الأذكى هو الأكثر خضرة: هل يمكن أن تحسن التصنيع الذكي أداء الشركات في مجال البيئة والمجتمع والحوكمة؟ Smarter is greener: can intelligent manufacturing improve enterprises’ ESG performance?

الأذكى هو الأكثر خضرة: هل يمكن أن تحسن التصنيع الذكي أداء الشركات في مجال البيئة والمجتمع والحوكمة؟

دا قاو, لينفانغ تان & يوي تشين

البيئة، الاجتماعية، والحكومة (ESG) تتماشى بشكل كبير مع أهداف “الكربون المزدوج” التي اقترحتها الصين وأصبحت مؤشراً مهماً لقياس التنمية عالية الجودة للمؤسسات. تستكشف هذه الدراسة تأثير التصنيع الذكي على أداء ESG للشركات وآلياته المحتملة. باستخدام مجموعة بيانات الشركات المدرجة في السوق الصينية من 2009 إلى 2021، نتعامل مع برامج التصنيع الذكي التجريبية (IMPP) كاختبار شبه طبيعي ونستخدم نموذج الفرق في الفرق المتقطع للتحليل التجريبي. تظهر النتائج أن أداء ESG للشركات يتحسن بشكل ملحوظ بعد المشاركة في IMPP، وتؤكد اختبارات الدواء الوهمي والتوازن الانتروبي النتائج بشكل أكبر. يظهر تحليل الآلية أن IMPP يعمل بطريقتين رئيسيتين: تعزيز الابتكار الأخضر للمؤسسات وتقليل سوء تخصيص الموارد المالية. يظهر تحليل التباين أن IMPP يحسن بشكل كبير أداء ESG للمؤسسات غير المملوكة للدولة، والتكنولوجيا العالية، والمشاريع الثقيلة الملوثة. بالإضافة إلى ذلك، يحسن IMPP إنتاجية العامل الإجمالي الأخضر للمؤسسات ويحقق فوائد اقتصادية كبيرة. لهذه الدراسة آثار سياسية بعيدة المدى لتعزيز التنمية المدفوعة بالجودة في صناعة التصنيع الصينية والتنمية المستدامة للمؤسسات.

مقدمة

تحت أهداف “ذروة الكربون” و”حياد الكربون” التي اقترحتها الحكومة الصينية، أصبح كيفية تخفيف قيود الموارد وتحقيق التنمية الاقتصادية المستدامة قضية مهمة (تشو وآخرون، 2022a، باي وآخرون، 2024). باعتبارها لاعبين رئيسيين في السوق، تمثل المؤسسات قوة أساسية في تنفيذ مفهوم التنمية الخضراء وقد تم الاهتمام بأدائها في ESG على نطاق واسع (جيانوبولوس وآخرون، 2022؛ قاو وآخرون، 2024a، 2024c، موسى وآخرون، 2024). وجدت الدراسات الحالية التأثير العميق لأداء ESG على الأداء المالي وعدم اليقين في السوق (موسى وإلمارزوقي، 2023؛ موسى وإلمارزوقي، 2024a؛ موسى وإلمارزوقي، 2024b). ومع ذلك، لا تزال ممارسة ESG تواجه مشاكل مثل ارتفاع تكلفة المدخلات وعدم اليقين في المخرجات، مما يؤدي إلى نقص في المدخلات الفعلية لـ ESG. كيف يمكن تحفيز دافع المؤسسات لتوسيع استثمارات ESG وتعزيز أداء ESG أصبح مصدر قلق عاجل في المجالات الأكاديمية والعملية.

في الوقت نفسه، يؤدي التصنيع الذكي، كمنتج للتكامل العميق بين تكنولوجيا المعلومات وتقنيات التصنيع، إلى ترقية صناعة التصنيع والتنمية المستدامة للمؤسسات (لي وبرانستتر، 2024). مقارنةً بالتحكم التلقائي في معدات أو خطوط إنتاج فردية بناءً على برمجة مسبقة، فإن مزايا التصنيع الذكي في اتخاذ قرارات الإنتاج لا يمكن مقارنتها. على سبيل المثال، تستفيد ممارسة تطبيق الصناعة 4.0 في مصنع بوش في ألمانيا من تقنيات تحديد الهوية بتردد الراديو وغيرها من تقنيات إنترنت الأشياء للتواصل مع أنظمة المعلومات الإدارية مثل تخطيط موارد المؤسسات، وإدارة دورة حياة المنتج، وإدارة سلسلة التوريد (دي باولا فيريرا وآخرون، 2022؛ بيسواس وآخرون، 2024). يتيح هذا التكامل السلس عبر سلسلة التوريد من المنبع إلى المصب تدفق البيانات تلقائيًا في الإنتاج، مما يحسن كفاءة التخصيص ويقلل من هدر الموارد. لذلك، يمكن أن يعزز التصنيع الذكي أداء ESG من خلال تحسين شفافية المعلومات وكفاءة استخدام الموارد، وتعزيز تآزر سلسلة التوريد، وتلبية توقعات أصحاب المصلحة بشأن التنمية المستدامة.

على وجه التحديد، يمكّن التصنيع الذكي جمع البيانات في الوقت الحقيقي ومشاركة المعلومات عبر سلسلة التوريد من خلال دمج المعدات، وخطوط الإنتاج، وأنظمة التصنيع. من منظور نظرية عدم تماثل المعلومات، تعمل هذه الشفافية للمعلومات على تحسين كفاءة التعاون في سلسلة التوريد ويمكن أن تحسن أداء ESG للمؤسسات (قاو وآخرون، 2024b). بالإضافة إلى ذلك، يمكن لنظام التصنيع الذكي إجراء تعدين وتحليل عميق لبيانات الإنتاج لتحقيق اتخاذ قرارات أكثر دقة، مما يمكن أن يقلل من الهدر (هوانغ وآخرون، 2022). من منظور نظرية أصحاب المصلحة، لا تلبي الممارسات المذكورة أعلاه توقعات أصحاب المصلحة مثل المستهلكين، والمستثمرين، والجهات التنظيمية بشأن حماية البيئة فحسب، بل يمكنها أيضًا تعزيز أداء ESG للمؤسسات من خلال تحسين كفاءة استخدام الموارد.

ومع ذلك، تفتقر الأدبيات الحالية إلى تحليلات تجريبية مفصلة حول نتائج ESG للتصنيع الذكي على مستوى الشركات. أكدت بعض الدراسات أن التصنيع الذكي يمكن أن يعزز استثمار الشركات في التكنولوجيا ومعالجة المعلومات (براجانزا وآخرون، 2017)، ويسرع التحول الرقمي للمؤسسات (تشو وآخرون، 2018)، ويعزز الميزة التنافسية للمؤسسات، ويحدث ترقية في صناعة التصنيع (يانغ وآخرون، 2020؛ تشو وآخرون، 2022b). بعبارة أخرى، تركز معظم الأدبيات الحالية حول التصنيع الذكي على التأثير الاقتصادي الناتج عن اعتماد نمط التصنيع الذكي وتولي اهتمامًا أقل للتأثير على أداء المسؤولية الاجتماعية للشركات. حتى لو

كانت ذات صلة، تركز الأبحاث فقط على التلوث البيئي (سونغ وآخرون 2023؛ شين وزانغ، 2023)، والتوظيف (أسيموغلو وريستريبو، 2018)، وإدارة سلسلة التوريد (غولدفارب وتاكر، 2019)، وأبعاد فردية أخرى. على سبيل المثال، فحص سونغ وآخرون (2023) تأثير الأتمتة والتكنولوجيا الذكية على البيئة ووجدوا أن المستوى المتزايد من تكنولوجيا الإنتاج مثل اعتماد الروبوتات يساهم في تقليل التلوث.

لمعالجة نقص الأدلة الدقيقة حول تأثير التصنيع الذكي على التحول المستدام للشركات، تفحص هذه الدراسة تجريبيًا تأثير برامج التصنيع الذكي التجريبية (IMPP) على أداء ESG للشركات من خلال بناء إطار تحليلي موحد. نركز على الإجابة على الأسئلة التالية: (1) هل يمكن أن تساعد IMPP المؤسسات في الوفاء بمسؤولياتها الاجتماعية وتحسين أداء ESG؟ (2) ما هي قنوات التأثير التي تؤثر من خلالها IMPP على أداء ESG؟ (3) هل يختلف التأثير اعتمادًا على خصائص الشركات؟

لذلك، تعالج هذه الدراسة IMPP كاختبار شبه طبيعي للتحقيق في العلاقة السببية بين التصنيع الذكي وأداء ESG للشركات. نقسم أولاً الشركات إلى مجموعات معالجة وضبط وفقًا لمشاركتها في IMPP، ثم نتبنى طريقة الفرق في الفرق المتقطع للاختبارات التجريبية. تظهر النتائج أن IMPP يمكن أن يحسن أداء ESG للشركات وأن الاستنتاج لا يزال ساريًا في سلسلة من اختبارات المتانة. يظهر تحليل الآلية أن الابتكار الأخضر وتخصيص الموارد المالية هما قناتان مهمتان للتأثير، وهما وساطة جزئية. بالإضافة إلى ذلك، نجد أيضًا أن تأثير تعزيز IMPP على أداء ESG يكون أكثر وضوحًا في المؤسسات غير المملوكة للدولة، والتكنولوجيا العالية، والمشاريع الثقيلة الملوثة.

المساهمات الهامشية لهذه الورقة هي كما يلي: أولاً، نحن ندمج التصنيع الذكي وأداء ESG للشركات في إطار تحليلي شامل. بالمقارنة مع الدراسات الحالية حول الاندماجات والاستحواذات (باروس وآخرون، 2022)، وثقافة الشركات (باي وآخرون، 2024)، وسياسات الضمان الاجتماعي (لو وآخرون، 2022)، والحوافز الضريبية (تانغ ووانغ، 2022)، والابتكارات التكنولوجية (مينتاه وإلمارزوقي، 2024؛ لو وآخرون، 2024) وعوامل داخلية وخارجية أخرى تؤثر على أداء ESG، تهدف هذه الدراسة إلى البدء من منظور التصنيع الذكي ومعاملة IMPP كتجربة شبه طبيعية لكشف التأثير السببي في تعزيز التنمية المستدامة للمؤسسات. توفر هذه الورقة منظورًا جديدًا لفهم العوامل متعددة الأبعاد التي تؤثر على أداء ESG.

ثانيًا، تهدف هذه الورقة إلى استكشاف الآثار الإيجابية لـ IMPP على أداء ESG للشركات من خلال دمج الاستنتاج النظري والتحليل التجريبي. معظم الأدبيات الحالية تدرس تجريبيًا تأثير التصنيع الذكي على الابتكار وأداء الإنتاج (لي وبرانستتر، 2024؛ فينتوريني، 2022)، تحلل هذه الورقة التأثير المحتمل للتصنيع الذكي على أداء ESG من منظور نظري ثم تستخدم بيانات الشركات المدرجة في الصين للتحليل التجريبي. النتائج لا تثري فقط النظام النظري للتصنيع الذكي، ولكنها أيضًا توفر دعمًا قيمًا لصانعي السياسات عند تنفيذ استراتيجية التصنيع الذكي.

ثالثًا، تكشف هذه الدراسة المزيد عن قنوات تأثير التصنيع الذكي على أداء ESG للمؤسسات. بالمقارنة مع الدراسات الحالية التي تناقش آلية التأثير من خلال التحول الرقمي والتحول التنظيمي (رانا ودالتاني، 2023؛ زيبَا وآخرون، 2021)، تبدأ هذه الدراسة من خصائص متطلبات IMPP وتستكشف دورها في أداء ESG للمؤسسات من خلال تعزيز الابتكار الأخضر للشركات وتحسين تخصيص الموارد المالية. تمتد نتائجنا إلى الآلية الدقيقة للتصنيع الذكي على التحول الأخضر للشركات.

الجزء التالي من هذه الورقة منظم كما يلي: “الخلفية المؤسسية والفرضية النظرية” هي الخلفية المؤسسية والفرضية النظرية؛ “البيانات والمنهجية” تظهر البيانات والمنهجية؛ “التحليل التجريبي” يجري التحليل التجريبي؛ “المناقشة الإضافية” تتضمن مناقشة إضافية، و”الاستنتاج وآثار السياسات” هو الاستنتاج وآثار السياسات.

الخلفية المؤسسية والفرضية النظرية

الخلفية المؤسسية. يعد التصنيع الذكي، كابتكار ثوري في التطور الصناعي الحديث، له تأثير عميق على ترقية الصناعة العالمية وأصبح محور المنافسة بين الدول. على سبيل المثال، قدمت الولايات المتحدة “استراتيجية القيادة في التصنيع المتقدم”، ودعت ألمانيا إلى “استراتيجية الصناعة الوطنية 2030″، وخطة “الصناعة الجديدة في فرنسا”، و”المجتمع 5.0” في اليابان. تماشيًا مع أهداف مماثلة، أطلقت الصين عدة مبادرات، مثل “صنع في الصين 2025″، و”خطة تطوير التصنيع الذكي (2016-2020)”. في الممارسة المحددة، نظرًا لأن التصنيع الذكي هو نظام هندسي معقد وضخم، بدأت الحكومة في إصدار “إشعار بدء العمل الخاص بتجربة التصنيع الذكي” لاختيار الشركات الرائدة في التصنيع الذكي منذ عام 2015.

