مع اضطرابات أخرى مثل الأحداث المناخية القاسية أو التوترات الجيوسياسية. قد تؤدي هذه إلى تمديد فترة عدم موثوقية سلاسل الإمداد، التي شهدها كل من

الشحن والموانئ منذ اندلاع أزمة COVID-19 في عام 2020 (Notteboom et al. 2021؛ Cullinane و Haralambides 2021؛ Cullinane et al. 2023). في عالم ‘VUCA’ (متقلب، غير مؤكد، معقد، وغامض؛ Bennet و Lemoine 2014)، من المحتمل أن تستمر الاضطرابات في أسواق الشحن، مما يتطلب المرونة والتخطيط الاستباقي لتحمل الصدمات الإضافية.

الشحن والموانئ منذ اندلاع أزمة COVID-19 في عام 2020 (Notteboom et al. 2021؛ Cullinane و Haralambides 2021؛ Cullinane et al. 2023). في عالم ‘VUCA’ (متقلب، غير مؤكد، معقد، وغامض؛ Bennet و Lemoine 2014)، من المحتمل أن تستمر الاضطرابات في أسواق الشحن، مما يتطلب المرونة والتخطيط الاستباقي لتحمل الصدمات الإضافية.

إذا لم تتحسن الحالة الأمنية في البحر الأحمر بشكل كبير في الربع الثاني من عام 2024، فقد يؤدي ذلك إلى زيادة خطر الضغوط التضخمية، اعتمادًا على مدى استمرار الاضطراب وما إذا كانت هناك اضطرابات أخرى تظهر. في هذه الأثناء، سيبحث صانعو القرار في سلاسل الإمداد عن تنفيذ حلول قصيرة الأجل للتحديات التي يواجهونها. وقد أسفر ذلك بالفعل عن:

(أ) إعادة توجيه السفن إعادة توجيه سريعة نسبيًا للتدفقات البحرية التي قد تستمر في المدى المتوسط، اعتمادًا على كيفية تطور أزمة البحر الأحمر؛

(ب) استخدام بدائل النقل زيادة استخدام بدائل النقل، بشكل أساسي من السكك الحديدية (لا سيما الجسور البرية الأوراسية والأمريكية)؛ و

(ج) إعادة تصميم سلسلة الإمداد إعادة هيكلة مصادر الإمداد، وتكوينات سلاسل الإمداد، وجداول الإنتاج.

(أ) إعادة توجيه السفن إعادة توجيه سريعة نسبيًا للتدفقات البحرية التي قد تستمر في المدى المتوسط، اعتمادًا على كيفية تطور أزمة البحر الأحمر؛

(ب) استخدام بدائل النقل زيادة استخدام بدائل النقل، بشكل أساسي من السكك الحديدية (لا سيما الجسور البرية الأوراسية والأمريكية)؛ و

(ج) إعادة تصميم سلسلة الإمداد إعادة هيكلة مصادر الإمداد، وتكوينات سلاسل الإمداد، وجداول الإنتاج.

اعتمادًا على كيفية تطور الأحداث، تثار بعض الأسئلة المثيرة للاهتمام حول ما إذا كانت بعض الخطوات القصيرة الأجل، التكيفية، (إطفاء الحرائق) ستقبل وتتبنى كحلول لوجستية طويلة الأجل – أي كتعديلات هيكلية:

4.1 إعادة توجيه السفن

لم يتم اكتشاف طريق كيب اليوم. في الواقع، كانت التفاف حول أفريقيا هو البديل الوحيد في التجارة بين آسيا وأوروبا خلال الحروب العربية الإسرائيلية (أزمة السويس عام 1956؛ حرب الأيام الستة عام 1967 وحرب يوم كيبور عام 1973)، وكلما كانت هناك زيادة في أنشطة القرصنة في البحر الأحمر، وارتفاع أسعار الوقود والحاجة إلى الإبحار البطيء، وزيادات باهظة في رسوم قناة السويس، وما إلى ذلك (Notteboom و Rodrigue 2011a، b؛ Notteboom 2012). بالمصادفة، لا يخدم طريق كيب أوروبا فقط، ولكن السفن، في طريقها إلى هناك، أو إلى الأمريكتين، يمكن أن تقوم بعمليات نقل في الموانئ الجنوب أفريقية، وبالتالي تخدم أيضًا كل من شرق وغرب أفريقيا (انظر الشكل 1). بديلان آخران، ربما أكثر ‘راديكالية’، عن السويس هما طريق البحر الشمالي القطبي (NSR) والممر الهندي-الشرق الأوسط-أوروبا (IMEC) الذي تم الإعلان عنه مؤخرًا.

بغض النظر عن الأزمة الحالية، تم دراسة NSR لسنوات وقد جربت شركات كبرى مثل Cosco و Maersk استخدامه. الطريق هو

حتى بعدم تطوير خيار NSR لأسباب بيئية (Verny و Grigentin 2009؛ Zhu et al. 2018). في صيف عام 2023، شملت أنشطة الشحن في NSR أول خدمة حاويات منتظمة متواضعة بين آسيا وأوروبا تديرها شركة الشحن الصينية NewNew باستخدام أربع سفن حاويات صغيرة بسعات تتراوح من 1200 إلى 2800 TEU (Humpert 2024). في الوقت الحالي، لا يزال NSR طريقًا متخصصًا لبعض التجارة البحرية المتعلقة بالطاقة والتعدين مثل عبور الغاز الطبيعي المسال النرويجي إلى اليابان، أو شحن الهيدروكربونات من القطب الشمالي (Schøyen و Bråthen 2011؛ Gunnarsson و Moe 2021).

حتى بعدم تطوير خيار NSR لأسباب بيئية (Verny و Grigentin 2009؛ Zhu et al. 2018). في صيف عام 2023، شملت أنشطة الشحن في NSR أول خدمة حاويات منتظمة متواضعة بين آسيا وأوروبا تديرها شركة الشحن الصينية NewNew باستخدام أربع سفن حاويات صغيرة بسعات تتراوح من 1200 إلى 2800 TEU (Humpert 2024). في الوقت الحالي، لا يزال NSR طريقًا متخصصًا لبعض التجارة البحرية المتعلقة بالطاقة والتعدين مثل عبور الغاز الطبيعي المسال النرويجي إلى اليابان، أو شحن الهيدروكربونات من القطب الشمالي (Schøyen و Bråthen 2011؛ Gunnarsson و Moe 2021).

تم تقديم مشروع IMEC البالغ قيمته 20 مليار دولار، والذي يقصر أيضًا المسافات عن طريق

كما قيل أعلاه، قد يقدم بديل أقل راديكالية وحل توجيه طويل الأجل من خلال الشحنات التي كانت حتى الآن تتحرك من آسيا إلى الساحل الشرقي الأمريكي عبر السويس والآن، خلال هذه الفترة من الأزمة، يمكن أن تتحول عبر المحيط الهادئ إلى موانئ الساحل الغربي الأمريكي للوصول إلى خدمات السكك الحديدية للجسور البرية الأمريكية. سيكون التأثير الجانبي لهذا الاتجاه هو إحياء حركة الموانئ WCNA، التي كانت تخسر باستمرار لصالح موانئ ECNA في السنوات الأخيرة (Kent و Haralambides، 2022؛ وزارة النقل الأمريكية 2023).