سياسة IMPP هي محاولة مهمة لدمج التصنيع الذكي بعمق في التنمية الخضراء. للمرة الأولى، تتضمن تقليل تكاليف التشغيل ومعدلات عيوب المنتجات، وتقليل دورات تطوير المنتجات، وتحسين كفاءة الإنتاج، وتعزيز كفاءة استخدام الطاقة في متطلبات التقييم. في الواقع، بعد المشاركة في IMPP، تشكل الشركات مزايا تنافسية من حيث كفاءة الإنتاج، وتكاليف التشغيل، وكفاءة استخدام الطاقة (يانغ وآخرون، 2020؛ زانغ ولي، 2021؛ ين ولي، 2022). وهذا يعني أن التصنيع الذكي لا يحسن فقط كفاءة تخصيص الموارد، ولكنه أيضًا يجلب فرصًا جديدة لتعزيز التنمية المستدامة.

الفرضية النظرية. استنادًا إلى عزار وفيفس (2021) ولي وآخرون (2023)، تأخذ هذه الدراسة مدخلات ESG في نموذج اتخاذ القرار الإنتاجي للشركات. على وجه التحديد، نفترض أنه في سوق تنافسية غير كاملة بها J شركات، يمكن تعيين دالة الإنتاج للشركة الممثلة كـ حيث تمثل إجمالي إنتاج الشركات، A تمثل نمط الإنتاج المعتمد من قبل المؤسسة ( أو 2 )، تمثل الإنتاج التقليدي والتصنيع الذكي؛ تمثل استثمار المؤسسة في ESG، تمثل مدخلات رأس المال للمؤسسة، و تقيس تكنولوجيا الإنتاج. يتأثر إنتاج المؤسسة بشكل رئيسي بنمط الإنتاج، ومدخلات ESG، ومدخلات رأس المال، وليس متأثرًا بمدخلات العمل. أثبتت الأدبيات الحالية أن أداء ESG يساعد في تحسين الكفاءة التشغيلية، وكذلك كفاءة الاستثمار (أرول وآخرون، 2022). لذلك، يمكن الافتراض أن أي أنه إذا تم اختيار التصنيع الذكي أو زيادة مدخلات ESG، يمكن تحسين المستوى الفني للمؤسسات وفقًا لذلك، وسيكون مستوى الإنتاج أعلى.

نفترض أيضًا أن تكلفة كل وحدة من مدخلات رأس المال ، تكلفة كل وحدة من مدخلات ESG هي ، ويختار نمط الإنتاج لكل وحدة من تكلفة المدخلات. سعر المنتج هو ، وبشكل محدد كثابت. لذلك، يمكن التعبير عن دالة الربح للشركة كالتالي:

استنادًا إلى شرط تعظيم الربح، فإن المشتقات الجزئية من الدرجة الأولى لـ و هي كما يلي:

وفقًا للمعادلات (4) و(5)، يمكننا الحصول على:

من خلال التفاضل في المعادلة (6) بالنسبة لـ و ، يمكننا الحصول على:

استنادًا إلى الحسابات أعلاه، يمكننا الحصول على:

وفقًا للمعادلة (8)، عندما يكون صحيحًا. يعني أنه مع استخدام نمط الإنتاج الذكي، فإن التأثير الهامشي للتحول على تكنولوجيا الإنتاج يتناقص؛ مع زيادة مدخلات ESG، يتناقص تأثيرها الهامشي على مستوى تكنولوجيا الإنتاج أيضًا. يتماشى هذا الإعداد مع كل من شروط إينادا لدالة الإنتاج وواقع إنتاج الشركات. وهذا يعني أنه مع بقاء الشروط الأخرى دون تغيير، عندما تتبنى الشركات أنماط التصنيع الذكي المتقدمة، يمكنها استثمار المزيد في ESG. لذلك، نقترح:

الفرضية 1: يمكن أن يحسن التصنيع الذكي أداء ESG للشركات.

تسلط نظرية المنظور القائم على الموارد الضوء على أنه عندما تحول الشركات مواردها الحالية إلى قدرات فريدة، يمكنها إنشاء ميزة تنافسية. تمتلك الشركات المشاركة في IMPP، التي تستخدم تقنيات مثل الذكاء الاصطناعي لتجديد عمليات الإنتاج، بلا شك قوة تكنولوجية متفوقة مقارنة بالشركات غير الذكية. الشركات المعتمدة كأعضاء في تجربة التصنيع الذكي عمومًا لديها إنتاجية أعلى ( )، وفي نفس الوقت لديها المزيد من مدخلات الابتكار، مما سيدفع تطبيق التقنيات الجديدة (ين ولي، 2022).

على وجه التحديد، من جانب الإنتاج، تستفيد التصنيع الذكي من تقنية إنترنت الأشياء لمراقبة مراحل الإنتاج المختلفة في الوقت الحقيقي، مما يكسر حواجز المعلومات داخل عمليات الإنتاج. وهذا يحول الابتكار التجريبي إلى ابتكار معلوماتي، ويعزز الابتكار الدقيق في المراحل الحرجة. إن دمج واستخدام التقنيات الخضراء يعزز بشكل كبير كفاءة وفعالية تكلفة الإنتاج المؤسسي (فينغ وآخرون، 2024). ثانيًا، من جانب المستهلك، يصبح من الأسهل على الشركات جمع البيانات حول سلوك المستخدم وتفضيلات الطلب من خلال تطبيق تقنية البيانات الضخمة. من خلال بناء شبكة ابتكار بين المستهلكين والشركات، من المتوقع أن تقوم الشركات بتخصيص الإنتاج، وتعزيز إنتاجية تكرار المنتجات، وتحفيز الابتكار (لو وشو، 2019؛ بينغ وتاو، 2022). تقوم الشركات بتنمية تنافسية خضراء من خلال الابتكار التكنولوجي الأخضر، وتحسين كفاءة استخدام الموارد، مما يدفعها لتلبية الالتزامات البيئية بشكل أفضل وتحسين أداء ESG (هوانغ وآخرون، 2023). وبالتالي، نقترح:

الفرضية 2: يمكن أن يحسن التصنيع الذكي أداء ESG للشركات من خلال تأثيرات الابتكار الأخضر.

تعتبر كفاءة تخصيص الموارد عاملاً مهمًا يؤثر على تحقيق التنمية الخضراء والمستدامة للشركات. وفقًا لنظرية تخصيص الموارد، يمكن أن تتدفق عوامل الإنتاج إلى القطاعات أو الشركات ذات الكفاءة الإنتاجية الأعلى (ميلتس، 2003). وينطبق الشيء نفسه على الموارد المالية. يجادل هذا البحث بأن تقنية التصنيع الذكي ستعمل على تحسين أداء ESG من خلال تحسين كفاءة تخصيص موارد الشركات. تحت نظام التصنيع الذكي، يمكن للشركات تعديل خطط الإنتاج ديناميكيًا وفقًا للطلب الفوري، وتحسين هيكل التكلفة إلى حد ما، وتحقيق توازن أفضل بين تمويل الديون والأسهم، وتحسين كفاءة استخدام رأس المال في الشركات (ما وآخرون، 2020؛ يانغ وآخرون، 2020؛ وو وليو، 2024). وفقًا للسياسات ذات الصلة لدعم تطوير التصنيع الذكي في الصين والوضع الحالي للسوق المالية، ستحصل الشركات على دعم مالي مناسب بعد المشاركة في IMPP. وهذا يعني أن قيود التكلفة التي تواجهها الشركات الذكية قد انخفضت، مما يعزز المزيد من الاستثمار في ESG.

من منظور توفر رأس المال، يقلل مشاركة الشركات في IMPP من عدم التماثل في المعلومات ومخاطر الائتمان بين الشركات والبنوك والمستثمرين. ستتحسن الفرص المتاحة للشركات لطلب التمويل الخارجي، ويمكن أن تتدفق الأموال في اتجاهات أكثر كفاءة (أشامبونغ وإلشانديدي، 2021). علاوة على ذلك، من وجهة نظر كفاءة استخدام رأس المال، يقلل التصنيع الذكي من تخصص الأصول من خلال قرارات الإنتاج الذكية، مما يجعل الإنتاج المرن ممكنًا، مما يحسن كفاءة استخدام رأس المال (تشونغ وجاو، 2017؛ غولدفارب وتاكر، 2019). من خلال تقليل تكلفة استخدام رأس المال وتحسين تخصيص الموارد المالية، يمكن للشركات تحسين أداء ESG. وبالتالي، نقترح:

الفرضية 3: يمكن أن يحسن التصنيع الذكي أداء ESG للشركات من خلال تأثير تخصيص الموارد المالية.

البيانات والمنهجية

البيانات. بالإشارة إلى هاو وآخرون (2024) وزو وآخرون (2024)، نختار شركات A-share المدرجة في أسواق الأسهم في شنغهاي وشنتشن كعينات بحثية. السبب هو أن هناك عددًا

كبيرًا من الشركات المدرجة التي تشمل صناعات متنوعة، وتحتل دورًا مهمًا وتمثيليًا في اقتصاد الصين. بالإضافة إلى ذلك، لدى هذه الشركات متطلبات خاصة للإفصاح عن معلومات ESG، وبيانات ESG متاحة بشكل كبير. فترة اختيار العينة هي 2009-2021، ومتغيرات المالية للشركات مأخوذة من قاعدة بيانات CSMAR. يستخدم هذا البحث درجة ESG كمتغير بديل لأداء ESG للشركات، والتي يتم الحصول عليها من نظام تصنيف ESG لمؤشر الصين سينو-سكيورتيز. لتحسين دقة النتائج التجريبية، بالإشارة إلى تانغ وآخرون (2024)، نقوم بمعالجة العينات على النحو التالي: (1) إزالة الشركات من قطاعات المالية والتأمين، بالإضافة إلى الشركات المعالجة الخاصة (ST)؛ (2) استبعاد العينات التي تفتقر إلى بيانات المتغيرات الرئيسية؛ (3) تطبيق طريقة وينسور على المتغيرات المستمرة عند كل من 1 والعتبات. أخيرًا، نحصل على مجموعة بيانات شاملة تتكون من 23,590 ملاحظة سنوية للشركات.

يوفر الجدول 1 الوصف الإحصائي للمتغيرات الرئيسية. من الجدير بالذكر أن متوسط درجة ESG يبلغ 73.256، مع انحراف معياري قدره 4.766. تتراوح الدرجات من حد أدنى قدره 56 إلى حد أقصى قدره 84.19، مع وسيلة قدرها 73.49، مما يشير إلى تباين معتدل في أداء ESG بين الشركات، وعادة ما تتجمع في الطبقات الوسطى إلى العليا. IMPP هو المتغير التفسيري في هذا البحث، وتظهر النتائج أن القيمة المتوسطة هي 0.003 والانحراف المعياري هو 0.056. ومع ذلك، تكشف الإحصائيات ذات الوسيط 0 عن ظاهرة ملحوظة: عدد العينات في مجموعة المعالجة التي تنفذ IMPP أقل من تلك في مجموعة التحكم، وهو السبب في اختيار طريقة توازن الإنتروبيا في اختبار القوة لحل قابلية المقارنة بين العينات. يتم أيضًا وصف متغيرات التحكم الإضافية، بما يتماشى مع النتائج المبلغ عنها في الأدبيات الحالية (لي وآخرون، 2024).

المتغيرات

المتغير التابع. بالإشارة إلى تشانغ وآخرون (2024)، يتم قياس أداء ESG للشركات من خلال البيانات من نظام تصنيف ESG لمؤشر الصين سينو-سكيورتيز. تم بناء منهجية التصنيف من خلال المنهجية الدولية السائدة والخبرة العملية فيما يتعلق بخصائص سوق رأس المال المحلي. يتضمن نظام التصنيف درجات ESG وتصنيفات AAAC، والتي تهدف إلى تقييم امتثال الشركة للمعايير البيئية والاجتماعية والحكومية الحالية. كلما كانت الدرجة أعلى، كان أداء ESG أفضل.

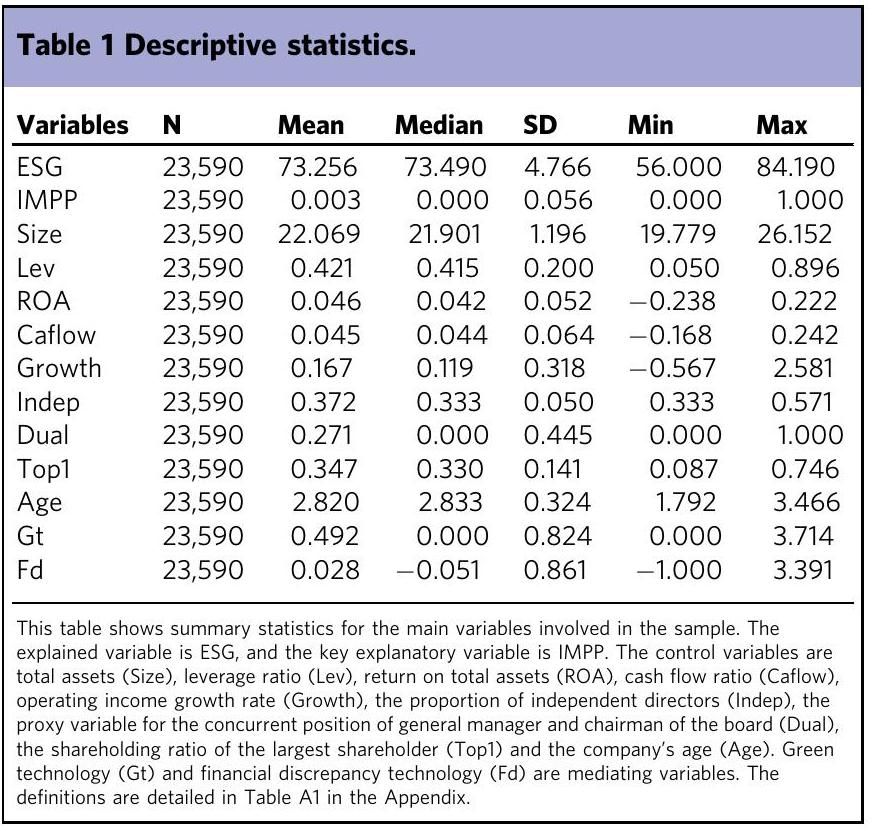

الشكل 1 اختبار التأثير الديناميكي. يُستخدم هذا الشكل لاختبار ما إذا كانت مجموعات المعالجة والتحكم تلبي فرضية الاتجاه المتوازي. يمثل المحور الأفقي نقاط زمنية عينة بالنسبة لسنة تنفيذ السياسة، ويمثل المحور العمودي التأثيرات الاقتصادية الديناميكية للسياسة. تشير الماس الماسية إلى المعاملات وتمثل الخطوط الصلبة فترات الثقة 95%. وفقًا لجاكوبسون وآخرون (1993)، يتم أخذ السنة التي تسبق صدمة السياسة كفترة أساسية. جميع المعاملات للسنوات التي تسبق تنفيذ السياسة ليست مختلفة بشكل كبير عن الصفر، مما يلبي فرضية الاتجاه المتوازي.