4.2 استخدام بدائل النقل (السكك الحديدية، الهواء)

إذا تم تقديم مستوى الخدمة المناسب بنجاح من خلال خيارات النقل البديلة التي يتم تجربتها خلال هذه الأزمة، فهل يمكن أن يعني ذلك أن حصة من السوق (مهما كانت صغيرة، ومهما كانت مرتبطة بشكل حتمي بشحنات ذات قيمة عالية و/أو حساسة للوقت) قد فقدت إلى الأبد لشحن الحاويات؟

4.3 إعادة تصميم سلسلة الإمداد

هل ستوفر الإصلاحات قصيرة الأجل التي يتم تنفيذها حاليًا دافعًا لحلول أكثر راديكالية ودائمة على المدى الطويل؟ في أقصى الحدود، هل تقوض ‘عالم VUCA’ مفهوم العولمة إلى حد كبير بحيث تبدأ ‘إعادة التصنيع’ و’التصنيع القريب’ و’التصنيع الصديق’ في الظهور كاستراتيجيات سلاسل إمداد رائجة (Hartman et al. 2017؛ Piatanesi و Arauzo-Carod 2019؛ Maihold 2022؛ Van Hassel et al. 2022؛ Javorcik et al. 2023)

مهما كانت الحلول قصيرة الأجل أو طويلة الأجل التي يتم تنفيذها لمواجهة الصعوبات الناجمة عن أزمة البحر الأحمر الحالية، نأمل أن تعزز هذه

التجربة مرة أخرى الحاجة إلى مرونة أكبر في سلاسل الإمداد (Tukamuhabwa et al. 2015) في مواجهة الاضطرابات الكبرى في عمليات الشحن العادية. ومع ذلك، يبقى أن نرى ما إذا كانت الدروس الأكثر أهمية التي تم تعلمها خلال جائحة COVID-19 يمكن أن تُستخدم بشكل جيد في تخفيف أسوأ الآثار المحتملة للأزمة الحالية.

References

Abdulla, K.A., and J.S.H. Singh. 2018. The Influence of Geography in Asymmetric Conflicts in Narrow Seas and the Houthi Insurgency in Yemen. Malaysian Journal of International Relations 6 (1): 84-90.

Al-Yadomi, H. 1991. The Strategic Importance of Bab Al-Mandab Strait. US Army War College, Pennsylvania, April 9th. https://apps.dtic.mil/sti/pdfs/ADA236804.pdf

Associated Press. 2024. Panama Canal Traffic Cut by More Than a Third Because of Drought. January 19th. https://apnews.com/article/panama-canal-global-trade-routes-drought-climate-change-bd76a 77825a2e8e751a24346f8fd54a9

Baltic Exchange. 2024. FBX Index January 2024: Expect Disruptions to Continue. January 11th. https:// www.balticexchange.com/en/news-and-events/news/guest-column/2024/expect-disruptions-to-conti nue.html

Bennett, N., and J. Lemoine. 2014. What VUCA Really Means for You. Harvard Business Review 92 (1/2): 1-7.

Bloomberg. 2024. Add Soaring Insurance Bills to Mounting Red Sea Trade Chaos. January 15th. https://www.bloomberg.com/news/articles/2024-01-15/add-soaring-insurance-bills-to-mount ing-red-sea-trade-chaos

Cariou, P., and T. Notteboom. 2023. Implications of COVID-19 on the US Container Port Distribution System: Import cargo Routing by Walmart and Nike. International Journal of Logistics Research and Applications 26 (11): 1536-1555.

Chen, J., T. Notteboom, X. Liu, H. Yu, N. Nikitakos, and C. Yang. 2019. The Nicaragua Canal: Potential Impact on International Shipping and Its Attendant Challenges. Maritime Economics & Logistics 21: 79-98.

Chen, K., S. Xu, and H. Haralambides. 2020. Determining Hub Port Locations and Feeder Network Designs: The Case of China-West Africa Trade. Transport Policy 86: 9-22.

Container News. 2024. 80% of All Container Ships on Suez Route Divert to Cape of Good Hope. January 9th. https://container-news.com/80-of-all-conta iner-ships-on-suez-route-divert-to-cape-of-good-hope/

Cullinane, K.P.B., and H. Haralambides. 2021. Global Trends in Maritime and Port Economics: The COVID-19 Pandemic and Beyond. Maritime Economics & Logistics 23: 369-380.

Cullinane, K.P.B., H. Haralambides, and T. Notteboom. 2023. Short-Term Effects and Longer-Term Impacts of the Covid-19 Pandemic on the International Shipping and Port Industries. International Journal of Transport Economics L (1/2): 45-88.

Economist Intelligence Unit. 2024. War Risks Raise Marine Insurance Premiums. January 12th. https:// www.eiu.com/n/war-risks-raise-marine-insurance-premiums/

Gunnarsson, B., and A. Moe. 2021. Ten Years of International Shipping on the Northern Sea Route. Arctic Review on Law and Politics 12: 4-30.

Guzansky, Y. and O. Eran. 2018. The Red Sea: An Old-New Arena of Interest. INSS Insight. No. 1068, June 24th. https://www.inss.org.il/publication/red-sea-old-new-arena-interest/

Haralambides, H.E. 2023. The State-of-Play in Maritime Economics and Logistics Research (20172023). Maritime Economics & Logistics. https://doi.org/10.1057/s41278-023-00265-x.

Al-Yadomi, H. 1991. The Strategic Importance of Bab Al-Mandab Strait. US Army War College, Pennsylvania, April 9th. https://apps.dtic.mil/sti/pdfs/ADA236804.pdf

Associated Press. 2024. Panama Canal Traffic Cut by More Than a Third Because of Drought. January 19th. https://apnews.com/article/panama-canal-global-trade-routes-drought-climate-change-bd76a 77825a2e8e751a24346f8fd54a9

Baltic Exchange. 2024. FBX Index January 2024: Expect Disruptions to Continue. January 11th. https:// www.balticexchange.com/en/news-and-events/news/guest-column/2024/expect-disruptions-to-conti nue.html

Bennett, N., and J. Lemoine. 2014. What VUCA Really Means for You. Harvard Business Review 92 (1/2): 1-7.

Bloomberg. 2024. Add Soaring Insurance Bills to Mounting Red Sea Trade Chaos. January 15th. https://www.bloomberg.com/news/articles/2024-01-15/add-soaring-insurance-bills-to-mount ing-red-sea-trade-chaos

Cariou, P., and T. Notteboom. 2023. Implications of COVID-19 on the US Container Port Distribution System: Import cargo Routing by Walmart and Nike. International Journal of Logistics Research and Applications 26 (11): 1536-1555.

Chen, J., T. Notteboom, X. Liu, H. Yu, N. Nikitakos, and C. Yang. 2019. The Nicaragua Canal: Potential Impact on International Shipping and Its Attendant Challenges. Maritime Economics & Logistics 21: 79-98.

Chen, K., S. Xu, and H. Haralambides. 2020. Determining Hub Port Locations and Feeder Network Designs: The Case of China-West Africa Trade. Transport Policy 86: 9-22.

Container News. 2024. 80% of All Container Ships on Suez Route Divert to Cape of Good Hope. January 9th. https://container-news.com/80-of-all-conta iner-ships-on-suez-route-divert-to-cape-of-good-hope/

Cullinane, K.P.B., and H. Haralambides. 2021. Global Trends in Maritime and Port Economics: The COVID-19 Pandemic and Beyond. Maritime Economics & Logistics 23: 369-380.

Cullinane, K.P.B., H. Haralambides, and T. Notteboom. 2023. Short-Term Effects and Longer-Term Impacts of the Covid-19 Pandemic on the International Shipping and Port Industries. International Journal of Transport Economics L (1/2): 45-88.

Economist Intelligence Unit. 2024. War Risks Raise Marine Insurance Premiums. January 12th. https:// www.eiu.com/n/war-risks-raise-marine-insurance-premiums/

Gunnarsson, B., and A. Moe. 2021. Ten Years of International Shipping on the Northern Sea Route. Arctic Review on Law and Politics 12: 4-30.

Guzansky, Y. and O. Eran. 2018. The Red Sea: An Old-New Arena of Interest. INSS Insight. No. 1068, June 24th. https://www.inss.org.il/publication/red-sea-old-new-arena-interest/

Haralambides, H.E. 2023. The State-of-Play in Maritime Economics and Logistics Research (20172023). Maritime Economics & Logistics. https://doi.org/10.1057/s41278-023-00265-x.

Haralambides, H.E. and O. Merk. 2020. The Belt and Road Initiative: Impacts on Global Maritime Trade Flows. International Transport Forum Discussion Papers, No. 2020/02, OECD Publishing, Paris.

Hartman, P.L., J.A. Ogden, J.R. Wirthlin, and B.T. Hazen. 2017. Nearshoring, Reshoring, and Insourcing: Moving Beyond the Total Cost of Ownership Conversation. Business Horizons 60 (3): 363-373.

Hokayem, E., and D.B. Roberts. 2016. The War in Yemen. Survival 58 (6): 157-186. https://doi.org/10. 1080/00396338.2016.1257202.

Hartman, P.L., J.A. Ogden, J.R. Wirthlin, and B.T. Hazen. 2017. Nearshoring, Reshoring, and Insourcing: Moving Beyond the Total Cost of Ownership Conversation. Business Horizons 60 (3): 363-373.

Hokayem, E., and D.B. Roberts. 2016. The War in Yemen. Survival 58 (6): 157-186. https://doi.org/10. 1080/00396338.2016.1257202.

Humpert, M. 2024. Northern Sea Route Saw Seven Containership Voyages in 2023, including Controversial Chinese Container Ship, High North News.

IMO. 2023. 2023 IMO Strategy on Reduction of GHG Emissions From Ships, Annex 1-Resolution MEPC.377(80), Marine Environment Protection Committee (MEPC), Adopted on 7 July 2023, London: International Maritime Organization.

International Energy Agency. 2023. Oil Market Report. https://www.iea.org/reports/oil-market-report-december-2023

Javorcik, B., L. Kitzmueller, H. Schweiger, and M.A. Yildirim. 2023. Economic costs of friend-shoring. Centre for Economic Studies IFO Institute Working Paper No. 10869. Munich.

Kent, Paul, and Hercules Haralambides. 2022. A Perfect Storm or an Imperfect Supply Chain? The US Supply Chain Crisis. Maritime Economics & Logistics. https://doi.org/10.1057/ s41278-022-00221-1.

Lee, T., and H.J. Kim. 2015. Barriers of Voyaging on the Northern Sea Route: A Perspective from SHIPPING COMPAnies. Marine Policy 62: 264-270.

Lee, H.L., V. Padmanabhan, and S. Whang. 1997. The Bullwhip Effect in Supply Chains. IEEE Engineering Management Review 43 (2): 108-117.

Maihold, G. 2022. A New Geopolitics of Supply Chains: The Rise of Friend-Shoring. Social Science Open Access Repository. https://nbn-resolving.org/urn:nbn:de:0168-ssoar-81700-2

NHK. 2024. Suzuki Suspends Plant in Hungary Over Houthi Attacks in the Red Sea. January 16th. https://www3.nhk.or.jp/nhkworld/en/news/20240116_26/#:~:text=Suzuki Motor says% 20it%20has,from%20January%2015%20to%2021

Nightingale, L. 2024. Red Sea Attacks Prompt 2m TEU Drop in Suez Boxship Traffic. Lloyds List. January 10th. https://www.lloydslist.com/LL1147891/Red-Sea-attacks-prompt-2m-teu-drop-in-Suez-boxship-traffic

Notteboom, T.E. 2012. Towards a New Intermediate Hub Region in Container Shipping? Relay and Interlining Via the Cape Route vs. the Suez Route. Journal of Transport Geography 22: 164-178.

Notteboom, T.E., T. Pallis, and J.P. Rodrigue. 2021. Disruptions and Resilience in Global Container Shipping and Ports: The COVID-19 Pandemic Versus the 2008-2009 Financial Crisis. Maritime Economics & Logistics 23: 179-210.

Notteboom, T.E., and J.P. Rodrigue. 2011. Challenges to and Challengers of the Suez Canal. Port Technology International: The Review of Advanced Technologies for Ports and Terminals World-Wide 51: 14-17.

Orkaby, A. 2021. The Red Sea and the Gulf of Aden. In Air Power in the Indian Ocean and the Western Pacific: Understanding Regional Security Dynamics, 1st ed., ed. H.M. Hensel. Abingdon: Routledge.

Peng Er, L. 2018. Thailand’s Kra Canal Proposal and China’s Maritime Silk Road: Between Fantasy and Reality? Asian Affairs: An American Review 45 (1): 1-17.

Piatanesi, B., and J.M. Arauzo-Carod. 2019. Backshoring and Nearshoring: An Overview. Growth and Change 50 (3): 806-823.