المتغير المستقل. المتغير التفسيري في هذا البحث هو، والذي يُستخدم لتقييم ما إذا كانت الشركةتشارك في مشروع الطيار للتصنيع الذكي في السنة. بالإشارة إلى وي وآخرون (2024)، إذا تم الموافقة على الشركةكشركة نموذجية للتصنيع الذكي في السنة، فإن IMPPيأخذ القيمة 1 في السنة الحالية والسنوات اللاحقة؛ وإلا، فإنه يكون 0.

متغيرات الآلية. التكنولوجيا الخضراء (Gt). يهدف هذا البحث إلى تقييم الابتكار الأخضر للشركات، ونتبنى طريقة القياس لطلبات براءات الاختراع الخضراء، والتي تتماشى مع وانغ وآخرون (2024). نعتقد أن عدد طلبات براءات الاختراع التي تقدمها الشركات يمكن أن تعكس بشكل أكثر دقة الإنجازات التكنولوجية الرئيسية التي تمتلكها، وبالتالي تعكس بشكل أكثر مباشرة قدرتها على الابتكار الأخضر. لذلك، كلما زاد عدد طلبات براءات الاختراع التي تقدمها الشركة، كلما اعتُبرت قدرتها على الابتكار الأخضر أقوى.

الاختلاف المالي (Fd). وفقًا لـ Qi وآخرين (2023)، يتم تعريف مفهوم الاختلاف المالي على أنه انحراف تكلفة رأس المال لشركة ما عن متوسط الصناعة. تقيس هذه المعادلة التوافق المالي لشركة ما بالنسبة لمعايير تكلفة رأس المال على مستوى الصناعة. لتقييم تكلفة رأس المال للشركات، نستخدم نسبة مصروفات الفائدة إلى إجمالي الالتزامات، مع تعديل إجمالي الالتزامات باستثناء الحسابات المستحقة الدفع. كلما زادت القيمة، زادت درجة عدم التوافق المالي في الصناعة.

متغيرات التحكم. للحصول على التأثير الصافي لـ IMPP على أداء الشركات في مجال ESG، نختار تسعة متغيرات تحكم على مستوى الشركة قد تؤثر على أداء ESG وفقًا لـ He et al. (2023) و Wang et al. (2023). أولاً، يمكن أن يؤدي الأداء المالي الأفضل إلى تقليل قيود التمويل على الشركات، مما يشجع الشركات على تحمل مسؤولية اجتماعية أكبر. بالإشارة إلى Ye و Tian (2024)، اختارت هذه الورقة نسبة الرفع المالي (Lev) ونسبة العائد على الأصول الإجمالية (ROA) ونسبة التدفق النقدي (Caflow) ومعدل نمو الدخل التشغيلي (Growth) كمتغيرات تحكم. ثانيًا، أشار Hillman و Dalziel (2003) إلى أن هيكل الحوكمة المؤسسية يؤثر على المسؤولية الاجتماعية للشركات.

لذلك، فيما يتعلق بـ هوانغ وآخرون (2024) وموسى وآخرون (2024)، نختار نسبة ملكية أكبر مساهم (Top1)، ونسبة المديرين المستقلين (Indep)، وما إذا كان المدير العام ورئيس مجلس الإدارة يشغلهما نفس الشخص (Dual) كمتغيرات تحكم. أخيرًا، يتحكم هذا البحث أيضًا في تأثير إجمالي الأصول (Size) وعمر الشركة (Age) على أداء ESG. وذلك لأن الشركات الأكبر تميل إلى تحمل مسؤوليات اجتماعية أكبر، مما سيؤثر على أدائها في ESG (دريمبيتيك وآخرون، 2020). يتم تقديم الوصف المحدد للمتغيرات في الجدول الملحق A1.

تصميم النموذج

نموذج الانحدار المرجعي. لتقليل تأثير العوامل الخارجية والانحياز في الاختيار على تقييم آثار السياسات، تختار هذه الورقة نموذج الفرق في الفرق (DID) للتحليل. بشكل محدد، واتباعًا لجيا (2014)، تستخدم هذه الدراسة نموذج انحدار DID متداخل يهدف إلى التحقق من الفرضية 1. السبب هو أن الشركات في مجموعة المعالجة تم اعتمادها كشركات نموذجية في التصنيع الذكي على دفعات. النموذج المحدد الذي يقيم تأثير IMPP على أداء ESG هو كما يلي:

يمثل أداء ESG للمؤسسةفي السنة, هو متغير وهمي للسياسة يشير إلى ما إذا كانت المؤسسةفي السنةيشارك في IMPP،هي متغيرات تحكمية على مستوى الشركة، و تمثل التأثيرات الفردية والثابتة للسنة على التوالي، و هو مصطلح الاضطراب العشوائي. نركز على المعامل من. إيجابييشير إلى أن تنفيذ IMPP يحسن أداء الشركات في مجال ESG، بينما يشير السلب إلىيشير إلى عائق في أداء ESG.

اختبار الاتجاه المتوازي. تعتمد صلاحية طريقة الاختلاف في الاختلافات (DID) على الفرضية القائلة بأن الاتجاهات الأساسية في مجموعتي العلاج والضبط يجب أن تكون متشابهة قبل تنفيذ التدخل، ويجب أن تكون الاتجاهات مختلفة بشكل ملحوظ بعد الصدمة. للتحقق مما إذا كانت هذه الفرضية مستوفاة، نقوم ببناء النموذج التالي:

في هذا التحليل، المتغير ، يمثل مجموعة من المتغيرات الوهمية، بينمايشير إلى المعامل، الذي يعد حاسمًا لتحديد أي تفاوتات كبيرة بين مجموعة التحكم ومجموعة العلاج. بما يتماشى مع جاكوبسون وآخرون (1993)، تحدد التحليل السنة التي تسبق صدمة السياسة كفترة الأساس. لتجنب التحيز في التقدير الناتج عن كون فترة دراسة الحدث طويلة جدًا مما يؤدي إلى نقص البيانات في كلا الطرفين، تعتمد هذه الورقة نهج ليو وآخرون (2023) وكونغ وآخرون (2024) من خلال تحديد فترة النافذة إلى 4 فترات زمنية قبل وبعد تنفيذ السياسة. عندما، الوضع خاص.يعني أن الفرق بين سنة العينة والسنة التي تم فيها تأسيس المؤسسةيتم الموافقة على أنها مؤسسة تجريبية في التصنيع الذكي إذا كانت أكبر من أو تساوي 4، فإنها تنتمي إلى مجموعة العلاج. عندما، يعني أن الفرق بين سنة العينة والسنة التي شاركت فيها المؤسسة في IMPP أقل من أو يساوي -4، المؤسسةتنتمي إلى مجموعة العلاج؛ وإلا، فهي 0.

اختبار الآلية. استنادًا إلى الافتراضات النظرية، قد تؤثر التصنيع الذكي على أداء الشركات في مجالات البيئة والمجتمع والحوكمة من خلال الابتكار في التكنولوجيا الخضراء وإعادة تخصيص الموارد المالية. بالإشارة إلى بارون وكيني (1986)، الوسيط

الجدول 2 نتيجة الانحدار الأساسية.

المتغيرات

(1)

(2)

(3)

(4)

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

IMPP

2.694***

2.391***

2.769***

2.611***

حجم

0.888***

1.014***

1.033***

ليف

-3.709*** (0.305)

-3.498*** (0.384)

-3.795*** (0.392)

العائد على الأصول

9.939*** (0.801)

6.452*** (0.871)

6.567*** (0.873)

كافلو

-2.417*** (0.481)

-1.992*** (0.499)

-2.327*** (0.507)

نمو

-0.383*** (0.084)

-0.492*** (0.085)

-0.342*** (0.087)

مستقل

6.309*** (0.807)

6.096*** (0.984)

6.056*** (0.969)

ثنائي

0.022 (0.095)

0.018 (0.117)

0.018 (0.116)

الأول

1.486*** (0.407)

1.914*** (0.718)

1.604** (0.717)

عمر

-1.078*** (0.181)

-2.133*** (0.300)

-3.232*** (0.755)

ثابت

73.637*** (0.104)

55.690*** (1.210)

55.292*** (1.800)

58.087*** (2.789)

شركة FE

✓

×

✓

✓

سنة FE

✓

✓

×

✓

ر

0.016

0.027

0.032

0.049

ن

23590

23590

23590

23590

تقدم هذه الجدول النتائج الأساسية المقدرة بناءً على النموذج المعادلة (9)، حيث يتم تحليل تأثير IMPP على أداء الشركات في مجال ESG. المتغير التابع هو درجات ESG، وIMPP هو متغير وهمي. تمثل المتغيرات الضابطة بشكل متسلسل إجمالي الأصول (الحجم)، ونسبة الرفع المالي (Lev)، والعائد على إجمالي الأصول (ROA)، ونسبة التدفق النقدي (Caflow)، ومعدل نمو الدخل التشغيلي (Growth)، ونسبة المديرين المستقلين (Indep)، والمتغير البديل للمنصب المتزامن للمدير العام ورئيس مجلس الإدارة (Dual)، ونسبة ملكية أكبر مساهم (Top1) وعمر الشركة (Age). تقدم العمود (1) النتائج التي تتحكم فقط في تأثيرات السنة والشركة الثابتة. تشمل الأعمدة (2) و(3) المتغيرات الضابطة ولكن تتحكم في تأثيرات السنة الثابتة وتأثيرات الشركة الثابتة بشكل منفصل. يقدم العمود (4) نتائج الانحدار التي تشمل المتغيرات الضابطة وتتحكم في تأثيرات الشركة والسنة في الوقت نفسه. ** و *** تشير إلى مستويات الدلالة. و ، على التوالي، مع الأخطاء المعيارية المجمعة بين قوسين. تم بناء نموذج التأثير للتحقق من الفرضيات H 2 و H 3 :

أينهي المتغيرات الوسيطة، التي تمثل التكنولوجيا الخضراء والفجوة المالية.يعكس تأثير التصنيع الذكي على المتغير الوسيط، بينمايمثل تأثير المتغيرات الوسيطة على أداء ESG. والمتغيرات الأخرى هي نفسها كما في النموذج (9).

تحليل تجريبي

اختبار الاتجاه المتوازي. قبل إجراء الانحدار الأساسي، من الضروري تحديد ما إذا كان افتراض الاتجاه المتوازي مستوفى، مما يعني تقييم الفروق النظامية في أداء ESG بين مجموعات التحكم والمعالجة قبل تنفيذ IMPP. يتم تقدير نموذج الانحدار (10) وتعرض النتائج في الشكل 1. يمكن ملاحظة أن المعاملات قبل تنفيذ السياسة ليست مختلفة بشكل كبير عن الصفر، وتتقاطع فترات الثقة مع محور الصفر. وهذا يكشف عن عدم وجود تفاوت ملحوظ في أداء الشركات في مجال ESG بين مجموعتي التحكم والمعالجة قبل المشاركة. بعد تنفيذ السياسة، يكون معامل التأثير السنوي لـ IMPP إيجابيًا، وفترات الثقة لا تتجاوز محور الصفر، الذي يقع فوق محور الصفر. هذا يدل على أن المعامل يختلف بشكل كبير عن

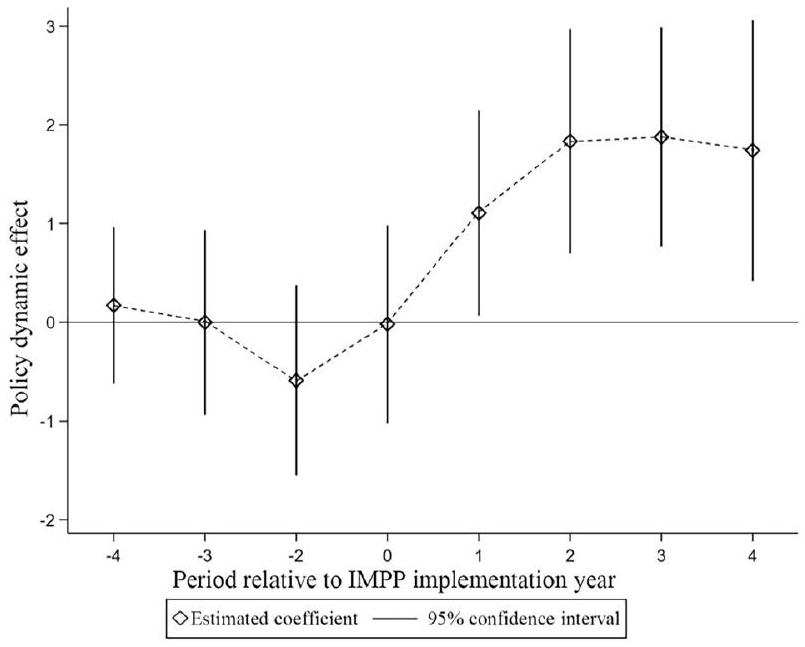

الشكل 2 اختبار الدواء الوهمي. يقدم الشكل نتائج اختبار الدواء الوهمي. على وجه التحديد، يتم استبدال متغير وهمي للسياسة المزيفة IMPP في المعادلة (9)، وتُكرر عملية الانحدار 500 مرة. ثم، يتم عرض توزيع معاملات IMPP لـ 500 انحدار كخط صلب. يمثل المحور الأفقي المُقدّر، ويمثل المحور العمودي الكثافة وقيم p، وتمثل النقاط السوداء قيم p للمُقدّر، ويمثل الخط المتقطع المعامل في الانحدار الأساسي. يمكن ملاحظة أن معاملات مجموعات العلاج الوهمي تتجمع حول الصفر، مما ينحرف بشكل كبير عن قيمة معامل الانحدار الأساسي البالغة 2.611، مما يثبت صحة النتائج المرجعية.