RANE Worldview. 2016. A New Threat to Red Sea Shipping. October 5th. https://worldview.stratfor.com/ article/new-threat-red-sea-shipping

Rasmussen, N. 2024. Record Deliveries Could Push Container Fleet Above 30 Million Teu in 2024. BIMCO Market Report. January 10th. https://www.bimco.org/news-and-trends/market-reports/shipp ing-number-of-the-week/20240110-snow

Reuters. 2023. Suez Canal Annual Revenue Hits Record USD9.4 Billion, Chairman Says. June 21st. https://www.reuters.com/world/africa/suez-canal-annual-revenue-hits-record-94-bln-chair man-2023-06-21/

Reuters. 2024a. Egypt’s Suez Canal Revenues Down

Reuters. 2024b. Tesla, Volvo Car Pause Output as Red Sea Shipping Crisis Deepens. January 13th. https://www.reuters.com/business/autos-transportation/tesla-berlin-suspend-most-produ ction-two-weeks-over-red-sea-supply-gap-2024-01-11/

Reuters. 2024c. Saudi Arabia Has Not Yet Joined BRICs-Minister. January 16th. https://www.reuters. com/world/saudi-arabia-has-not-yet-joined-brics-minister-2024-01-16/

Seadistance.net. 2024. Sea distance calculator. http://www.shiptraffic.net/2001/05/sea-distances-calcu lator.html

IMO. 2023. 2023 IMO Strategy on Reduction of GHG Emissions From Ships, Annex 1-Resolution MEPC.377(80), Marine Environment Protection Committee (MEPC), Adopted on 7 July 2023, London: International Maritime Organization.

International Energy Agency. 2023. Oil Market Report. https://www.iea.org/reports/oil-market-report-december-2023

Javorcik, B., L. Kitzmueller, H. Schweiger, and M.A. Yildirim. 2023. Economic costs of friend-shoring. Centre for Economic Studies IFO Institute Working Paper No. 10869. Munich.

Kent, Paul, and Hercules Haralambides. 2022. A Perfect Storm or an Imperfect Supply Chain? The US Supply Chain Crisis. Maritime Economics & Logistics. https://doi.org/10.1057/ s41278-022-00221-1.

Lee, T., and H.J. Kim. 2015. Barriers of Voyaging on the Northern Sea Route: A Perspective from SHIPPING COMPAnies. Marine Policy 62: 264-270.

Lee, H.L., V. Padmanabhan, and S. Whang. 1997. The Bullwhip Effect in Supply Chains. IEEE Engineering Management Review 43 (2): 108-117.

Maihold, G. 2022. A New Geopolitics of Supply Chains: The Rise of Friend-Shoring. Social Science Open Access Repository. https://nbn-resolving.org/urn:nbn:de:0168-ssoar-81700-2

NHK. 2024. Suzuki Suspends Plant in Hungary Over Houthi Attacks in the Red Sea. January 16th. https://www3.nhk.or.jp/nhkworld/en/news/20240116_26/#:~:text=Suzuki Motor says% 20it%20has,from%20January%2015%20to%2021

Nightingale, L. 2024. Red Sea Attacks Prompt 2m TEU Drop in Suez Boxship Traffic. Lloyds List. January 10th. https://www.lloydslist.com/LL1147891/Red-Sea-attacks-prompt-2m-teu-drop-in-Suez-boxship-traffic

Notteboom, T.E. 2012. Towards a New Intermediate Hub Region in Container Shipping? Relay and Interlining Via the Cape Route vs. the Suez Route. Journal of Transport Geography 22: 164-178.

Notteboom, T.E., T. Pallis, and J.P. Rodrigue. 2021. Disruptions and Resilience in Global Container Shipping and Ports: The COVID-19 Pandemic Versus the 2008-2009 Financial Crisis. Maritime Economics & Logistics 23: 179-210.

Notteboom, T.E., and J.P. Rodrigue. 2011. Challenges to and Challengers of the Suez Canal. Port Technology International: The Review of Advanced Technologies for Ports and Terminals World-Wide 51: 14-17.

Orkaby, A. 2021. The Red Sea and the Gulf of Aden. In Air Power in the Indian Ocean and the Western Pacific: Understanding Regional Security Dynamics, 1st ed., ed. H.M. Hensel. Abingdon: Routledge.

Peng Er, L. 2018. Thailand’s Kra Canal Proposal and China’s Maritime Silk Road: Between Fantasy and Reality? Asian Affairs: An American Review 45 (1): 1-17.

Piatanesi, B., and J.M. Arauzo-Carod. 2019. Backshoring and Nearshoring: An Overview. Growth and Change 50 (3): 806-823.

RANE Worldview. 2016. A New Threat to Red Sea Shipping. October 5th. https://worldview.stratfor.com/ article/new-threat-red-sea-shipping

Rasmussen, N. 2024. Record Deliveries Could Push Container Fleet Above 30 Million Teu in 2024. BIMCO Market Report. January 10th. https://www.bimco.org/news-and-trends/market-reports/shipp ing-number-of-the-week/20240110-snow

Reuters. 2023. Suez Canal Annual Revenue Hits Record USD9.4 Billion, Chairman Says. June 21st. https://www.reuters.com/world/africa/suez-canal-annual-revenue-hits-record-94-bln-chair man-2023-06-21/

Reuters. 2024a. Egypt’s Suez Canal Revenues Down

Reuters. 2024b. Tesla, Volvo Car Pause Output as Red Sea Shipping Crisis Deepens. January 13th. https://www.reuters.com/business/autos-transportation/tesla-berlin-suspend-most-produ ction-two-weeks-over-red-sea-supply-gap-2024-01-11/

Reuters. 2024c. Saudi Arabia Has Not Yet Joined BRICs-Minister. January 16th. https://www.reuters. com/world/saudi-arabia-has-not-yet-joined-brics-minister-2024-01-16/

Seadistance.net. 2024. Sea distance calculator. http://www.shiptraffic.net/2001/05/sea-distances-calcu lator.html

Schøyen, H., and S. Bråthen. 2011. The Northern Sea Route Versus the Suez Canal: Cases from Bulk Shipping. Journal of Transport Geography 19 (4): 977-983.

Solvang, H.B., S. Karamperidis, N. Valantasis-Kanellos, and D.W. Song. 2018. An Exploratory Study on the Northern Sea Route as an Alternative Shipping Passage. Maritime Policy & Management 45 (4): 495-513.

Theocharis, D., V.S. Rodrigues, S. Pettit, and J. Haider. 2019. Feasibility of the Northern Sea Route: The Role of Distance, Fuel Prices, Ice Breaking Fees and Ship Size for the Product Tanker Market. Transportation Research Part E: Logistics and Transportation Review 129: 111-135.

Tseng, P.H., and K. Cullinane. 2018. Key Criteria Influencing the Choice of Arctic Shipping: A Fuzzy Analytic Hierarchy Process Model. Maritime Policy & Management 45 (4): 422-438.

Tseng, P.H., and N. Pilcher. 2022. Examining the Opportunities and Challenges of the Kra Canal: A PESTELE/SWOT Analysis. Maritime Business Review 7 (2): 161-174.

Tukamuhabwa, B.R., M. Stevenson, J. Busby, and M. Zorzini. 2015. Supply Chain Resilience: Definition, Review and Theoretical Foundations for Further Study. International Journal of Production Research 53 (18): 5592-5623.

UNCTAD. 2024. Red Sea, Black Sea and Panama Canal: UNCTAD Raises Alarm on Global Trade Disruptions. January 26th. https://unctad.org/news/red-sea-black-sea-and-panama-canal-unctad-raises-alarm-global-trade-disruptions

US Department of Defense. 2023. Statement from Secretary of Defense Lloyd J. Austin III on Ensuring Freedom of Navigation in the Red Sea, 18 December 2023.

US Department of Transportation. 2023. Transportation Statistics Annual Report 2023, Bureau of Transportation Statistics, Washington, DC. https://doi.org/10.21949/1529944

US Energy Information Administration. 2023. Red Sea Chokepoints are Critical for International Oil and Natural Gas Flows. December 4th. https://www.eia.gov/todayinenergy/detail.php?id=61025

Van Hassel, E., T. Vanelslander, K. Neyens, H. Vandeborre, D. Kindt, and S. Kellens. 2022. Reconsidering Nearshoring to Avoid Global Crisis Impacts: Application and Calculation of the Total Cost of Ownership for Specific Scenarios. Research in Transportation Economics 93: 101089.

Wright, R. 2024. Red Sea Security Fears Cut Container Shipments Through Suez Canal. Financial Times. January 10th. https://www.ft.com/content/007e8ec6-7124-4e11-b40f-9863bf64df0c

Verny, J., and C. Grigentin. 2009. Container Shipping on the Northern Sea Route. International Journal of Production Economics 122 (1): 107-117.

Xeneta. 2024a. Red Sea Crisis: Latest data from Xeneta Forecasts Ocean Freight Shipping Rates are Set to Rise Further in February. January 23rd. https://www.xeneta.com/news/red-sea-crisis-latest-data-from-xeneta-forecasts-ocean-freight-shipping-rates-are-set-to-rise-further-in-february

Xeneta. 2024b. Shippers must act quickly to protect supply chains amid surging ocean freight rates and market confusion. January 11th. https://www.xeneta.com/blog/red-sea-crisis-shippers-must-act-quickly-to-protect-supply-chains-amid-surging-ocean-freight-rates-and-market-confusion#:~:text= The%201atest%20data%20from%20Xeneta,Mediterranean%20have%20increased%20by%20118%25

Xu, H., Z. Yin, D. Jia, F. Jin, and H. Ouyang. 2011. The Potential Seasonal Alternative of Asia-Europe Container Service Via Northern Sea Route Under the Arctic Sea Ice Retreat. Maritime Policy & Management 38 (5): 541-560.

Yip, T.L., and M.C. Wong. 2015. The Nicaragua Canal: Scenarios of Its Future Roles. Journal of Transport Geography 43: 1-13.

Zhu, S., X. Fu, A.K. Ng, M. Luo, and Y.E. Ge. 2018. The Environmental Costs and Economic Implications of Container Shipping on the Northern Sea Route. Maritime Policy & Management 45 (4): 456-477.

Solvang, H.B., S. Karamperidis, N. Valantasis-Kanellos, and D.W. Song. 2018. An Exploratory Study on the Northern Sea Route as an Alternative Shipping Passage. Maritime Policy & Management 45 (4): 495-513.

Theocharis, D., V.S. Rodrigues, S. Pettit, and J. Haider. 2019. Feasibility of the Northern Sea Route: The Role of Distance, Fuel Prices, Ice Breaking Fees and Ship Size for the Product Tanker Market. Transportation Research Part E: Logistics and Transportation Review 129: 111-135.

Tseng, P.H., and K. Cullinane. 2018. Key Criteria Influencing the Choice of Arctic Shipping: A Fuzzy Analytic Hierarchy Process Model. Maritime Policy & Management 45 (4): 422-438.

Tseng, P.H., and N. Pilcher. 2022. Examining the Opportunities and Challenges of the Kra Canal: A PESTELE/SWOT Analysis. Maritime Business Review 7 (2): 161-174.

Tukamuhabwa, B.R., M. Stevenson, J. Busby, and M. Zorzini. 2015. Supply Chain Resilience: Definition, Review and Theoretical Foundations for Further Study. International Journal of Production Research 53 (18): 5592-5623.

UNCTAD. 2024. Red Sea, Black Sea and Panama Canal: UNCTAD Raises Alarm on Global Trade Disruptions. January 26th. https://unctad.org/news/red-sea-black-sea-and-panama-canal-unctad-raises-alarm-global-trade-disruptions

US Department of Defense. 2023. Statement from Secretary of Defense Lloyd J. Austin III on Ensuring Freedom of Navigation in the Red Sea, 18 December 2023.

US Department of Transportation. 2023. Transportation Statistics Annual Report 2023, Bureau of Transportation Statistics, Washington, DC. https://doi.org/10.21949/1529944

US Energy Information Administration. 2023. Red Sea Chokepoints are Critical for International Oil and Natural Gas Flows. December 4th. https://www.eia.gov/todayinenergy/detail.php?id=61025

Van Hassel, E., T. Vanelslander, K. Neyens, H. Vandeborre, D. Kindt, and S. Kellens. 2022. Reconsidering Nearshoring to Avoid Global Crisis Impacts: Application and Calculation of the Total Cost of Ownership for Specific Scenarios. Research in Transportation Economics 93: 101089.

Wright, R. 2024. Red Sea Security Fears Cut Container Shipments Through Suez Canal. Financial Times. January 10th. https://www.ft.com/content/007e8ec6-7124-4e11-b40f-9863bf64df0c

Verny, J., and C. Grigentin. 2009. Container Shipping on the Northern Sea Route. International Journal of Production Economics 122 (1): 107-117.

Xeneta. 2024a. Red Sea Crisis: Latest data from Xeneta Forecasts Ocean Freight Shipping Rates are Set to Rise Further in February. January 23rd. https://www.xeneta.com/news/red-sea-crisis-latest-data-from-xeneta-forecasts-ocean-freight-shipping-rates-are-set-to-rise-further-in-february

Xeneta. 2024b. Shippers must act quickly to protect supply chains amid surging ocean freight rates and market confusion. January 11th. https://www.xeneta.com/blog/red-sea-crisis-shippers-must-act-quickly-to-protect-supply-chains-amid-surging-ocean-freight-rates-and-market-confusion#:~:text= The%201atest%20data%20from%20Xeneta,Mediterranean%20have%20increased%20by%20118%25

Xu, H., Z. Yin, D. Jia, F. Jin, and H. Ouyang. 2011. The Potential Seasonal Alternative of Asia-Europe Container Service Via Northern Sea Route Under the Arctic Sea Ice Retreat. Maritime Policy & Management 38 (5): 541-560.

Yip, T.L., and M.C. Wong. 2015. The Nicaragua Canal: Scenarios of Its Future Roles. Journal of Transport Geography 43: 1-13.

Zhu, S., X. Fu, A.K. Ng, M. Luo, and Y.E. Ge. 2018. The Environmental Costs and Economic Implications of Container Shipping on the Northern Sea Route. Maritime Policy & Management 45 (4): 456-477.