0 بعد صدمات السياسة وتحسن أداء ESG في مجموعة المعالجة أفضل بشكل ملحوظ من تلك في مجموعة التحكم. في الوقت نفسه، يظهر المعامل اتجاهًا تصاعديًا تدريجيًا في السنوات الثلاث الأولى بعد الانضمام إلى برنامج IMPP، بينما ينخفض قليلاً في السنة الرابعة. وهذا يعني أن التحسن في ESG الذي جلبته مشاركة الشركات في التصنيع الذكي يظهر اتجاهًا للارتفاع أولاً ثم الانخفاض.

الانحدار الأساسي. يتم اشتقاق نتيجتنا الأساسية من تقدير نموذج الانحدار (9)، كما هو موضح في الجدول 2. في العمود (1)، بعد أخذ تأثيرات السنة وثبات الشركة في الاعتبار ولكن دون ضوابط إضافية، نجد معامل IMPP إيجابي إحصائيًا عند الـمستوى الدلالة. تدعم هذه الأدلة الفرضية 1 التي تفيد بأن التصنيع الذكي يعزز بشكل ملحوظ أداء ESG. تعرض الأعمدة (2) و(3) نتائج إضافة متغيرات التحكم والتلاعب بتأثيرات السنة وتأثيرات الشركة، على التوالي. يقدم العمود (4) نتائج الانحدار التي تم فيها إضافة متغيرات التحكم وتم التحكم في تأثيرات الشركة والسنة في الوقت نفسه. توضح التحليلات أن معامل IMPP الإيجابي الكبير يبقى ثابتًا. حجم المعامل ليس مختلفًا بشكل كبير عن الأعمدة الثلاثة الأولى، مما يشير إلى أن المشاركة في IMPP قد حسنت أداء ESG للشركات. تشير النتائج من جميع الأعمدة الأربعة إلى أن المشاركة في التصنيع الذكي تعزز بشكل إيجابي أداء ESG للشركات، وهو ما يتماشى مع نتائج جون وآخرون (2024) ووي وآخرون (2024). تم التحقق من الفرضية 1.

قد يكون سبب هذه النتائج هو أن الشركات التي تعتمد على التصنيع الذكي تعتمد على البيانات الضخمة، وإنترنت الأشياء، وغيرها من التقنيات لمراقبة عملية الإنتاج، مما يزيد من الشفافية التشغيلية ويجعل قرارات الإنتاج أكثر فعالية. يمكن أن تلبي هذه الممارسات بشكل أكثر فعالية توقعات المستثمرين والهيئات التنظيمية وغيرهم من أصحاب المصلحة بشأن التنمية المستدامة، مما يعزز أداء ESG (Zhang et al., 2023). فيما يتعلق بالمتغيرات الضابطة، تميل الشركات الأكبر إلى الحصول على درجات ESG أعلى. قد يكون هذا

الجدول 3 اختبار توازن الانتروبيا باستخدام طريقة الاختلافات في الاختلافات.

المتغيرات

(1)

(2)

(3)

(4)

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

IMPP

2.072***

2.222***

1.985***

2.203***

ثابت

74.513***

43.825***

33.196***

٣٧.١٠٦***

التحكمات

×

✓

✓

✓

شركة FE

✓

×

✓

✓

سنة FE

✓

✓

×

✓

ر

0.072

0.062

0.073

0.078

ن

22237

22237

٢٢٢٣٧

22237

تقدم هذه الجدول نتائج تقدير المعادلة (9) بعد معالجة العينات بواسطة طريقة توازن الإنتروبيا، مع تحليل تأثير التصنيع الذكي على أداء الشركات في مجال ESG. العمود (1) يعرض النتائج مع التحكم فقط في تأثيرات السنة وتأثيرات الشركة الثابتة. العمودان (2) و(3) يتضمنان متغيرات التحكم ولكن يتحكمان في تأثيرات السنة الثابتة وتأثيرات الشركة الثابتة بشكل منفصل. العمود (4) يقدم نتائج الانحدار التي تشمل متغيرات التحكم وتتحكم في تأثيرات السنة والشركة في الوقت نفسه. المتغير التابع هو درجات ESG، وIMPP هو متغير وهمي. متغيرات التحكم هي نفسها كما هو مذكور أعلاه، والنتائج متاحة في الجدول A3 في الملحق. *** تشير إلى مستويات الدلالة بنسبة 1%، مع الأخطاء المعيارية المجمعة بين قوسين.

لأن الشركات الكبرى تولي اهتمامًا أكبر للأصول غير الملموسة مثل السمعة وتكون مدفوعة للوفاء بالمسؤوليات الاجتماعية. يرتبط ارتفاع نسبة الرفع المالي بأداء ESG أقل، ويؤدي ارتفاع العائد على الأصول إلى أداء ESG أعلى، وهو ما يتماشى مع الأدبيات الحالية (لو وتشينغ، 2023؛ ين وآخرون، 2023).

اختبارات القوة. لتحسين قوة نتائج الانحدار الأساسية، نستخدم أيضًا اختبار الدواء الوهمي، وطريقة توازن الانتروبيا، وبعض اختبارات القوة الأخرى. تهدف تطبيق هذه الطرق إلى التغلب على تحيز اختيار العينة ومشكلات الاندماج الناتجة عن المتغيرات المفقودة وضمان استنتاجات علمية وصحيحة.

اختبار الدواء الوهمي. للتخفيف من التأثير المحتمل للعوامل غير المرصودة في تحليل الانحدار المرجعي، تنفذ هذه الدراسة اختبار الدواء الوهمي. على وجه التحديد، يتم بناء المتغير الوهمي IMPP من خلال تحديد الشركات في مجموعة العلاج الزائفة ووقت التنفيذ، ثم يتم استبدال المتغير الوهمي IMPP المعاد بناؤه في المعادلة (9) للانحدار. يتم تنفيذ الإجراء الموضح أعلاه 500 مرة، مما يؤدي إلى توليد رسم بياني للتوزيع. نظرًا لأن المجموعة التجريبية الزائفة وفترة المشاركة يتم اختيارها عشوائيًا، يجب ألا يؤثر الصدمة السياسية الزائفة بشكل كبير على ESG الشركات. كما هو موضح في الشكل 2، يمثل المحور الأفقي المعامل، بينما يمثل المحور العمودي الكثافة وقيم p. تمثل النقاط السوداء قيم p للمقدر، بينما تشير الخطوط الصلبة إلى توزيع كثافة النواة، والخطوط المتقطعة تتوافق مع المعامل في الانحدار الأساسي. يمكن ملاحظة أن معاملات مجموعات العلاج الزائفة تتجمع بشكل أساسي حول الصفر، مما ينحرف بشكل كبير عن قيمة معامل الانحدار الأساسي البالغة 2.611. وهذا يشير إلى أن التدخلات السياسية المضللة لا تمارس تأثيرًا كبيرًا على ESG الشركات، أي أن النتائج من تحليل الانحدار الأولي لا تتأثر بالمتغيرات العشوائية الخفية وكذلك المتغيرات غير المرصودة الأخرى. إن تحسين أداء ESG الشركات هو بالفعل نتيجة للمشاركة في IMPP.

اختبار توازن الانتروبيا-DID. تختلف المؤسسات في جوانب عديدة، ليس فقط في ما إذا كانت تشارك في IMPP، ولكن أيضًا في الخصائص الفردية مثل العائد على إجمالي الأصول، والحجم، ونسبة الرفع المالي، مما قد يؤدي إلى انحياز محتمل في اختيار العينة.

الجدول 4 اختبار PSM-DID.

(1)

(2)

(3)

(4)

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

البيئة والمجتمع والحوكمة

IMPP

3.023***

3.481***

3.203***

2.874***

(0.722)

(0.859)

(0.601)

(0.582)

ثابت

73.284*** (0.003)

45.118*** (2.612)

48.548*** (3.072)

47.969*** (5.752)

التحكمات

×

✓

✓

✓

شركة FE

✓

×

✓

سنة FE

✓

×

✓

✓

ر

0.055

0.025

0.056

0.068

ن

18522

18522

18522

18522

تظهر هذه الجدول النتائج التي تم الحصول عليها باستخدام طريقة PSM لمطابقة العينات، ثم استخدام الانحدار DID. في العمود (1)، يتم تقديم النتائج بعد التحكم فقط في تأثيرات السنة والثابت. كلا العمودين (2) و(3) يتضمنان متغيرات التحكم، حيث يتحكم العمود (2) في تأثير السنة الثابت، بينما يتحكم العمود (3) في تأثير الشركة الثابت. يظهر العمود (4) نتائج الانحدار بعد التحكم في كل من متغيرات التحكم وتأثيرات السنة والشركة. المتغير التابع هو درجات ESG، وIMPP هو متغير وهمي. متغيرات التحكم هي نفسها المذكورة أعلاه، والنتائج متاحة في الجدول A4 في الملحق. *** تشير إلى مستويات الدلالة بنسبة 1%، مع الأخطاء المعيارية المجمعة بين قوسين.

في نتائج الانحدار المرجعي. لذلك، نستخدم طريقة توازن الإنتروبيا التي اقترحها هاينمولر (2012) للعثور على مجموعات التحكم الأكثر ملاءمة لمجموعة المعالجة من خلال التحكم في التوازن متعدد الأبعاد للمتغيرات. كل هذا لضمان تجانس تنفيذ السياسة (بيست وسينها، 2021). بشكل محدد، تختار هذه الورقة اللحظات من الدرجة الأولى للمتغيرات للمطابقة، وتظهر نتائج المطابقة في الجدول A2 في الملحق.

تقدم الجدول 3 نتائج اختبار توازن الانتروبيا-DID. في العمود (1)، لا تتضمن الانحدار أي متغيرات تحكم ولكن تتحكم في كل من تأثيرات السنة وتأثيرات الشركة الثابتة. تعكس الأعمدة (2) و(3) إضافة متغيرات تحكم والتلاعب بتأثيرات السنة الثابتة وتأثيرات الشركة الثابتة، على التوالي. تشمل نتيجة العمود (4) متغيرات تحكم وتتحكم في نفس الوقت في تأثيرات السنة وتأثيرات الشركة الثابتة. تظهر النتائج أن معامل IMPP إيجابي وذو دلالة إحصائية عند المستوى الإحصائي. وهذا يشير إلى أنه بعد النظر في التحيز في اختيار العينة، لا يزال للمشاركة في التصنيع الذكي تأثير إيجابي كبير على ESG الشركات، مما يؤكد قوة نتائجنا الأساسية.

اختبار PSM-DID. للتحكم في الفروق النظامية بين المجموعة التجريبية ومجموعة التحكم وتقليل التحيز في تقدير DID، تستخدم هذه الدراسة طريقة مطابقة الدرجات الاحتمالية (PSM) لفرز العينات. في العملية المحددة، يتم استخدام طريقة المطابقة لأقرب 4 جيران، ويتم اختيار المتغيرات التحكم التالية للمطابقة، مثل حجم المؤسسة (Size)، ونسبة الأصول إلى الخصوم (Lev)، والعائد على إجمالي الأصول (ROA)، وتدفق النقد (Caflow)، ومعدل النمو (Growth)، ونسبة المديرين المستقلين (Indep). تظهر نتائج المطابقة في الانحراف المعياري للمتغيرات المشتركة في الشكل A1 في الملحق.