Publisher’s Note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

- Hercules Haralambides

haralambides@ese.eur.nl

Theo Notteboom

theo.notteboom@ugent.be

Kevin Cullinane

kevin.cullinane@gu.se

Faculty of Law and Criminology, Maritime Institute, Ghent University, Ghent, Belgium

Department of Transport and Regional Economics, Faculty of Business and Economics, University of Antwerp, Antwerp, Belgium

Faculty of Sciences, Antwerp Maritime Academy, Antwerp, Belgium

4 School of Maritime Economics and Management, Dalian Maritime University, Dalian, China

5 Université Paris 1, Panthéon Sorbonne, France

Erasmus University, Rotterdam, The Netherlands

7 School of Business, Economics and Law, University of Gothenburg, Göteborg, Sweden Brazil, Russia, India, China, South Africa.

Most notably, the Houthis launched a cruise missile attack against a US destroyer in 2016, but the missile was intercepted before reaching its target (RANE Worldview 2016). Presently, 20 countries are partaking, some anonymously. With the exception of Greece, the European South (Spain, Italy, France) declined the US invitation to join; the ‘north’ is represented by Denmark and The Netherlands only. The strategic significance of chokepoints could not be better exemplified than by the Pass of Thermopylae where, in the Second Persian War of 480 BC, the Spartan King Leonidas, with 300 of his men, managed to fend off the vast armies of Xerxes I.

Interestingly, the current Thai government is reviving the 2015 plan of its predecessor, inviting instead private investor interest for a 90 km landbridge, at a predicted cost of USD28 billion, including the construction of two mega-seaports (Ranong and Chumphon) at the two ends of the Isthmus. When the Canal operates at full capacity, it can handle 40 transits a day. With all the measures the Panama Canal Authority (PCA) has taken because of the drought, that number had decreased to only 22 in late 2023. In mid-January 2024, the canal’s capacity increased marginally to 24 daily transits (PCA data). The problem, obviously, is that the water situation results in draft restrictions, so the quantity of cargo that ships can carry is limited, compared to earlier times. Some shipping lines and shippers have opted for alternative routes (such as the Suez route or the US land-bridge) to deal with the lower overall capacity of the Canal, the lower payload of vessels caused by draft restrictions, and the strong increase in Panama Canal transit fees resulting from PCA’s auction-based pricing system. When a container is ‘rolled,’ it has not been loaded onto the vessel it was meant to sail on. Container rollings can have various reasons such as vessel overbooking, port call cancelation, vessel weight issues, documentation issues, and so on.

Suez Canal transit fees range between USD 750,000 and 1 million in the case of a one-way transit of a large containership. Notwithstanding India’s obvious interest in the project, the country has never relinquished her interest in Russia’s International North South Transport Corridor (INSTC) which, starting probably from the Iranian Gulf port of Chabahar, continues north, over 7000 km , eventually reaching Moscow, calling on its way at Tehran and Baku (Azerbaijan) and, from Moscow, branching out westwards to Turkey.

Journal: Maritime Economics & Logistics, Volume: 26, Issue: 1

DOI: https://doi.org/10.1057/s41278-024-00287-z

Publication Date: 2024-02-20

DOI: https://doi.org/10.1057/s41278-024-00287-z

Publication Date: 2024-02-20

The Red Sea Crisis: ramifications for vessel operations, shipping networks, and maritime supply chains

Accepted: 14 February 2024 / Published online: 20 February 2024

© The Author(s), under exclusive licence to Springer Nature Limited 2024

© The Author(s), under exclusive licence to Springer Nature Limited 2024

1 Introduction

The attack of Hamas on Israel of October 7, 2023, and the military response of the latter in Gaza have made news headlines for much of the last quarter of 2023 and early 2024. The international community has attempted to prevent escalation and the spreading of the conflict to other parts of the Middle East and the wider world. Despite those efforts, a major security situation emerged in mid-November in the Red Sea and the Strait of Bab al-Mandab more specifically (map in Fig. 1), when Houthi Rebels based in Yemen started to target international shipping transiting through the region. In a matter of weeks, the situation escalated, adversely affecting both shipping and trade.

The Red Sea crisis is yet another major disruption affecting the dynamics in shipping and logistics. In the past few years, interoceanic passages and routes have been significantly affected by a series of weather anomalies (e.g., the drought which has reduced the capacity of the Panama Canal by

Fig. 1 The Red Sea and the Strait of Bab al-Mandab as part of the routing alternatives on the Asia-North Europe trade and Asia-Americas trade. IMEC India-Middle East-Europe Corridor, ECNA East Coast North America, ECSA East Cost South America, WCNA West Coast North America. Source The authors

accidents and vessel groundings (e.g., the ‘Ever Given’ incident, when the Suez Canal was blocked for six days in March 2021, at a cost to trade of USD10 billion a day).

This editorial provides not only insights into the course of events which have occurred during the Red Sea crisis, but it also analyzes the short-term-and probably longer-term-impacts of the Red Sea crisis on vessel operations and shipping networks; freight rates and pricing practices; and on global supply chains. The Editorial was finalized on February 13, 2024. As the Red Sea crisis is still unfolding at the time of writing, the Editorial focuses primarily on the early impacts of the crisis on the shipping industry and global supply chains. The full impacts can only be known with some degree of accuracy once the crisis has come to an end or has been contained in such a way that the levels of uncertainty and insecurity faced by shipping and trade have been reduced to acceptable levels. However, it remains unclear under what conditions shipping lines will consider the Red Sea as a safe passage. Will they resume vessel transits when the Red Sea is without incidents for

2 Prelude and course of events

The current crisis in the Red Sea has been brewing for some time, with its origins in the ongoing civil war in Yemen between the internationally recognized government, operating out of Saudi Arabia, and the Houthi militia. While the former is primarily backed by Saudi Arabia and an international coalition, the latter has the support of both Iran and troops allegiant to the former President Ali Abdullah Saleh (Guzansky and Eran 2018).

The roots of the civil war in Yemen are far too complex to analyze in this editorial; this would be beyond our scope anyway. However, one might not be totally wrong in seeing this conflict which, in ten years, has claimed the lives of more than a quarter of a million people due to the hostilities and their consequences, as the terrain of Saudi-Iranian rivalries. With the acceptance of the two countries into the BRICS

In 2014, the Houthi militia succeeded in capturing the main ports and cities along Yemen’s Red Sea coast. What started as a civil war, confined solely to Yemen, soon escalated into a regional conflict, with a Saudi-led military intervention in support of the government in March 2015 (Hokayem and Roberts 2016). This intervention was primarily aimed at ensuring the security of the Bab al-Mandab strait: a chokepoint at the southern entrance to the Red Sea (see Fig. 1). Shared by Yemen, Eritrea and Djibouti, the Bab al-Mandab chokepoint is the Cerberus that ‘guards’ the entrance to the Red Sea. The Strait has a width of something less than 30 km and it is divided into two channels by Perim Island (Al-Yadomi 1991). The Strait makes the strategic importance of the Gulf of Aden even more pronounced, with most major powers, starting with China (in Djibouti) and the US, maintaining a military presence in the Gulf which has traditionally been plagued by high levels of piracy activity and illegal arms trafficking over the dark web and in other ways. International cooperation initiatives and regional laws (e.g., Djibouti’s) have been rather unsuccessful in improving the security situation in the Gulf.

The relative success of the Saudi military intervention in 2015 has not, however, prevented the Houthi militia from engaging in maritime reprisals since that time. Using drone boats, cruise missiles, speedboats, and mines (Knights and Mello 2015; Abdullah and Singh 2018), the narrowness of the Bab al-Mandab strait has been utilized by the Houthi militia to instigate sporadic attacks mainly, but not exclusively,

When Israel started its military action against Hamas in Gaza in mid-October 2023, Muslim countries and groups such as Hezbollah did not declare war on Israel. The notable exception was the Ansar Allah (Partisans of God) group: Houthi rebels who control the west of Yemen including most of its Red Sea coast near the Strait of Bab Al-Mandab. In early November 2023, the Houthi launched long-range ballistic missiles at Israel, but all were intercepted by the US and the Saudi military. From

mid-November 2023, the Houthi militia started to focus more on attacking merchant vessels. Initially, hijacking actions were conducted such as on the roro vessel Galaxy Leader. This was soon followed by attacks on merchant vessels traveling through the lower Red Sea and the Strait of Bab Al-Mandab, using drones, missiles, and gunmen on speedboats. While the Houthi initially claimed they were only targeting merchant vessels traveling to or from Israel or of Israeli ownership, it soon became evident that also ships of countries supportive of Israeli actions in Gaza were being attacked.

By mid-December 2023, security threats escalated to the point where Maersk, MSC, BP, and other shipping groups suspended canal passages or started to reroute traffic via the Cape of Good Hope. At the same time, a maritime coalition to defend shipping against attacks was initiated. Table 1 provides an overview of the main incidents and events during the Red Sea crisis, listing the many (mostly failed) attacks on cargo ships. When the lack of security in the region started to hurt international shipping and trade, a growing international reaction emerged, led by the US. A key statement was made on December 18, 2023, by US Secretary of Defense Lloyd Austin, explicitly referring to the freedom of navigation and resulting in the establishment of Operation Prosperity Guardian:

The recent escalation in reckless Houthi attacks originating from Yemen threatens the free flow of commerce, endangers innocent mariners, and violates international law. The Red Sea is a critical waterway that has been essential to freedom of navigation and a major commercial corridor that facilitates international trade. Countries that seek to uphold the foundational principle of freedom of navigation must come together to tackle the challenge posed by this non-state actor launching ballistic missiles and unmanned aerial vehicles (UAVs) at merchant vessels from many nations lawfully transiting international waters. (U.S. Department of Defence, 2023).

The situation escalated further in early January 2024, with a massive Houthi attack on January 10, followed on January 12 by the first counterstrike by air on Yemen territory by US and UK military forces. Between mid-November and midFebruary, some 40 Houthi attacks have been carried out on vessels transiting the southern Red Sea and the Gulf of Aden. Damage on ships has been minimal in most cases, mainly thanks to the interception and neutralization of a large number of Houthi missiles, drones, and speedboats by warships in the region. By the third week of January, the attacks were spreading in terms of both geography (i.e., no longer only in the southern part of the Red Sea but also in the Gulf of Aden) and the scope of the targets (i.e., also targeting naval vessels). The expanding geographical scope of the risk zone makes it increasingly difficult for the navies, who are having to spread their already limited assets over a wider area.

Table 1 Key incidents and events during the Red Sea crisis (situation until February 12, 2024).

| Actions by HR (Houthi rebels) | Course of events Red Sea crisis | Counter actions |

| Late Oct-2023 | HR declare war on Israel | |

| Early Nov-23 | Ineffective long-range ballistic missile attacks at Israel | |

| 19-Nov-2023 | Roro ship Galaxy Leader (NYK): Hijacking, 25 crew members held hostage | |

| 3-Dec-2024 | Three ships (among which bulk carrier Unity Explorer and container ship of OOCL): massive missile attack | |

| 13-Dec-2023 | Chemical tanker Ardmore Encounter: Gunmen on speedboat and two missiles | |

| A number of container carriers announce to (temporarily) halt Red Sea transits or divert vessels via the Cape route | 13-Dec-2023 | |

| 14-Dec-2023 | Container ship Maersk Gibraltar: near-misss missile attack | |

| 15-Dec-2023 | Container ship Al Jasrah (Hapag-Lloyd): fire on board due to missile strike ; Container ship MSC Palatium III: hit by missile | |

| Establishment of “Operation Prosperity Guardian”, a multinational initiative focusing on security in the Red Sea (US, UK, Bahrain, Canada, France, Italy, Netherlands, Norway, Seychelles and Spain) | 18-Dec-2023 | |

| French navy starts escorting French cargo ships through the Red Sea | 22-Dec-2023 | |

| 23-Dec-2023 | Tankers Sai Baba (hit), MV Chem Pluto (hit) and Blaamanen (near-hit): drone attacks | |

| 27-Dec-2024 | Container ship MSC United VIII: unsuccesful attack ; 12 attack drones, 3 anti-ship missiles and 2 land-attack cruise missiles shot down | |

| 28-Dec-2023 | 1 drone and 1 anti-ship ballistic missile intercepted by US navy | |

| 30/31-Dec-2023 | Container ship Maersk Hangzhou: unsuccesful missile and speedboat attacks two days in a row | |

| UK defense secretary hints to direct military action against HR in Yemen | 1-Jan-2024 | |

| 2-Jan-2024 | Military tension in the region increases with arrival of frigate Alborz of Iran | |

| 3-Jan-2024 | Container ship CMA CGM Tage: unsuccesful attack with 2 anti-ship ballistic missiles | |

| A coalition of 12 countries issues a firm warning if HR continue the attacks | 4-Jan-2024 | |

| 5-Jan-2024 | HR drone boat with explosives detonated: no hits or damage | |

| 7-Jan-2024 | Drone shot down by US destroyer; suspicous approach of small boats | |

| Cosco announces that they suspend liner services to Israeli ports for the time being | 8-Jan-2024 | |

| Unconfirmed news that some shipping lines are entering agreements with HR to avoid attacks | 9-Jan-2024 |

| Table 1 (continued) | ||

| Actions by HR (Houthi rebels) | Course of events Red Sea crisis | Counter actions |

| 10-Jan-2024 | Large HR attack neutralized by US military: 18 drones, 2 anti-ship cruise missiles and one anti-ship ballastic missile | since 12-Jan-2024 |

| First of a series of aircraft and missile attacks by US and UK military forces on HR locations in Yemen targeting radar systems, and storage and launch sites of drones and missiles. | ||