بعد المطابقة، يتم استبدال العينات في نموذج الانحدار (9)، وتظهر النتائج في الجدول 4، عندما لا تتم إضافة متغيرات تحكم إلى العمود (1)، وعندما يتم التحكم في تأثيرات ثابتة فردية وتأثيرات ثابتة زمنية بشكل منفصل في الأعمدة (2)-(4)، أو كليهما. يمكن أن نجد أن معاملات IMPP في جميع نتائج الانحدار تتوافق مع نتائج الانحدار الأساسية في الجدول 2، أي أن معامل IMPP إيجابي وذو دلالة إحصائية عند المستوى . في نفس الوقت، يكون المعامل أكبر من نتيجة المعيار في الجدول 2، مما يشير إلى أنه بعد التحكم في تحيز العينة، يمكن أن يعزز انخراط الشركات في برنامج IMPP بشكل فعال أداء ESG للشركات، مما يثبت مرة أخرى قوة الانحدار المرجعي.

اختبار الجدول 5 للداخلية.

(1)

(2)

المرحلة الأولى

المرحلة الثانية

IMPP

ESG

IV

0.0045*** (0.001)

IMPP

40.7546*** (13.208)

ثابت

-0.0646*** (0.007)

58.3171*** (1.088)

التحكم

✓

✓

تأثيرات الشركة الثابتة

✓

✓

تأثيرات السنة الثابتة

✓

✓

إحصائية LM

36.912 [0.000]

إحصائية فالد F

36.921 {16.38}

N

22,641

22,641

يقدم هذا الجدول نتائج الانحدار لاختبارات الداخلية باستخدام طريقة المربعات الصغرى ذات المرحلتين. نستخدم المتغيرات الآلية (IV) لـ IMPP، والتي تم بناؤها بواسطة العنصر التفاعلي المضاعف بين عدد الموظفين في خدمات الاتصالات في عام 2003 وعدد مستخدمي الإنترنت في السنة السابقة في المنطقة التي تقع فيها المؤسسة. المتغيرات التحكم هي نفسها كما هو مذكور أعلاه، والنتائج متاحة في الجدول A5 في الملحق. قيمة [] هي قيمة P، وقيمة هي القيمة الحرجة عند المستوى لاختبار التعرف الضعيف. *** تشير إلى مستويات الدلالة 1%، على التوالي، مع أخطاء معيارية متجمعة في الأقواس.

اختبار الداخلية. على الرغم من أن هذه الدراسة تسعى للتحكم في العوامل المختلفة التي قد تؤثر على أداء ESG للمؤسسات، قد لا تزال النتائج التجريبية تتأثر ببعض العوامل المحتملة التي لم يتم ملاحظتها، مما يتسبب في تحيز التقدير. لمعالجة قضايا الداخلية التي قد تنشأ من المتغيرات المفقودة والسببية العكسية، نقترح استخدام طريقة المتغير الآلي (IV) لتعزيز موثوقية النتائج. بالإشارة إلى كوان ولي (2022)، يتم اختيار العنصر التفاعلي المضاعف بين عدد الموظفين في خدمات الاتصالات في عام 2003 وعدد مستخدمي الإنترنت في السنة السابقة في المنطقة التي تقع فيها المؤسسة، كمتغير آلي لـ IMPP. علاوة على ذلك، فإن إحصائية فالد-F في اختبار تحديد IV الضعيف أعلى من القيمة الحرجة عند المستوى ، مما يؤكد أن اختيار IV معقول.

لذلك، يتم استخدام طريقة المربعات الصغرى ذات المرحلتين للانحدار. تظهر نتائج الانحدار في الجدول 5. في المرحلة الأولى، يكون معامل الانحدار لـ IV إيجابيًا بشكل كبير عند المستوى ، مما يشير إلى وجود ارتباط إيجابي كبير بين IMPP و IV. في المرحلة الثانية، لا يزال معامل الانحدار لـ IMPP إيجابيًا بشكل كبير عند المستوى . بعبارة أخرى، في حالة التخفيف المحتمل للداخلية، يمكن أن تستمر الشركات المشاركة في تجربة IMPP في تعزيز أداء ESG بشكل إيجابي، مما يثبت مرة أخرى قوة النتائج الأساسية.

اختبارات التباين

تباين ملكية الشركات. قد تؤدي اختلافات الملكية إلى أداء مختلف في المسؤولية الاجتماعية، خاصةً الشركات المملوكة للدولة والشركات الخاصة في طريقة الوفاء بالمسؤولية الاجتماعية (تشانغ وآخرون، 2023؛ لي وآخرون، 2023). عادةً ما تكون الشركات المملوكة للدولة أكبر ولديها مصداقية اجتماعية أعلى، بينما تكون الشركات الخاصة أكثر مرونة ولديها دافع أقوى للتكيف مع التطور التكنولوجي. في هذه الدراسة، يتم تصنيف العينات حسب هيكل ملكيتها إلى مجموعات مملوكة للدولة وغير مملوكة للدولة. تظهر الأعمدة (1) و(2) في الجدول 6 أنه بالنسبة للشركات المملوكة للدولة، فإن معامل IMPP إيجابي ولكنه يفتقر إلى الدلالة الإحصائية. على العكس من ذلك، بين الشركات غير المملوكة للدولة، فإن معامل IMPP إيجابي وذو دلالة إحصائية عند المستوى . علاوة على ذلك، فإن معامل الانحدار

لشركات غير المملوكة للدولة يتجاوز ذلك للشركات المملوكة للدولة. تشير هذه النتائج إلى أن IMPP يلعب دورًا أكبر وأكثر أهمية في تحسين أداء ESG للشركات غير المملوكة للدولة. يمكن أن يُعزى ذلك إلى أن الشركات غير المملوكة للدولة، التي تواجه ضغطًا أكبر في المنافسة السوقية، تميل إلى تعديل استراتيجيات إنتاجها بسرعة استجابة لمتطلبات السوق وتفضيلات المستهلكين.

تباين مستوى التكنولوجيا الصناعية. يمثل التصنيع الذكي تكامل تكنولوجيا المعلومات المتطورة مع عمليات التصنيع المعقدة. عادةً ما تحتوي الصناعات عالية التقنية على مكونات تقنية أعلى وتكون أكثر عرضة للتغيير التكنولوجي. من خلال التكيف بشكل أسرع مع التغييرات التي تطرأ نتيجة للتصنيع الذكي، تعدل بسرعة طرق إنتاجها وتفي بشكل أفضل بمسؤولياتها الاجتماعية. وفقًا لجاو وآخرون (2024د) ووانغ وآخرون (2024)، نحدد رمز الصناعة للشركات المدرجة عالية التقنية وفقًا لتعريف دليل تصنيف الصناعة للشركات المدرجة (2012). من بينها، يتم التعرف على الشركات ذات رموز الصناعة C25-C29، C31-C32، C34-C41، I63-I65، وM73 كشركات صناعية عالية التقنية، بينما البقية هي شركات غير تقنية. يمكن العثور على التصنيف الصناعي المحدد في الجدول A9 في الملحق.

تظهر التحليل المقدم في الأعمدة (3) و(4) من الجدول 6 أن معامل IMPP يحمل معاملًا إيجابيًا وذو دلالة إحصائية على الأقل عند المستوى . من الجدير بالذكر أن حجم المعامل أكثر وضوحًا داخل القطاعات عالية التقنية. وهذا يشير إلى أن المشاركة في IMPP تحسن أداء ESG للشركات، مع تأثير أكبر على الشركات في الصناعات عالية التقنية. تؤكد النتيجة أيضًا فرضيتنا بأن اعتماد التصنيع الذكي يمكن أن يحسن عمليات الإنتاج وبالتالي يعزز أداء ESG عبر صناعات مختلفة، لا سيما بالنسبة للصناعات عالية التقنية. بالاعتماد على المستوى التقني الأعلى الموجود، تكون تلك الشركات أكثر تكيفًا مع تطوير وتطبيق تكنولوجيا التصنيع الذكي، وبالتالي تحقيق تحسينات في ESG.

تباين مستوى التلوث. قد يكون هناك أيضًا ارتباط بين مستوى انبعاث الملوثات وأداء المسؤولية الاجتماعية. خاصة بالنسبة للصناعات ذات التلوث الثقيل، فإن الدافع لتنفيذ التنمية المستدامة يكون أقوى، لتجنب الشكاوى من أصحاب المصلحة مثل المستثمرين والجهات التنظيمية الحكومية. إن تنفيذ التحول الذكي لتحسين تخصيص الموارد وتعزيز الابتكار الأخضر يكون أكثر ملاءمة للوفاء بالمسؤوليات الاجتماعية وتحسين أداء ESG. بالإشارة إلى يو وسو (2024) ووانغ وآخرون (2024)، نستخدم التعريف الوارد في النسخة المعدلة من إرشادات تصنيف الصناعة للشركات المدرجة التي أصدرتها لجنة تنظيم الأوراق المالية الصينية في عام 2012 لتصنيف الصناعات إلى صناعات ذات تلوث ثقيل وصناعات غير ذات تلوث ثقيل. من بينها، تشمل الصناعات ذات التلوث الثقيل 15 صناعة مختلفة، بما في ذلك تعدين الفحم، وتعدين النفط والغاز الطبيعي، وتعدين ومعالجة خام المعادن الحديدية.

تظهر الأعمدة (5) و(6) في الجدول 6 أن معامل IMPP إيجابي وذو دلالة إحصائية عندالمستوى الإحصائي. علاوة على ذلك، فإن المعامل أكبر في الصناعات ذات التلوث الثقيل، مما يشير إلى أن دور IMPP في تعزيز أداء ESG أكثر وضوحًا في الشركات ذات التلوث الثقيل. قد تنبع أسباب هذه الظاهرة من أن الشركات في الصناعات ذات التلوث الثقيل غالبًا ما تكون مصحوبة بكمية كبيرة من استهلاك الطاقة وانبعاثات الملوثات في عملية الإنتاج. من خلال اعتماد أنماط الإنتاج الذكية، تعزز هذه الشركات استخدام تقنيات ومعدات أكثر صداقة للبيئة، مما يتماشى مع المتطلبات.

الجدول 6 تحليل التباين.

المتغيرات

(1)

مملوك للدولة

(2)

غير مملوك للدولة

(٤)

غير تقني

(3)

تكنولوجيا متقدمة

(5)

مُلوِّث بشدة

(6)

غير ملوث بشكل كبير

IMPP

1.183

(0.754)

3.597***

(1.016)

2.504**

(1.089)

2.201***

(0.761)

3.488***

(0.444)

2.463***

(0.724)

ثابت

42.620***

(5.266)

57.019***

(3.555)

57.143***

(4.357)

٥٦.٢٤٥***

(3.913)

56.721***

(5.374)

٥٦.٢٣٢***

(3.441)

التحكمات

نعم

نعم

نعم

نعم

نعم

نعم

شركة في

نعم

نعم

نعم

نعم

نعم

نعم

سنة FE

نعم

نعم

نعم

نعم

نعم

نعم

ر

0.062

0.061

0.045

0.054

0.057

0.051

ن

8588

15002

١٠١٠٤

13486

6928

16662

تقدم الجدول التحليل غير المتجانس استنادًا إلى ملكية الشركات، ومستوى التكنولوجيا الصناعية، ومستوى التلوث. تظهر الأعمدة (1) و(2) النتائج عندما يتم تصنيف المؤسسات على أنها مملوكة للدولة وغير مملوكة للدولة. تعرض الأعمدة (3) و(4) الانحدار للمؤسسات عالية التقنية وغير التقنية. الأعمدة (5) و(6) هي نتائج المؤسسات ذات التلوث الثقيل وغير ذات التلوث الثقيل. جميع الانحدارات تتحكم في تأثيرات الشركة والسنة الثابتة. المتغيرات الضابطة هي نفسها كما هو مذكور أعلاه، والنتائج متاحة في الجدول A6 في الملحق. ** و *** تشير إلى مستويات الدلالة 5% و1%، على التوالي، مع الأخطاء المعيارية المجمعة بين قوسين.

الجدول 7 تحليل الآلية.

(1)

(2)

(3)

(4)

المتغيرات

جي تي

البيئة والمجتمع والحوكمة

Fd

البيئة والمجتمع والحوكمة

IMPP

0.583*** (0.146)

2.476*** (0.621)

-0.237* (0.128)

2.572*** (0.624)

جي تي

0.233*** (0.056)

Fd

-0.164*** (0.042)

ثابت

1.064*** (0.353)

1.712*** (0.594)

1.247** (0.528)

1.554*** (0.451)

التحكمات

نعم

نعم

نعم

نعم

شركة FE

نعم

نعم

نعم

نعم

سنة FE

نعم

نعم

نعم

نعم

ر

0.171

0.250

0.134

0.287

ن

23590

23590

23590

23590

تقدم الجدول النتائج استنادًا إلى المعادلتين (11) و(12)، مستكشفة قنوات التأثير لـ IMPP لتحسين أداء الشركات في مجال ESG. تمثل Gt التكنولوجيا الخضراء، وFd هو الفارق المالي، وهما متغيران وسيطان المشار إليهما في النموذج (12). المتغيرات الأخرى هي نفسها المذكورة أعلاه، والنتائج متاحة في الجدول A7 في الملحق. تظهر الأعمدة (1)-(4) النتائج مع الابتكار الأخضر والفارق المالي كمتغيرات وسيطة على التوالي. جميع الانحدارات تتحكم في تأثيرات الشركة والسنة الثابتة. *, **، *** تشير إلى مستويات الدلالة.، و ، على التوالي، مع الأخطاء المعيارية المجمعة بين قوسين.

قوانين وأنظمة حماية البيئة، مما يؤدي إلى تحسين أكثر وضوحًا في أداء ESG.

مزيد من المناقشة

تحليل الآلية. أظهرت الدراسات التجريبية السابقة أن المشاركة في IMPP تسهم في تحسين أداء الشركات في مجال ESG. بناءً على ذلك، تستكشف هذه الفقرة الآليات المحتملة، مع التركيز بشكل خاص على دور الابتكار في التكنولوجيا الخضراء وتأثير تخصيص الموارد المالية.

أثر ابتكار التكنولوجيا الخضراء. تشير التحليلات النظرية إلى أن التصنيع الذكي يمكن أن يحسن أداء ESG من خلال تعزيز ابتكار التكنولوجيا الخضراء. تستخدم هذه الفقرة Gt كمتغير وسيط للتحقق. تظهر النتائج في العمودين (1) و(2) من الجدول 7. في العمود (1)، حيث المتغير التابع هو معامل IMPP إيجابي وذو دلالة إحصائية عندالمستوى. وهذا يشير إلى أن التصنيع الذكي يساهم في زيادة درجة الابتكار الأخضر في الشركات. في العمود (2)، يكشف أنالمعامل إيجابي وذو دلالة إحصائية عند المستوى. وبالمثل، فإن معامل IMPP أيضًا إيجابي عند مستوى للدلالة الإحصائية. هذا يعني أنه عندما يتم اختبار تأثيرات المتغير الآلي Gt والمتغير الرئيسي IMPP على ESG في نفس الوقت في النموذج (12)، فإن معامل التأثير المباشر ( ) من IMPP له دلالة، و معامل ( ) من آلية المتغير كما أن ذلك مهم أيضًا. علاوة على ذلك، فإن معامل IMPP أصغر من ذلك الخاص بالانحدار الأساسي الموضح في العمود الرابع من الجدول 2. تظهر هذه النتائج أن تأثير التحسين للتصنيع الذكي على ESG يتكون من أجزاء مباشرة وغير مباشرة. يتم نقل جزء عبر المتغير الوسيطحيث يعزز IMPP أداء الشركات في مجال ESG من خلال تعزيز الابتكار الأخضر، ويلعب هذا الابتكار دورًا وسيطًا جزئيًا فقط في تعزيز ESG. جانب آخر يتعلق بالتأثير الفوري لـ IMPP على المتغير التابع ESG. تتماشى نتائجنا مع ما وجده هوانغ وآخرون (2022). السبب هو أن التصنيع الذكي يمكن أن يحفز الشركات على تحديث التكنولوجيا باستمرار، والوفاء بشكل أفضل بالمسؤوليات الاجتماعية، وتحسين أداء ESG من خلال الترقية في نهاية الإنتاج وطلب الإنتاج المخصص في نهاية المستهلك. تم تأكيد الفرضية 2.

أثر تخصيص الموارد المالية. في التحليل النظري السابق، قد تعمل التصنيع الذكي أيضًا على تحسين أداء ESG من خلال التخصيص الأمثل للموارد المالية. في هذا الجزء، يتم استخدام Fd كمتغير بديل للتحليل التجريبي وتُعرض نتائج الانحدار في العمودين (3) و(4) من الجدول 7. في العمود (3)، المتغير المفسر هو، ومعامل IMPP له دلالة سلبية عند المستوى. هذا يُظهر أن التصنيع الذكي يساعد في تخفيف الاضطراب المالي، مما يُحسن كفاءة تخصيص الموارد المالية. في العمود (4)، نجد أن المعامل سالب ومعامل IMPP موجب، وكلا المعاملين لهما دلالة إحصائية عند المستوى، مما يعني أن التصنيع الذكي يمكن أن يخفف من الاضطرابات المالية ويحسن أداء الشركات في مجال البيئة والمجتمع والحوكمة. هذه النتيجة مشابهة لنتائج آلية الابتكار الأخضر، في النموذج (12)، حيث معامل التأثير المباشر ( ) من IMPP على ESG واضح، في حين أن معامل ( ) من متغير الآلية على ESG له أهمية متساوية. علاوة على ذلك، فإن معامل IMPP أصغر مقارنةً بالانحدار الأساسي. تشير النتائج إلى أن تأثير التحسين للتصنيع الذكي على ESG يتكون من جزئيه المباشر وغير المباشر. جزء من النقل يتم من خلال المتغير الوسيط.بينما يهدف IMPP إلى تحسين أداء ESG من خلال تخفيف التوزيع غير العقلاني للموارد المالية. ومن الجدير بالذكر أن إعادة تخصيص الموارد المالية تلعب فقط دورًا وسيطًا جزئيًا في تعزيز ESG. الجزء الآخر هو أن التصنيع الذكي يعزز مباشرة أداء ESG. تم تأكيد الفرضية 3. هذا

الجدول 8 اختبار الأثر الاقتصادي.

(1)

(2)

(3)

المتغيرات

جي تي إف بي

الاتحاد الأوروبي

تي سي

IMPP

0.004**

-0.001

0.005**

(0.002)

(0.002)

(0.002)

ثابت

0.802***

0.794***

1.008***

(0.006)

(0.006)

(0.009)

التحكمات

نعم

نعم

نعم

شركة FE

نعم

نعم

نعم

سنة FE

نعم

نعم

نعم

ر

0.474

0.385

0.351

ن

23590

23590

23590

تُظهر الجدول الأثر الاقتصادي للتصنيع الذكي على الإنتاجية الكلية الخضراء (GTFP) كما هو مستمد من المعادلة (9). المتغير التابع في العمود (1) هو GTFP المحسوب بناءً على نموذج SBM-ML. المتغيرات التابعة في العمودين (2) و(3) هي مكونات EC وTC البيئية بعد تحليل GTFP. المتغيرات الأخرى متوافقة مع النماذج المذكورة أعلاه، والنتائج متاحة في الجدول A8 في الملحق. **، *** تشير إلى مستويات الدلالة 5% و1%، على التوالي، مع الأخطاء المعيارية المجمعة في الأقواس.

النتيجة تتماشى مع الأدبيات الموجودة (غولدفارب وتاكر، 2019؛ يانغ، 2022). التصنيع الذكي يعزز قيمة الشركات وأداء ESG من خلال تقليل تكلفة استخدام رأس المال وتحسين كفاءة الاستخدام.

تحليل الأثر الاقتصادي. تتناول هذه القسم المزيد من الآثار الاقتصادية للتصنيع الذكي كما تقاس بإنتاجية العوامل الكلية الخضراء (GTFP). بالإشارة إلى قاو وآخرون.نحن نتبنى نموذج قياس مالموكويست-لويينبرغر القائم على السلاكس (SBM-ML) لحساب الإنتاجية البيئية العامة للشركات (GTFP). بالإضافة إلى ذلك، نقوم بتفكيكها إلى التأثيرات الناتجة عن تغيير الكفاءة (EC) والتقدم التكنولوجي (TP). يشير EC إلى تحسين GTFP الناتج عن تحسين إدارة التنظيم وتعديل الهيكل الصناعي في ظل الظروف التقنية المعطاة. بينما يشير TP إلى النمو الذي تحقق من GTFP بعد إدخال الابتكارات التكنولوجية الخضراء.

تظهر النتائج في الجدول 8. GTFP هو المتغير المفسر في العمود (1)، ويظهر معامل IMPP قيمة إيجابية وذات دلالة إحصائية عندالمستوى. في العمود (2)، حيث المتغير التابع هو EC، يظهر معامل IMPP سالبًا، على الرغم من أنه ليس ذا دلالة إحصائية. على العكس، تكشف نتيجة TC في العمود (3) أن معامل IMPP إيجابي ويحقق دلالة إحصائية عندهذا يشير إلى أن ارتفاع GTFP المدفوع بالتصنيع الذكي يُعزى بشكل أساسي إلى تحسين المستويات التكنولوجية، وأن تأثير كفاءة إدارة المنظمات ليس له دلالة كبيرة.

قد تكمن الأسباب في حقيقة أنه عندما تتبنى المؤسسات التصنيع الذكي، فإنها غالبًا ما تعطي الأولوية لتطبيق هذه التقنيات في الإنتاج العملي. تميل التعديلات في إدارة التنظيم إلى التأخر عن وتيرة تطبيق التكنولوجيا، مما يتطلب المزيد من الوقت للتكيف وهضم هذه التغييرات، مثل تعديل حجم التوظيف لعمال خط الإنتاج والفنيين (ليو وآخرون، 2020). حتى عندما تتأخر استراتيجية إدارة المؤسسات عن تطوير تكنولوجيا التصنيع الذكي، قد يؤدي ذلك إلى مشاكل مثل تخصيص الموارد بشكل غير معقول ويحد من فوائد تكنولوجيا التصنيع الذكي. من ناحية أخرى، تتطور تكنولوجيا التصنيع الذكي نفسها بسرعة، والتقنيات المتقدمة مثل إنترنت الأشياء والذكاء الاصطناعي تتجدد باستمرار (شليمتيز ومزهويف، 2024). يركز تطبيق هذه التقنيات بشكل أكبر على عمليات الإنتاج وابتكار المنتجات، مما يجعل تأثير IMPP على TC أكثر أهمية من تأثير EC.

الخاتمة وآثار السياسات

تقوم هذه الدراسة بتحليل والتحقق مما إذا كانت التصنيع الذكي يساهم في تعزيز أداء الشركات في مجال ESG من خلال التحليل النظري والتجريبي. باستخدام بيانات الشركات المدرجة في سوق الأسهم الصينية من 2009 إلى 2021، نعتبر تنفيذ برامج تجريبية للتصنيع الذكي ك تجربة شبه طبيعية ونستخدم نموذج DID المتقطع للاختبارات التجريبية. تظهر النتائج أن الشركات المشاركة في برامج التصنيع الذكي يمكن أن تحسن بشكل كبير من أداء ESG. تكشف تحليل الآلية أنها يمكن أن تعزز أداء ESG للشركات من خلال مسارين: تعزيز الابتكار في التكنولوجيا الخضراء وتقليل سوء تخصيص الموارد المالية. علاوة على ذلك، نجد من خلال تحليل التباين أن تأثير تحسين التصنيع الذكي على ESG يكون أكثر وضوحًا في الشركات غير المملوكة للدولة، والشركات عالية التقنية، والشركات ذات التلوث الثقيل. بالإضافة إلى ذلك، نجد أن التأثير الاقتصادي للتصنيع الذكي على الإنتاجية الإجمالية لعوامل الإنتاج الخضراء، يتم بشكل رئيسي من خلال تحسين التقدم في التكنولوجيا الخضراء.

تقدم هذه الورقة أدلة تجريبية على تنفيذ برامج تجريبية للتصنيع الذكي وتشجيع الشركات على تعزيز أداء ESG. وبناءً عليه، نقدم أيضًا الآثار السياسية التالية. أولاً، يجب علينا تسريع تطوير التصنيع الذكي، وتوسيع الأنشطة العملية للتصنيع الذكي، وتعزيز أداء ESG للشركات. مقارنةً بمشاكل انخفاض كفاءة الإنتاج وعدم التماثل في المعلومات في نمط الإنتاج التقليدي، لا يقوم التصنيع الذكي فقط بتحسين تخصيص موارد الشركات، بل يدفع أيضًا الشركات للوفاء بمسؤولياتها الاجتماعية بشكل أفضل وتحسين أداء ESG. لذلك، من الضروري زيادة نطاق برامج التصنيع الذكي التجريبية، على سبيل المثال، من خلال تحسين تدابير الحوافز أو السياسات الضريبية التفضيلية لشركات التصنيع الذكي، لتعزيز مشاركة الشركات المصنعة ذات الصلة، ومن ثم تحسين أداء ESG.

ثانياً، يجب على الحكومة تعزيز الابتكار في التكنولوجيا الخضراء وسياسات التمويل الأخضر المتعلقة بالتصنيع الذكي، وإطلاق العنان بالكامل لدور رأس المال وكذلك عوامل التكنولوجيا في تطوير التصنيع الذكي. نجد أن الابتكار الأخضر والفجوة المالية تلعبان دوراً جزئياً في تحسين ESG للتصنيع الذكي. لذلك، يجب على الحكومة اغتنام الفرصة للتنمية عالية الجودة في تكنولوجيا المعلومات وصناعة التصنيع، وتحسين نظام الابتكار التكنولوجي والتطبيق، وتوجيه الأموال الاجتماعية للاستثمار في مجال التصنيع الذكي. في الوقت نفسه، من الضروري أيضاً تعزيز الإصلاحات الحديثة في إدارة الشركات، مثل الإدارة الاستراتيجية للشركات لتتكيف بشكل أكبر مع أحدث أنماط الإنتاج، وتعظيم الاستفادة من العوائد التي يجلبها التصنيع الذكي.

ثالثًا، يمكن للحكومة تنفيذ سياسات تفضيلية تستهدف الشركات ذات التلوث العالي وكذلك الشركات غير المملوكة للدولة، مما يشجعها على المشاركة بنشاط في التحول الذكي. وتظهر النتائج التجريبية أن تأثير تحسين ESG في التصنيع الذكي يكون أكثر وضوحًا في الشركات ذات التلوث العالي، والشركات غير المملوكة للدولة، والشركات عالية التقنية. لذلك، يجب أخذ احتياجات هذه الشركات بعين الاعتبار بشكل كامل عند تعزيز سياسات التصنيع الذكي، ويجب توجيه الشركات لاستخدام تكنولوجيا التصنيع المتقدمة للتحول إلى الأخضر وتعزيز ممارسات ESG من خلال زيادة الدعم السياسي أو الحوافز الضريبية.