| 12-Jan-2024 | Khalissa: possible missile attack | |

| 13-Jan-2024 | HR consider all US and UK ships as hostile targets, not only ships with ties to Israel. | |

| 14-Jan-2024 | US Destroyer USS Laboon: unsuccessful anti-ship cruise missile attack | |

| 15-Jan-2024 | Bulk carrier Gibraltar Eagle: hit by an anti-ship missile | |

| 16-Jan-2024 | Zografia: possible missile attack | |

| 17-Jan-2024 | Bulk carrier Genco Picardy: hit by drone | |

| 19-Jan-2024 | Chemical tanker Chem Ranger: unsuccesful anti-ship missile attack 2M partners MSC and Maersk change Asia-Europe and trans-Pacific network with new rotations around the Cape | |

| 24-Jan-2024 | ||

| 24-Jan-2024 | US-flagged container vessels Maersk Detroit and Maersk Chesapeake: unsuccesful anti-ship missile attack; Bulk carrier Tomahawk: unsuccessful drone attack | |

| 26-Jan-2024 | Product tanker Marlin Luanda: missile attack in Gulf of Aden; signficant fire on board extinguished a day later | |

| 1-Feb-2024 | Container ship Koi (CMA CGM): missile attack claimed by HR | |

| 6-Feb-2024 | Bulk carrier Star Nasia and cargo ship Morning Tide: missile attack; minor damage to Star Nasia | |

| 12-Feb-2024 | Bulk carrier Star Iris: hit by missile attack | |

Source The authors, based on mainstream and specialized news reports.

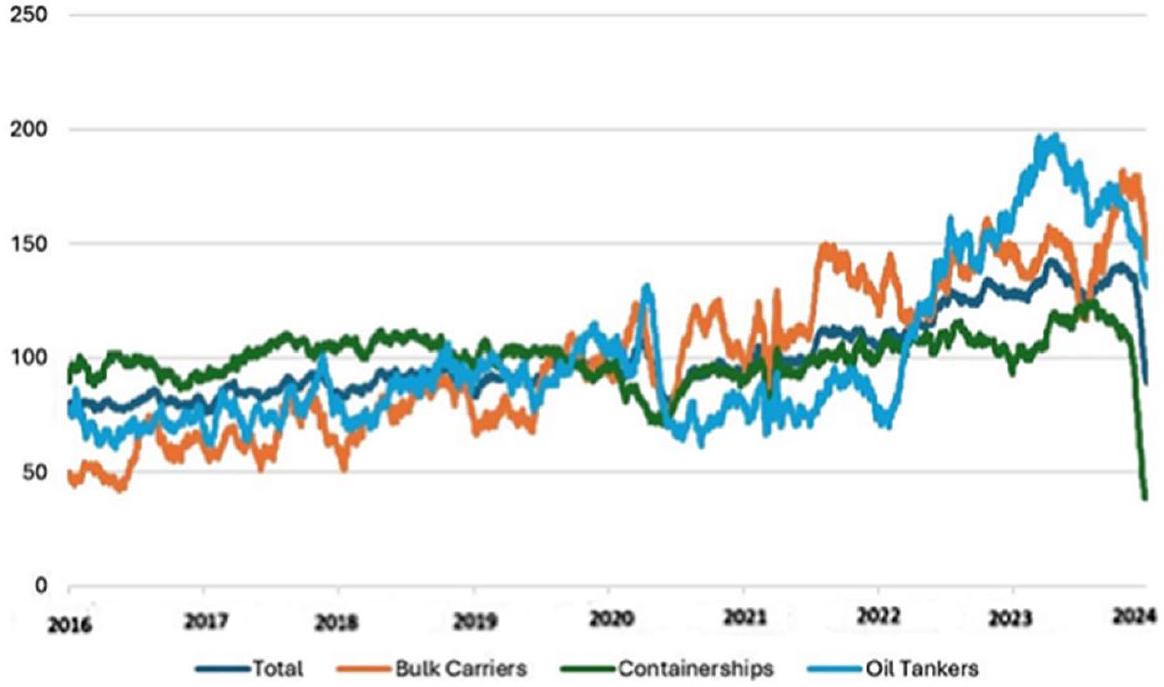

Fig. 2 Index of Daily Transits of the Suez Canal by Vessel Type 2016-2024 (Average value

The threat of retaliations from both sides has brought security concerns into a new phase. The Houthi militia-as certain analysts foresee-might even aim for a direct confrontation with the US. Such an escalation in the Red Sea crisis could undermine the ongoing peace talks between the Houthi and Saudi Arabia who, as mentioned earlier, have been involved in a bloody war since 2015. Concerns also persist that the situation could escalate still further if a successful Houthi attack were to result in fatalities on board vessels and/or the sinking of cargo ships transiting the Red Sea. However, the security situation could improve significantly overnight, in case an agreement is reached, between all parties concerned, on a longer-term ceasefire in Gaza.

3 Supply chain impacts

The Red Sea is one of the world’s major interoceanic trade passages with two entries: the Suez Canal in the North and the Bab al-Mandab Strait in the south. According to the US Energy Information Administration (2023), an annual average of 8.8 million barrels of oil shipments pass through the Bab al-Mandab strait each day, representing

Table 2 Impact of Cape rerouting on sailing distance, total ship round voyage time, and emissions for a typical Asia-North Europe weekly liner service

| Unit | Red Sea/ Suez route | Cape route | Increase (%) | |

| Total roundvoyage sailing distance | nm | 24000 | 31000 | 29.2 |

| Average sailing speed | kn | 16 | 17 | 6.3 |

| Average total port time per call | days | 1.7 | 1.7 | |

| Number of Asian port calls | no. | 5 | 5 | |

| Number of North European port calls | no. | 4 | 4 | |

| Total sailing time | days | 62.5 | 76.0 | 21.6 |

| Total port time | days | 15.3 | 15.3 | |

| Total roundvoyage time | days | 77.8 | 91.3 | 17.3 |

| Required number of vessels for weekly service | no. | 11 | 13 | 17.3 |

A vessel speed increase from 16 to 17 knots typically leads to a

Source The authors

the full impact of the Red Sea crisis on shipping and global supply chains is yet to be seen, businesses and shipping lines are trying, as far as possible, to mitigate the potential logistics ramifications of the crisis. This section explores the major current and potential future impacts of the Red Sea crisis by examining (a) the impacts on vessel operations and shipping network configurations, (b) changes in freight rates and surcharge practices, and (c) broader ramifications for global supply chains.

Source The authors

the full impact of the Red Sea crisis on shipping and global supply chains is yet to be seen, businesses and shipping lines are trying, as far as possible, to mitigate the potential logistics ramifications of the crisis. This section explores the major current and potential future impacts of the Red Sea crisis by examining (a) the impacts on vessel operations and shipping network configurations, (b) changes in freight rates and surcharge practices, and (c) broader ramifications for global supply chains.

3.1 Vessel rerouting