رابعًا، يمكن تطبيق الرؤى التي اكتسبتها الصين في سياسات التصنيع الذكي على اقتصادات ناشئة أخرى، بهدف تعزيز تقدمها في الابتكار التكنولوجي. ونمو مستدام. على الرغم من وجود اختلافات ثقافية ومؤسسية بين الصين وغيرها من الاقتصادات، مثل سرعة اعتماد التقنيات الجديدة، قد تتأخر بعض الدول، أو قد يكون لدى بعض الحكومات تدخل اقتصادي أقل، مما يؤدي إلى اتخاذ قرارات أقل كفاءة. ومع ذلك، لا يزال نموذج التنمية في الصين يحمل قيمة للإشارة والترويج في سياق الاقتصاد الرقمي والتحول التكنولوجي. يمكن للدول الأخرى صياغة سياسات مناسبة بناءً على ظروفها الوطنية، ومن خلال التخطيط الشامل للنظام والتوجه الاستراتيجي، بما في ذلك الدعم المالي والمساعدات المالية، لتعزيز تطوير صناعات التصنيع الذكي.

على الرغم من أننا تحققنا من تأثير تحسين التصنيع الذكي على أداء ESG من الجوانب النظرية والتجريبية، وناقشنا دور الابتكار الأخضر وتخصيص الموارد المالية، إلا أننا نعترف أنه بسبب قيود المساحة، سيكون هناك أيضًا بعض النواقص. على سبيل المثال، لا تناقش هذه الورقة قابلية تطبيق هذا الاستنتاج في دول أخرى، كما أنها لا تناقش التأثير التفاضلي للتصنيع الذكي على العناصر الفرعية لـ ESG وتقدير مساهمة كل وسيط في تحسينات ESG. لذلك، يمكن أن تستكشف الأبحاث المستقبلية التأثير التفاضلي للتصنيع الذكي على العناصر الفرعية لـ ESG وتستخدم متغيرات وسيطة مختلفة لت quantifying المساهمة المحددة لقنوات التأثير، وبالتالي إثراء البحث في المجالات ذات الصلة وتوسيع قابلية تطبيق الاستنتاجات.

توفر البيانات

جميع البيانات في هذه الدراسة تم الحصول عليها من تقارير وقواعد بيانات رسمية، وقد تم وصف المصادر المحددة بالتفصيل في قسم البيانات. تم أخذ البيانات اللازمة لبناء متغير التصنيع الذكي من وزارة الصناعة وتكنولوجيا المعلومات لجمهورية الصين الشعبية. وهي متاحة مجانًا على https://wap.miit.gov.cn. البيانات الأخرى المستخدمة في هذه الدراسة متاحة من قاعدة بيانات CSMAR. المؤلفون غير مخولين بالكشف عن هذه البيانات.

تاريخ الاستلام: 15 أغسطس 2024؛ تاريخ القبول: 1 أبريل 2025؛

تم النشر عبر الإنترنت: 14 أبريل 2025

References

Acemoglu D, Restrepo P (2018) The race between man and machine: Implications of technology for growth, factor shares, and employment. Am Econ Rev 108(6):1488-1542

Acheampong A, Elshandidy T (2021) Does soft information determine credit risk? Textbased evidence from European banks. J Int Financial Mark Inst Money 75:101303

Aroul RR, Sabherwal S, Villupuram SV (2022) ESG, operational efficiency and operational performance: evidence from Real Estate Investment Trusts. Manag Financ 48(8):1206-1220

Azar J, Vives X (2021) General equilibrium oligopoly and ownership structure. Econometrica 89(3):999-1048

Bai F, Shang M, Huang Y (2024) Corporate culture and ESG performance: empirical evidence from China. J Clean Prod 437:140732

Baron RM, Kenny DA (1986) The moderator-mediator variable distinction in social psychological research: conceptual, strategic, and statistical considerations. J Personal Soc Psychol 51:1173-1182

Barros V, Matos PV, Sarmento JM, Vieira PR (2022) M&A activity as a driver for better ESG performance. Technol Forecast Soc Change 175:121338

Best R, Sinha K (2021) Fuel poverty policy: Go big or go home insulation. Energy Econ 97:105195

Biswas I, Singh G, Tiwari S, Choi TM, Pethe S (2024) Managing Industry 4.0 supply chains with innovative and traditional products: contract cessation points and value of information. Eur J Operat Res 316(2):539-555

Braganza A, Brooks L, Nepelski D, Ali M, Moro R (2017) Resource management in big data initiatives: processes and dynamic capabilities. J Bus Res 70:328-337

de Paula Ferreira W, Armellini F, de Santa-Eulalia LA, Thomasset-Laperrière V (2022) A framework for identifying and analysing industry 4.0 scenarios. J Manuf Syst 65:192-207

Drempetic S, Klein C, Zwergel B (2020) The influence of firm size on the ESG score: corporate sustainability ratings under review. J Bus Ethics 167(2):333-360

Feng N, Tu S, Guo F (2024) Big-data analytics capability, value creation process, and collaboration innovation quality in manufacturing enterprises: a knowledge-based view. Comput Ind Eng 187:109804

Gao D, Feng H, Cao Y (2024a) The spatial spillover effect of innovative city policy on carbon efficiency: evidence from China. Singapore Econ Rev 1-23. https:// doi.org/10.1142/S0217590824500024

Gao, D, Tan, L, Duan, K (2024b) Forging a path to sustainability: the impact of Fintech on corporate ESG performance. Eur J Finance, 1-19. https://doi.org/ 10.1080/1351847X.2024.2416995

Gao D, Zhou X, Wan J (2024c) Unlocking sustainability potential: the impact of green finance reform on corporate ESG performanc. Corp Soc Responsib Environ Manage 31(5):4211-4226

Gao D, Zhou X, Mo X, Liu X (2024d) Unlocking sustainable growth: exploring the catalytic role of green finance in firms’ green total factor productivity. Environ Sci Pollut Res 31(10):14762-14774

Giannopoulos G, Kihle Fagernes RV, Elmarzouky M, Afzal Hossain KABM (2022) The ESG disclosure and the financial performance of Norwegian listed firms. J Risk Financial Manag 15(6):237

Goldfarb A, Tucker C (2019) Digital economics. J Econ Lit 57(1):3-43

Hainmueller J (2012) Entropy balancing for causal effects: a multivariate reweighting method to produce balanced samples in observational studies. Political Anal 20(1):25-46

Hao X, Sun Q, Li K, Li P, Wu H (2024) Does environmental decentralisation improve ESG performance? Evidence from listed companies in China. Energy Econ 139:107932

He F, Ding C, Yue W, Liu G (2023) ESG performance and corporate risk-taking: evidence from China. Int Rev Financial Anal 87:102550

Hillman AJ, Dalziel T (2003) Boards of directors and firm performance: integrating agency and resource dependence perspectives. Acad Manag Rev 28(3):383-396

Huang G, He LY, Lin X (2022) Robot adoption and energy performance: evidence from Chinese industrial firms. Energy Econ. 107:105837

Huang J, Wang Y, Luan B, Zou H, Wang J (2023) The energy intensity reduction effect of developing digital economy: theory and empirical evidence from China. Energy Econ 128:107193

Huang X, Ren Y, Ren X (2024) Legal background executives, corporate governance and corporate ESG performance. Financ Res Lett 69:106120

Jacobson LS, LaLonde RJ, Sullivan DG (1993) Earnings losses of displaced workers. Am Econ Rev 83(4):685-709

Jia R (2014) The legacies of forced freedom: China”s treaty ports. Rev Econ Stat 96(4):596-608

Jun X, Ai J, Zheng L, Lu M, Wang J (2024) Impact of information technology and industrial development on corporate ESG practices: evidence from a pilot program in China. Econ Model 139:106806

Kong D, Ji M, Liu L (2024) Parent firm dividend payouts and subsidiary earnings management: evidence from mandatory dividend policy. J. Account Public Policy 44:107192

Lei N, Miao Q, Yao X (2023) Does the implementation of green credit policy improve the ESG performance of enterprises? Evidence from a quasi-natural experiment in China. Econ Model. 127:106478

Li G, Branstetter LG (2024) Does “Made in China 2025” work for China? Evidence from Chinese listed firms. Res Policy 53(6):105009

Li J, Wu T, Liu B, Zhou M (2024) Can digital transformation enhance corporate ESG performance? The moderating role of dual environmental regulations. Finance Res Lett 62:105241

Liu S, Ma S, Yin L, Zhu J (2023) Land titling, human capital misallocation, and agricultural productivity in China. J Dev Econ 165:103165

Lu S, Cheng B (2023) Does environmental regulation affect firms’ ESG performance? Evidence from China. Manag Decis Econ 44(4):2004-2009

Lu Y, Xu X (2019) Cloud-based manufacturing equipment and big data analytics to enable on-demand manufacturing services. Robot Comput Integr Manuf 57:92-102

Lu Y, Xu C, Zhu B, Sun Y (2024) Digitalization transformation and ESG performance: Evidence from China. Bus Strategy Environ 33(2):352-368

Lv W, Ma W, Yang X (2022) Does social security policy matter for corporate social responsibility? Evidence from a quasi-natural experiment in China. Econ Model. 116:106008

Lyu C, Yang J, Zhang F, Teo TS, Guo W (2020) Antecedents and consequence of organizational unlearning: evidence from China. Ind Mark Manag 84:261-270

Ma S, Zhang Y, Liu Y, Yang H, Lv J, Ren S (2020) Data-driven sustainable intelligent manufacturing based on demand response for energy-intensive industries. J Clean Prod 274:123155

Melitz MJ (2003) The impact of trade on intra-industry reallocations and aggregate industry productivity. Econometrica, 71(6):1695-1725

Mintah EO, Elmarzouky M (2024) Digital-platform-based ecosystems: CSR innovations during crises. J Risk Financial Manag 17(6):247

Moussa AS, Elmarzouky M (2023) Does capital expenditure matter for ESG disclosure? A UK perspective. J Risk Financial Manag 16(10):429

Moussa AS, Elmarzouky M (2024a) Sustainability reporting and market uncertainty: the moderating effect of carbon disclosure. Sustainability 16(13):5290

Moussa AS, Elmarzouky M (2024b) Beyond compliance: how ESG reporting and strong governance influence financial performance in UK firms. J Risk Financial Manag 17(8):326

Moussa AS, Elmarzouky M, Shohaieb D (2024) Green Governance: how ESG initiatives drive financial performance in UK Firms? Sustainability 16(24):10894

Peng Y, Tao C (2022) Can digital transformation promote enterprise performance? – From the perspective of public policy and innovation. J Innov Knowl 7(3):100198

Qi W, Li B, Liu Q, Lv J (2023) Low-skill lock-in? Financial resource mismatch and low-skilled labor demand. Financ Res Lett 55:104003

Quan XF, Li C (2022) Intelligent manufacturing and cost stickiness: a quasi-natural experiment from China’s intelligent Manufacturing demonstration project. Econ Res 57(04):68-84

Rana J, Daultani Y (2023) Mapping the role and impact of artificial intelligence and machine learning applications in supply chain digital transformation: a bibliometric analysis. Oper Manag Res 16(4):1641-1666

Schlemitz A, Mezhuyev V (2024) Approaches for data collection and process standardization in smart manufacturing: systematic literature review. J Ind Inf Integr 38:100578

Shen Y, Zhang X (2023) Intelligent manufacturing, green technological innovation and environmental pollution. J Innov Knowl 8(3):100384

Song J, Chen Y, Luan F (2023) Air pollution, water pollution, and robots: Is technology the panacea. J Environ Manag 330:117170

Tang H, Tong M, Chen Y (2024) Green investor behavior and corporate green innovation: evidence from Chinese listed companies. J Environ Manag 366:121691

Tang M, Wang Y (2022) Tax incentives and corporate social responsibility: the role of cash savings from accelerated depreciation policy. Econ Model 116:106040

Venturini F (2022) Intelligent technologies and productivity spillovers: evidence from the Fourth Industrial Revolution. J Econ Behav Organ 194:220-243

Wang K, Chen X, Wang C (2023) The impact of sustainable development planning in resource-based cities on corporate ESG-Evidence from China. Energy Econ 127:107087

Wang SM, Wang M, Feng C (2024) Deleveraging and green technology innovation: evidence from Chinese listed companies. Res Int Bus Finance 69:102289

Wei X, Jiang F, Chen Y, Hua W (2024) Towards green development: the role of intelligent manufacturing in promoting corporate environmental performance. Energy Econ 131:107375

Wu G, Liu Y (2024) Production automation and financial cost control based on intelligent control technology in sustainable manufacturing. Int J Adv Manufacturing Technol 1-10. https://doi.org/10.1007/s00170-024-13059-z

Yang CH (2022) How artificial intelligence technology affects productivity and employment: firm-level evidence from Taiwan. Res. Policy 51(6):104536

Yang J, Ying L, Gao M (2020) The influence of intelligent manufacturing on financial performance and innovation performance: the case of China. Enterp Inf Syst 14(6):812-832

Ye X, Tian X (2024) Green finance and ESG performance: a Quasi-Natural experiment on the influence of green financing pilot zones. Res Int Bus Finance 73:102647

Yin H, Li C (2022) Can intelligent manufacturing empower enterprise innovation? A Quasi-Natural experiment based on China”s intelligent manufacturing demonstration project. J Financial Res 10:98-116

Yin Z, Li X, Si D, Li X (2023) China stock market liberalization and company ESG performance: the mediating effect of investor attention. Econ Anal Policy 80:1396-1414

Yu H, Su T (2024) ESG performance and corporate solvency. Financ Res Lett 59:104799

Zeba G, Dabić M, Čičak M, Daim T, Yalcin H (2021) Technology mining: artificial intelligence in manufacturing. Technol Forecast Soc Change 171:120971

Zhang D, Meng L, Zhang J (2023) Environmental subsidy disruption, skill premiums and ESG performance. Int Rev Financial Anal 90:102862

Zhang G, Lee Y (2021) Determinants of financial performance in China”s intelligent manufacturing industry: Innovation and liquidity. Int J Financial Stud 9(1):15

Zhang Y, Wan D, Zhang L (2024) Green credit, supply chain transparency and corporate ESG performance: evidence from China. Financ Res Lett 59:104769

Zhong M, Gao L (2017) Does corporate social responsibility disclosure improve firm investment efficiency? Evidence from China. Rev Account Financ 16(3):348-365

Zhou G, Liu L, Luo S (2022a) Sustainable development, ESG performance and company market value: mediating effect of financial performance. Bus Strategy Environ 31(7):3371-3387

Zhou J, Li P, Zhou Y, Wang B, Zang J, Meng L (2018) Toward new-generation intelligent manufacturing. Engineering 4(1):11-20

Zhou L, Jiang Z, Geng N, Niu Y, Cui F, Liu K, Qi N (2022b) Production and operations management for intelligent manufacturing: a systematic literature review. Int J Prod Res 60(2):808-846

Zhu M, Liang C, Yeung AC, Zhou H (2024) The impact of intelligent manufacturing on labor productivity: an empirical analysis of Chinese listed manufacturing companies. Int J Prod Econ 267:109070

الشكر والتقدير

تم دعم هذا العمل من قبل مشروع تخطيط الفلسفة والعلوم الاجتماعية في مقاطعة هاينان (رقم HNSK(JD)22-4)، مؤسسة الشباب للعلوم الإنسانية والاجتماعية، وزارة التعليم (رقم 24YJC790043)، صناديق بدء البحث في جامعة هاينان (رقم kyqd(sk)2022030)، ومؤسسة العلوم الطبيعية في مقاطعة هاينان في الصين (رقم 722QN293).

مساهمات المؤلفين

دا قاو: التصور، الموارد، المنهجية، التحليل النوعي، ومراجعة الكتابة والتحرير. لينفانغ تان: التحقيق، تنظيم البيانات، وإدارة المشروع. يوي تشين: التصور، الموارد، المنهجية، التحليل النوعي، الكتابة، إعداد المسودة الأصلية، والمراجعة.

المصالح المتنافسة

يعلن المؤلفون عدم وجود مصالح متنافسة.

الموافقة الأخلاقية

لا تحتوي هذه المقالة على أي دراسات مع مشاركين بشريين أجراها أي من المؤلفين.

الموافقة المستنيرة

لا تحتوي هذه المقالة على أي دراسات مع مشاركين بشريين أجراها أي من المؤلفين.

يجب توجيه المراسلات وطلبات المواد إلى يوي تشين.

معلومات إعادة الطبع والإذن متاحة على http://www.nature.com/reprints

ملاحظة الناشر تظل Springer Nature محايدة فيما يتعلق بالمطالبات القضائية في الخرائط المنشورة والانتماءات المؤسسية.

كلية القانون والأعمال، معهد ووهان للتكنولوجيا، ووهان، الصين. كلية الأعمال الدولية، جامعة هاينان، هايكو، الصين. البريد الإلكتروني: chen_yue@hainanu.edu.cn

Smarter is greener: can intelligent manufacturing improve enterprises’ ESG performance?

Da Gao , Linfang Tan & Yue Chen

Environmental, Social, and Governance (ESG) is highly consistent with the “Dual Carbon” goals proposed by China and has become an important indicator to measure enterprises’ high-quality development. This study explores the impact of intelligent manufacturing on corporate ESG performance and its potential mechanisms. Using the dataset of China’s A-share listed companies from 2009 to 2021, we treat the intelligent manufacturing pilot programs (IMPP) as a quasi-natural experiment and use the staggered difference-indifference model for empirical analysis. The results show that corporate ESG performance is significantly improved after participating in IMPP, and the placebo and entropy balancing tests further reconfirm the results. The mechanism analysis shows that IMPP works in two main ways: promoting enterprises’ green innovation and reducing the misallocation of financial resources. The heterogeneity analysis shows that the IMPP significantly improves the ESG performance of Non-state-owned, high-tech, and heavy-polluting enterprises. In addition, the IMPP improves the enterprises’ green total factor productivity and brings significant economic benefits. This study has far-reaching policy implications for promoting the quality-driven development of China’s manufacturing industry and the sustainable development of enterprises.

Introduction

nder the goals of “carbon peak” and “carbon neutrality” proposed by the Chinese government, how to alleviate resource constraints and achieve sustainable economic development has become an important issue (Zhou et al., 2022a, Bai et al., 2024). As key market players, enterprises represent an essential force in implementing the concept of green development and their ESG performance has been widely concerned (Giannopoulos et al., 2022; Gao et al., 2024a, 2024c, Moussa et al., 2024). Existing studies have found the profound impact of ESG performance on financial performance and market uncertainty (Moussa and Elmarzouky, 2023; Moussa and Elmarzouky, 2024a; Moussa and Elmarzouky, 2024b). However, ESG practice is still faced with problems such as high input cost and uncertain output, resulting in insufficient actual ESG input. How to stimulate the motivation of enterprises to expand ESG investment and promote ESG performance has become an urgent concern in academic and practical fields.

Meanwhile, intelligent manufacturing, as a product of the deep integration of information technology and manufacturing techniques, leads to the upgrading of the manufacturing industry and the enterprise’s sustainable development (Li and Branstetter, 2024). Compared with the automatic control of a single equipment or production line based on preset programming, the advantages of intelligent manufacturing in production decisionmaking are incomparable. For instance, the Industry 4.0 application practice of the Bosch factory in Germany leverages radio frequency identification and other Internet of Things technologies to interface with management information systems such as enterprise resource planning, product lifecycle management, and supply chain management (de Paula Ferreira et al., 2022; Biswas et al., 2024). This seamless integration across the upstream and downstream of the supply chain enables automatic data flow in production, optimizing the allocation efficiency and reducing resource waste. Therefore, intelligent manufacturing can enhance ESG performance by improving information transparency and resource utilization efficiency, enhancing supply chain synergy, and meeting stakeholders’ expectations for sustainable development.

Specifically, intelligent manufacturing enables real-time data collection and information sharing across the supply chain by integrating equipment, production lines, and manufacturing systems. From the perspective of information asymmetry theory, this transparency of information improves the collaborative efficiency of the supply chain and can improve enterprises’ ESG performance (Gao et al., 2024b). In addition, the intelligent manufacturing system can carry out in-depth mining and analysis of production data to achieve more accurate decision-making, which can minimize waste (Huang et al., 2022). From the perspective of the stakeholder theory, the above practices not only meet the expectations of stakeholders such as consumers, investors, and regulators for environmental protection, but they can also further enhance the enterprises’ ESG performance by improving resource utilization efficiency.

However, the existing literature lacks detailed empirical analyses on the ESG outcomes of intelligent manufacturing at the firm level. Some studies have confirmed that intelligent manufacturing can promote enterprises’ technological investment and information processing (Braganza et al., 2017), accelerate enterprise’s digital transformation (Zhou et al., 2018), enhance enterprises’ competitive advantage, and upgrade the manufacturing industry (Yang et al., 2020; Zhou et al., 2022b). In other words, most of the existing literature about intelligent manufacturing focuses on the economic impact brought by the adoption of intelligent manufacturing mode and pays less attention to the impact on corporate social responsibility performance. Even if

relevant, the research focuses solely on environmental pollution (Song et al. 2023; Shen and Zhang, 2023), employment (Acemoglu and Restrepo, 2018), supply chain management (Goldfarb and Tucker, 2019), and other single dimensions. For example, Song et al. (2023) examined the impact of automation and intelligent technology on the environment and found that the increasing level of production technology such as robot adoption contributes to pollution abatement.

To address the lack of micro-evidence on the impact of intelligent manufacturing on firms’ sustainable transformation, this study empirically examines the impact of intelligent manufacturing pilot programs (IMPP) on corporate ESG performance by constructing a unified analytical framework. We focus on answering the following questions: (1) Can IMPP help enterprises fulfill their social responsibilities and improve ESG performance? (2) What are the impact channels through which IMPP affects ESG performance? (3) Does the impact vary depending on corporate characteristics?

Therefore, this study treats the IMPP as a quasi-natural experiment to investigate the causal relationship between intelligent manufacturing and corporate ESG performance. We first divide firms into treatment and control groups according to their participation in the IMPP, and then we adopt the staggered difference-in-difference method for empirical tests. The results show that IMPP can improve corporate ESG performance and the conclusion is still valid in a series of robustness tests. The mechanism analysis shows that green innovation and financial resource allocation are two important impact channels, which are partial mediation. In addition, we also find that the enhancement effect of IMPP on ESG performance is more pronounced in nonstate, high-tech, and heavy-polluting enterprises.

The marginal contributions of this paper are as follows: First, we integrate intelligent manufacturing and corporate ESG performance into a comprehensive analytical framework. Compared with the existing studies on mergers and acquisitions (Barros et al., 2022), corporate culture (Bai et al., 2024), social security policies (Lv et al., 2022), tax incentives (Tang and Wang, 2022), technological innovations (Mintah and Elmarzouky, 2024; Lu et al., 2024) and other internal and external factors affecting ESG performance, this study aims to start from the perspective of intelligent manufacturing and treat IMPP as a quasi-natural experiment to reveal the causal effect in promoting enterprises’ sustainable development. This paper provides a new perspective for understanding the multi-dimensional factors affecting ESG performance.

Second, this paper aims to deeply explore the positive effects of IMPP on corporate ESG performance by combining theoretical deduction and empirical analysis. Most of the existing literature empirically studies the impact of intelligent manufacturing on innovation and production performance (Li and Branstetter, 2024; Venturini, 2022), this paper analyzes the possible impact of intelligent manufacturing on ESG performance from the theoretical perspective and then uses the data of Chinese listed companies for empirical analysis. The results not only enrich the theoretical system of intelligent manufacturing, but also provide valuable decision support for policymakers when implementing intelligent manufacturing strategy.

Third, this study further reveals the impact channels of intelligent manufacturing on enterprises’ ESG performance. Compared with existing studies that discuss the influence mechanism through digital transformation and organizational transformation (Rana and Daultani, 2023; Zeba et al., 2021), this study starts from the characteristics of IMPP requirements and explores its role on the enterprises’ ESG performance by promoting corporate green innovation and optimizing the allocation of financial

resources. Our findings extend the micro mechanism of intelligent manufacturing on firms’ green transformation.

The subsequent part of this paper is organized as follows: “Institutional background and theoretical hypothesis” is the institutional background and theoretical hypothesis; “Data and methodology” shows data and methodology; “Empirical analysis” conducts empirical analysis; “Further discussion” involves further discussion, and “Conclusion and policy implications” is the conclusion and policy implications.

Institutional background and theoretical hypothesis

Institutional background. Intelligent manufacturing, as a revolutionary innovation in modern industrial development, has a profound impact on global industrial upgrading and become the focus of competition among countries. For example, the USA put forward “the Advanced Manufacturing Leadership Strategy”, Germany advocated “the National Industrial Strategy 2030”, France’s “New Industrial France Plan”, and Japan’s “Society 5.0”. In line with similar goals, China has launched several initiatives, such as “Made in China 2025”, and “the Intelligent Manufacturing Development Plan (2016-2020)”. In specific practice, considering that intelligent manufacturing is a complex and huge system engineering, the government has begun to issue “The Notice on Launching of Intelligent Manufacturing Pilot and Demonstration Special Action” to select intelligent manufacturing pilot enterprises since 2015.

The IMPP policy is an important attempt to deeply integrate intelligence manufacturing into green development. For the first time, it incorporates reducing operating costs and product defect rates, shortening product development cycles, improving production efficiency, and enhancing energy use efficiency into the assessment requirements. In fact, after participating in IMPP, enterprises do form comparative advantages in terms of production efficiency, operating cost, and energy utilization efficiency (Yang et al., 2020; Zhang and Lee, 2021; Yin and Li, 2022). This means that intelligent manufacturing not only effectively improves the efficiency of resource allocation, but also brings new opportunities for promoting sustainable development.

Theoretical hypothesis. Based on Azar and Vives (2021) and Lei et al. (2023), this study takes ESG input into enterprises’ production decision-making model. Specifically, we assume that in an imperfectly competitive market with J firms, the production function of the representative firm can be set as , where represents the firms’ total output, A represents the production mode adopted by the enterprise ( or 2 ), representing traditional production and intelligent manufacturing; represents the enterprise’s investment in ESG, represents the enterprise’s capital input, and function measures the production technology. The enterprise’s production is mainly affected by the production mode, ESG input, and capital input, not affected by labor input. Existing literature has proved that ESG performance helps to improve operational efficiency, as well as investment efficiency (Aroul et al., 2022). Therefore, it can be assumed that , that is, if intelligent manufacturing is chosen or ESG input is increased, the technical level of enterprises can be improved accordingly, and the output level would be higher.

We also assume that the cost of each unit of capital input , the cost of each unit of ESG input is , and the production mode chooses per unit of cost input. Product price is , and specifically as a constant. Therefore,

the profit function of firm can be expressed as:

Based on the condition of profit maximization, the first-order partial derivatives of and are following:

According to Eqs. (4) and (5), then we can obtain:

By differentiating Eq. (6) concerning and , we can obtain:

Based on the above calculation, we can get: