DOI: https://doi.org/10.1007/s40822-023-00251-x

تاريخ النشر: 2024-03-01

تغير المناخ، معايير ESG والتنظيمات الحديثة: التحديات والفرص

الملخص

أصبح تطبيق معايير البيئة والمجتمع والحوكمة (ESG) الآن مطلبًا أساسيًا في العالم المالي. لذلك، من الضروري فهم واختيار وتقييم مخاطر هذه المعايير ESG وتقييم كيفية تأثيرها على منتج أو قرار استثماري. وبالتالي، الهدف الرئيسي من هذه المقالة هو تحليل مؤشرات ESG (البيئة، المجتمع والحوكمة) وتأثيراتها المحتملة في إطار المعلومات غير المالية. التطورات التنظيمية الحالية، مثل توجيه الإبلاغ عن الاستدامة المؤسسية الأوروبية (CSRD)، تدفع لجعل مؤشرات ESG (ضمن هذا المنظور الثلاثي: المخاطر الاجتماعية والبيئية والحوكمة) مجموعة رئيسية من المعلومات التي يجب استخدامها من قبل المراسلين ومستخدمي المعلومات. ستدرس هذه المقالة بمزيد من التفصيل الآثار الرئيسية التي ستحدثها هذه التنظيمات في كيفية عكس الشركات لمعلومات البصمة الاجتماعية والبيئية في تقاريرها الخارجية. نظرًا لأن هذه المؤشرات ESG قد تؤثر بشكل كبير على العوامل المالية للشركة، فإن أصحاب المصلحة سيكونون مهتمين بكيفية تعامل الشركات مع هذه المخاطر ESG. لذلك، ستزيد هذه البيانات ESG من الشفافية وستعني فهمًا أفضل لكيفية التزام الشركات والمستثمرين بالاستدامة للتطور نحو اقتصاد محايد للكربون. لفهم التزام الشركة بهذه المعايير ESG، سيتعين على أصحاب المصلحة تقييم جوانب مختلفة من المعلومات المبلغ عنها. في هذا السياق، ستركز هذه المقالة على كيفية دمج وكالات التصنيف الائتماني لهذه المخاطر في تقييماتها. أصبحت وكالات التصنيف الائتماني فاعلين مهمين في معايير الاستدامة، حيث تدمج مخاطر ESG في تقييماتها، مما ينقل أهمية هذه المؤشرات إلى المستثمرين والأسواق. ستنظر هذه الدراسة في الآفاق الزمنية المختلفة بين الربحية المالية ومؤشرات الاستدامة. الاتجاه الحالي والطلب الكبير على المؤشرات غير المالية لا يتمتعان بنفس العمق والإطار والتقاليد مثل المؤشرات المالية. قد يؤدي ذلك إلى وضع يتطلب فترة للتكيف بين العالمين وجعلهما يتصلان معًا بطريقة يحتاج فيها أحدهما إلى الآخر.

الاختصارات

| ESG | البيئة، المجتمع، والحوكمة |

| ECAI | مؤسسات التقييم الائتماني الخارجية |

| UNE | الأمم المتحدة |

| CSR | المسؤولية الاجتماعية للشركات |

| CNMV | اللجنة الوطنية لسوق القيم |

| CG | مدونة الحوكمة/ |

| GREY | مبادرة الإبلاغ العالمية |

| SASB | معيار المحاسبة للاستدامة |

| TFCRFD | فريق العمل المعني بالإفصاحات المالية المتعلقة بالمناخ |

| CDP | مشروع الإفصاح عن الكربون |

| E | الأرباح |

| BV | القيمة الدفترية |

| R | الإيرادات |

| CF | التدفق النقدي |

| D | الأرباح الموزعة |

| W | المتوسط المرجح |

| ROE | العائد على حقوق الملكية |

| NFRD | توجيه الإبلاغ غير المالي |

| CSRD | توجيه الإبلاغ عن الاستدامة المؤسسية |

1 المقدمة

2 تغير المناخ، ومعايير الحوكمة البيئية والاجتماعية، ومخاطر الأعمال

- إزالة الغابات: بفضل عملية التمثيل الضوئي، تمتص الأشجار

وتعيده إلى الغلاف الجوي في شكل أكسجين نشط، بالإضافة إلى كونها منظمين طبيعيين للمناخ. إن إزالة الغابات بشكل غير منضبط يهدد هذا التأثير المفيد. - احتراق الوقود الأحفوري: ينتج احتراق الفحم والنفط والغاز ثاني أكسيد الكربون وأكسيد النيتروز.

- الأسمدة النيتروجينية: تُستخدم هذه الأنواع من الأسمدة بشكل متزايد في الزراعة وتنتج كميات كبيرة من أكسيد النيتروز.

- تربية الماشية: تعتبر الماشية واحدة من المصادر الرئيسية لانبعاثات الميثان. في الواقع، توصي الأمم المتحدة بتقليل استهلاكنا من اللحوم كواحدة من الوصفات الرئيسية لمكافحة تغير المناخ.

- تدمير النظم البيئية البحرية: تعتبر المحيطات أيضًا مصبات لـ

الناتجة. بالإضافة إلى تدميرها، تكمن المشكلة عندما تصل إلى حدها

- زيادة السكان: يستمر عدد سكان العالم في النمو والاستهلاك. يتطلب عدد السكان المتزايد المزيد من الموارد، مما يؤدي إلى زيادة انبعاثات الغازات الدفيئة.

- تشمل المخاطر البيئية تلك التي تتعلق بنشاط الشركة وتأثيرها، سواء بشكل مباشر أو غير مباشر، على البيئة، ويتم التعرف عليها حاليًا كعنصر من عناصر مخاطر تغير المناخ (كيدوارد وآخرون، 2022). لكل نشاط تجاري تأثيرات بيئية. مع تأثير اقتصادي أكبر أو أقل، ما هو مؤكد هو أن الامتثال لهذه المعايير البيئية يُقدَّر بشكل متزايد ككفاءة وشفافية وجودة والتزام الشركة (غوبتا وآخرون، 2016).

- تشمل المخاطر الاجتماعية تلك التي تستند إلى علاقة الشركة بالمجتمع مع اهتمام خاص بأولئك الذين لديهم علاقة أكثر مباشرة: الموظفون، المساهمون، العملاء، الموردون، أو المجتمعات المحلية التي تولد فيها نشاطها (أولا، 2010). قد تشمل هذه المخاطر دعاوى قانونية محتملة، غرامات، أو عقوبات بسبب قضايا مع الموظفين، المساهمين، المجتمعات، الحكومة، إلخ، مما يعني تأثيرًا كبيرًا على المحركات المالية للشركات التي يجب أن يتم التعرف عليها وأخذها بعين الاعتبار من قبل المستثمرين.

3 تصنيف معايير ESG

3.1 المعايير البيئية

3.1.1 المخاطر الفيزيائية

3.1.2 مخاطر الانتقال

3.1.3 المخاطر الجيوسياسية والتنظيمية والقانونية

3.1.4 المخاطر التكنولوجية

3.1.5 مخاطر السوق

3.1.6 مخاطر السمعة

النموذج الذي يمكن تعريفه في التقييم، فضلاً عن الملف الاقتصادي المالي للنماذج الخبيرة. يمكن أن يكون مثالاً على ذلك فضيحة “فولكس فاجن” لتلاعبها بانبعاثات محركات الديزل الخاصة بها أو الشركات التي قامت بتصريفات في مناطق ذات قيمة بيئية خاصة.

3.2 المعايير الاجتماعية

- المزايا التنافسية (أو عدمها) للشركات فيما يتعلق بهذه المعايير الاجتماعية.

- إذا كانت الشركة تتبع هذه المعايير الاجتماعية، فهذا لأن إدارتها مناسبة وتؤدي إجراءاتها بشكل صحيح وفقًا لهذه المعايير الاجتماعية.

- بمجرد أن تتجسد المخاطر، يمكن أن تؤثر على النسب المالية المحددة للشركة وبالتالي على تدفقاتها النقدية مقابل الملاءة المالية.

3.3 معايير الحوكمة

- أن تكون هناك سياسة CSR (المسؤولية الاجتماعية للشركات) تشمل المبادئ أو الالتزامات التي تتعهد بها الشركة طواعية مع مختلف أصحاب المصلحة، وأن تحدد، على الأقل، أهداف تلك السياسة، والاستراتيجية المؤسسية من حيث الاستدامة، والبيئة، والقضايا الاجتماعية وآليات مراقبة المخاطر غير المالية، والأخلاقيات وسلوك الأعمال، من بين أمور أخرى.

- أن تقوم الشركة بالإبلاغ، في وثيقة منفصلة أو في التقرير الإداري، عن الأمور المتعلقة بالمسؤولية الاجتماعية للشركات، باستخدام واحدة من المنهجيات المعترف بها دوليًا.

- هذه المعايير الحوكمة هي مخاطر الشركة التي، بمجرد أن تتحقق، يمكن أن تؤثر على النسب المالية المحددة للشركة وبالتالي على جودتها الائتمانية.

3.4 أهمية معايير ESG

للهدف المالي، ولكن مع معايير الأثر الاجتماعي حيث تعتبر مقاييس ESG أساسية. أخيرًا، قبل الوصول إلى استثمار يركز فقط على العائد المالي، لدينا استثمار مستدام ومسؤول حيث يتم السعي لتحقيق الربحية المالية، ولكن مع تركيز على المدى الطويل، حيث تخدم معايير ESG لتخفيف المخاطر والبحث عن الفرص التي قد توجد. تبدو هذه الأساليب في تنوعاتها المختلفة كالاتجاه الحالي للمستثمرين، الذين بدأوا في ترك جانبًا المستثمرين الذين يركزون فقط على الاستثمار المالي دون أخذ معايير ESG في الاعتبار.

- من الصعب تخصيص قيمة نقدية لقضايا ESG ودمجها في النماذج المالية التنبؤية.

- قد يكون الكشف عن المعلومات المتعلقة بـ ESG من قبل الشركات محدودًا وغير موثوق وغير موحد.

- تميل قضايا ESG إلى التأثير على الأداء المالي على المدى الطويل، بينما العديد من المستثمرين، كما تم الإشارة إليه أعلاه، لديهم آفاق زمنية قصيرة نسبيًا.

وتحول إيجابي في القطاع المالي. هذه البنوك تتخذ خطوات استباقية لتنسيق عملياتها مع الأهداف العالمية للاستدامة، معترفة بالحاجة الملحة لمعالجة الاعتبارات البيئية والاجتماعية في أنشطة الإقراض والاستثمار. من خلال تنفيذ أنظمة إدارة ESRA، تهدف إلى تقييم وتخفيف المخاطر البيئية والاجتماعية المحتملة المرتبطة بمحافظها، مما يعزز التنمية المستدامة وممارسات المصرفية المسؤولة. هذا الانتقال لا يبرز فقط الأهمية المتزايدة لعوامل ESG في صناعة المالية، بل يعكس أيضًا التزامًا بمشهد مالي أكثر استدامة وعدلاً ووعيًا بيئيًا.

4 تنظيمات تقارير ESG وغير المالية

(ب) التكيف مع تغير المناخ.

(ج) الاستخدام المستدام وحماية الموارد المائية والبحرية.

(د) الانتقال إلى اقتصاد دائري.

(هـ) منع التلوث والسيطرة عليه.

(و) حماية واستعادة التنوع البيولوجي والأنظمة البيئية.

المستثمرون، الحوكمة، الأسواق

المادية البيئية والاجتماعية

المستهلكون، المجتمع المدني، الموظفون، المستثمرون

توصيات TCFD

توجيه الإبلاغ غير المالي

الرسم البياني 8

العلاقة بين تصنيفات الائتمان والتصنيفات الخضراء

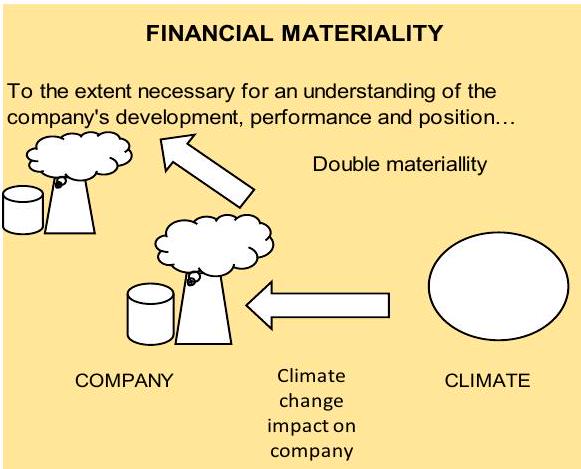

هم، والمعلومات اللازمة لفهم الأثر الذي يحدثونه على الناس والبيئة (الأشكال 7، 8).

مغطاة من قبل كل من التصنيف وتوجيهات الإبلاغ. في NFRD، على التوالي، تقع CCRs تحت بُعد “البيئة”. إلى أي مدى يمكن استخراج معلومات CCR بشكل منفصل عن تقرير الشركة سيعتمد على معايير الإبلاغ عن الاستدامة الأوروبية التي يتم تطويرها حاليًا.

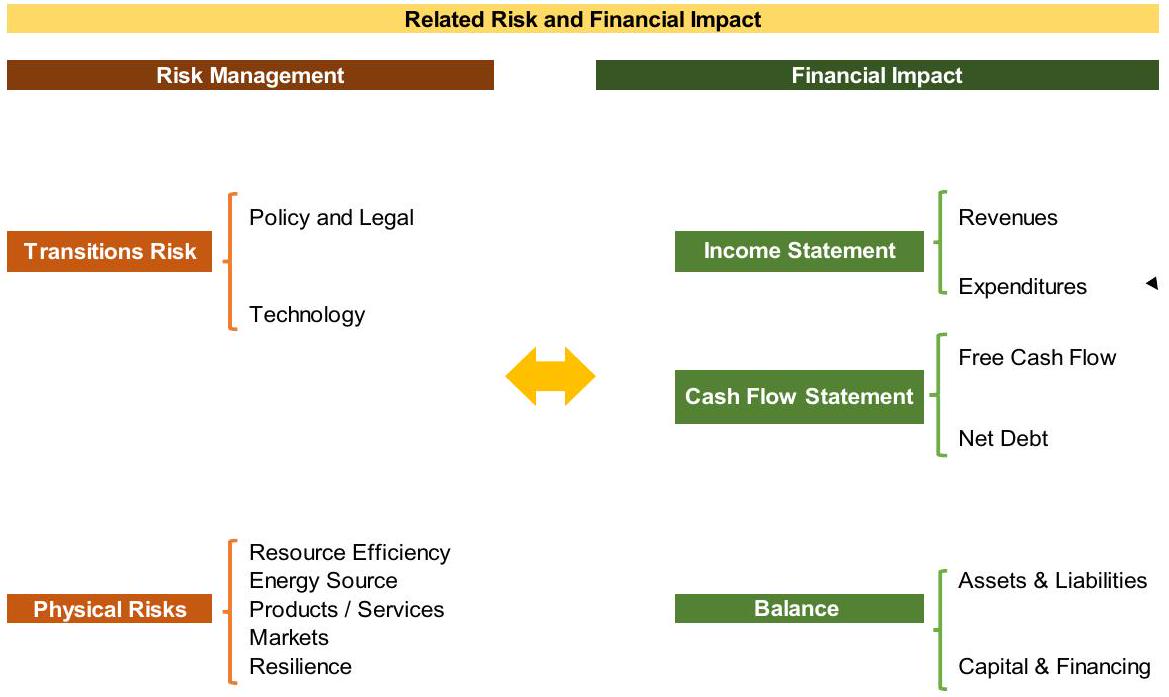

- السياسة والقانون: التأثير المالي لتسعير الكربون، التزامات الإبلاغ، تنظيم المنتجات والخدمات الحالية، التعرض للتقاضي.

- التكنولوجيا: التأثير المالي لاستبدال المنتجات والخدمات الحالية بخيارات منخفضة الانبعاثات، الاستثمار الفاشل في تقنيات جديدة

- السوق: التأثير المالي لتغير سلوك العملاء، عدم اليقين في إشارات السوق، ارتفاع تكلفة المواد الخام

- السمعة: التأثير المالي لتغير تفضيلات المستهلكين، زيادة قلق أصحاب المصلحة/التعليقات السلبية، وصمة عار على القطاع.

- كفاءة الموارد: استخدام وسائل النقل، عمليات الإنتاج والتوزيع الأكثر كفاءة، استخدام إعادة التدوير، الانتقال إلى مبانٍ أكثر كفاءة، تقليل استخدام واستهلاك المياه.

- مصدر الطاقة: استخدام مصادر الطاقة منخفضة الانبعاثات، استخدام الحوافز السياسية الداعمة، استخدام تقنيات جديدة.

- المنتجات والخدمات: تطوير و/أو توسيع السلع والخدمات منخفضة الانبعاثات، تطوير حلول التكيف مع المناخ، تطوير منتجات أو خدمات جديدة من خلال

والابتكار. - الأسواق: الوصول إلى أسواق جديدة، استخدام حوافز القطاع العام.

| المخاطر الفيزيائية | المخاطر غير الفيزيائية | الفرص | |||||

| شديدة | طويلة الأمد | السياسة/القانون/التقاضي | التكنولوجيا | السوق/الاقتصاد | السمعة | المالية | |

| الوصف | الأثر الفيزيائي للأحداث الجوية الأكثر شدة على الاستثمارات | الأثر الفيزيائي للأحداث الكارثية الأكثر تكرارًا | جميع الأهداف والتفويضات والتشريعات واللوائح على المستويات الدولية والوطنية ودون الوطنية التي تهدف إلى معالجة تغير المناخ، والتي تشمل المخاطر المحتملة المرتبطة بالتحولات المدفوعة بالسياسة نحو اقتصاد منخفض الكربون | سرعة التقدم التكنولوجي والاستثمارات لدعم اقتصاد منخفض الكربون أو تقليل انبعاثات الكربون (مخاطر الانتقال) | التغيرات في العرض أو الطلب أو الديناميات التنافسية، وإعادة تقييم الأصول المالية الكثيفة الكربون، وسرعة هذه إعادة التقييم. | الأذى للسمعة المالية أو غير المالية نتيجة ارتباط مباشر أو غير مباشر بأصل أو شركة. | المزايا الاقتصادية للشركات والمستثمرين والاقتصادات الناتجة عن التحولات المدفوعة بالسياسة والسوق والتكنولوجيا نحو اقتصاد أكثر استدامة ومنخفض الكربون، والتي تشمل استراتيجيات التكيف مع المناخ والتخفيف. |

| الأثر المالي | الاضطرابات في العمليات التشغيلية، والنقل، وسلاسل الإمداد، وشبكات التوزيع، وما إلى ذلك، بالإضافة إلى الأضرار التي تلحق بالأصول الفيزيائية | يمكن أن تؤثر التدهورات أو القيود على توفر الموارد على الشركات والاستثمارات التي تعتمد على هذه الموارد | يمكن أن تؤثر التكاليف المتعلقة بالامتثال، والالتزامات، والقيود على استخدام الأصول الكثيفة الكربون، والاستثمارات في تقنيات جديدة، والأصول المتعثرة، واهتزاز الأصول على قيمة الأصول التشغيلية والاستثمارات. | إلغاء استثمارات في تقنيات قائمة، والاستثمارات الضرورية في تقنيات جديدة، والتعديلات التشغيلية والعملية لاستيعاب هذه التقنيات الجديدة يمكن أن تؤثر على قيمة الأصول التشغيلية والاستثمارات | استدامة نماذج الأعمال المحددة، وتقييمات الشركات أو الأوراق المالية، واهتزاز الأصول يمكن أن تؤثر على قيمة الأصول التشغيلية والاستثمارات | الأذى لسمعة العلامة التجارية، وفقدان الإيرادات، وتكاليف إضافية | زيادة كفاءة الموارد الطبيعية، وتحسين الفعالية التشغيلية، وتوفير التكاليف، واكتشاف مصادر إيرادات جديدة، وزيادة الطلب على منتجات جديدة، وزيادة السيولة في السوق من خلال تحسين التسعير والشفافية، وتسريع الابتكار التكنولوجي، وتقليل اهتزاز الأصول بسبب زيادة الاستثمار في البنية التحتية المقاومة للمناخ |

- المرونة: المشاركة في برامج الطاقة المتجددة واعتماد تدابير كفاءة الطاقة، واستبدال/تنويع الموارد.

- وصف موجز لنموذج أعمال المجموعة، بما في ذلك بيئة أعمالها، وتنظيمها وهيكلها، والأسواق التي تعمل فيها، وأهدافها واستراتيجياتها، والعوامل الرئيسية والاتجاهات التي قد تؤثر على تطورها المستقبلي.

- وصف للسياسات التي تطبقها المجموعة فيما يتعلق بهذه الأمور، بما في ذلك إجراءات العناية الواجبة المطبقة لتحديد وتقييم،

الوقاية، والتخفيف من المخاطر والأثر الكبيرين والتحقق والرقابة، بما في ذلك ما تم اتخاذه من تدابير. - نتائج تلك السياسات، بما في ذلك مؤشرات الأداء الرئيسية غير المالية ذات الصلة لمراقبة وتقييم التقدم وتعزيز القابلية للمقارنة بين الشركات والقطاعات، وفقًا للأطر المرجعية الوطنية أو الأوروبية أو الدولية المستخدمة لكل موضوع.

- المخاطر الرئيسية المرتبطة بتلك القضايا المرتبطة بأنشطة المجموعة، بما في ذلك، حيثما كان ذلك مناسبًا ونسبياً، علاقاتها التجارية، والمنتجات أو الخدمات التي قد يكون لها آثار سلبية في تلك المجالات، وكيفية إدارة المجموعة لتلك المخاطر، موضحة الإجراءات المستخدمة لتحديدها وتقييمها وفقًا للأطر الوطنية، الأوروبية أو الدولية المرجعية لكل موضوع. يجب تضمين معلومات حول الآثار التي تم تحديدها، مع تقديم تحليل لهذه، حول المخاطر الرئيسية على المدى القصير والمتوسط والطويل.

- مؤشرات الأداء الرئيسية غير المالية ذات الصلة بالنشاط التجاري، والتي تلبي معايير القابلية للمقارنة، والأهمية، والملاءمة، والموثوقية. لتسهيل مقارنة المعلومات، سواء عبر الزمن أو بين الكيانات، سيتم استخدام معايير لمؤشرات غير مالية رئيسية يمكن تطبيقها بشكل عام وتلتزم بإرشادات المفوضية الأوروبية في هذا الشأن ومعايير المبادرة العالمية للإبلاغ، ويجب ذكر الإطار الوطني في التقرير، الأوروبي أو الدولي المستخدم لكل موضوع. يجب أن تنطبق مؤشرات الأداء غير المالية الرئيسية على كل من أقسام بيان التقرير غير المالي. يجب أن تكون هذه المؤشرات مفيدة، مع مراعاة الظروف المحددة ومتسقة مع المعايير المستخدمة في إجراءات إدارة المخاطر والتقييم الداخلية الخاصة بها. في أي حال، يجب أن تكون المعلومات المقدمة دقيقة وقابلة للمقارنة وقابلة للتحقق.

- معلومات مفصلة عن الآثار الحالية والمتوقعة لأنشطة المؤسسة على البيئة، وعند الاقتضاء، الصحة والسلامة، وإجراءات التقييم أو الشهادات البيئية؛ الموارد المخصصة للوقاية من المخاطر البيئية؛ تطبيق مبدأ الحيطة، وعدد الأحكام والضمانات للمخاطر البيئية.

- التلوث: تدابير لمنع أو تقليل أو إصلاح انبعاثات الكربون التي تؤثر بشكل خطير على البيئة؛ مع الأخذ في الاعتبار أي شكل من أشكال تلوث الهواء المحدد لنشاط معين، بما في ذلك تلوث الضوضاء والضوء.

- الاقتصاد الدائري والوقاية من النفايات وإدارتها: تدابير للوقاية، وإعادة التدوير، وإعادة الاستخدام، وأشكال أخرى من استرداد النفايات والتخلص منها؛ إجراءات لمكافحة هدر الطعام.

- الاستخدام المستدام للموارد: استهلاك المياه وإمدادات المياه وفقًا للقيود المحلية؛ استهلاك المواد الخام والتدابير المتخذة لتحسين كفاءة استخدامها؛ استهلاك الطاقة المباشر وغير المباشر، والتدابير المتخذة لتحسين كفاءة الطاقة واستخدام الطاقات المتجددة.

- تغير المناخ: العناصر الهامة لانبعاثات غازات الدفيئة الناتجة عن أنشطة الشركة، بما في ذلك استخدام السلع والخدمات التي تنتجها؛ التدابير المتخذة للتكيف مع عواقب تغير المناخ؛ الأهداف التخفيضية التي تم تحديدها طوعًا على المدى المتوسط والطويل لتقليل انبعاثات غازات الدفيئة والوسائل المنفذة لهذا الغرض.

- حماية التنوع البيولوجي: التدابير المتخذة للحفاظ على التنوع البيولوجي أو استعادته؛ الآثار الناتجة عن الأنشطة أو العمليات في المناطق المحمية.

5 اعتبار عوامل ESG من قبل وكالات التصنيف الائتماني./عوامل ESG ووكالات التصنيف الائتماني

تؤثر على الشركات. بشكل أساسي، تركز على المخاطر الفيزيائية ومخاطر الانتقال.

| موديز | S&P | فيتش | DBRS | |

| 1 | تلوث الهواء وتنظيم انبعاثات الكربون | انبعاثات غازات الدفيئة | انبعاثات غازات الدفيئة وجودة الهواء | انبعاثات الكربون وتأثير الاحتباس الحراري |

| 2 | تلوث الأرض – قيود على الاستخدام | التنوع البيولوجي، المياه واستخدام الأراضي | إدارة الطاقة | التنوع البيولوجي وتأثيره على التربة |

| 3 | تلوث المياه وندرة المياه | التلوث والنفايات | إدارة المياه ونفايات المياه | موارد وإدارة نفايات الصرف الصحي |

| 4 | المخاطر الطبيعية وتأثير الإنسان | الظروف الطبيعية (التعرض لظروف الطقس السلبية) | التعرض للتأثيرات البيئية | مخاطر المناخ |

6 الاستنتاجات

زيادة الشفافية، وقابلية التتبع، وتوحيد المعلومات المالية للشركات (غوبتا وآخرون، 2019).

لا يتم تحديد هذه العلاقة بوضوح. السبب الرئيسي هو نقص تجانس البيانات المبلغ عنها من قبل الشركات، فضلاً عن عدم توفر سلسلة تاريخية من بيانات الاستدامة بنطاق على الأقل مشابه لذلك الخاص بالمعلومات المالية.

إعلانات

الوصول المفتوح هذه المقالة مرخصة بموجب رخصة المشاع الإبداعي للاستخدام والمشاركة والتكيف والتوزيع وإعادة الإنتاج في أي وسيلة أو صيغة، طالما أنك تعطي الائتمان المناسب للمؤلفين الأصليين والمصدر، وتوفر رابطًا لرخصة المشاع الإبداعي، وتوضح ما إذا تم إجراء تغييرات. الصور أو المواد الأخرى من طرف ثالث في هذه المقالة مشمولة في رخصة المشاع الإبداعي للمقالة، ما لم يُذكر خلاف ذلك في سطر ائتمان للمادة. إذا لم تكن المادة مشمولة في رخصة المشاع الإبداعي للمقالة وكان استخدامك المقصود غير مسموح به بموجب اللوائح القانونية أو يتجاوز الاستخدام المسموح به، فستحتاج إلى الحصول على إذن مباشرة من صاحب حقوق الطبع والنشر. لعرض نسخة من هذه الرخصة، قم بزيارةhttp://creativecommons.org/licenses/by/4.0/.

References

Aula, P. (2010). Social media, reputation risk and ambient publicity management. Strategy & Leadership, 38(6), 43-49. https://doi.org/10.1108/10878571011088069

Aizebeokhai, A. P. (2009). Global warming and climate change: realities, uncertainties and measures. International Journal of Physical Sciences, 4(13), 868-879.

Benedetti, D., Biffis, E., Chatzimichalakis, F., Fedele, L. L., & Simm, I. (2021). Climate change investment risk: Optimal portfolio construction ahead of the transition to a lower-carbon economy. Annals of Operations Research, 299(1), 847-871.

Boffo, R., & Patalano, R. (2020). “ESG Investing: Practices, Progress and Challenges”, OECD Paris. https://www.oecd.org/finance/ESG-Investing-Practices-Progress-and-Challenges.pdf

Carbon Disclosure Project (CDP). (2020). The time to green finance diclosure insight action. CDP Financial Services. Disclosure Report 2020. https://www.cdp.net, https://cdn.cdp.net/cdp-production/cms/ reports/documents/000/005/741/original/CDP-Financial-Services-Disclosure-Report-2020.pdf? 1619537981

Charlo Molina, M. J., Moya Clemente, I., & Muñoz Rubio, A. M. (2013). Factores diferenciadores de las empresas del índice de responsabilidad español. Cuadernos De Gestión, 2(13), 15-37.

CNMV. (2014). Comision Nacional del Mercado de Valores. (Spanish Stocks Exchange Commision Authority). Good Governance of Listed (CGGLC) “Código de Buen Gobierno”.

Delmas, M., & Blass, V. (2010). Measuring corporate environmental performance: The trade-offs of sustainability ratings. Business Strategy and the Environment, 19(4), 245-260.

Diaz, D., & Moore, F. (2017). Quantifying the economic risks of climate change. Nature Climate Change, 7(11), 774-782.

Eccle, R., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11), 2835-2857. https://doi.org/10.1287/ mnsc. 2014.1984

Eccles, R.G., & Stroehle, J. (2018). Exploring social origins in the construction of ESG measures (2018). Available at SSRN: https://ssrn.com/abstract=3212685 or https://doi.org/10.2139/ssrn.3212685

European Commission. (2017). European commission on non-financial reporting – methodology for nonfinancial reporting – (2017/C 215/01)10, and the standards of the Global Reporting Initiative will be used. Available at https://eur-lex.europa.eu/legal-content/ES/TXT/PDF/?uri=CELEX:52017XC070 5(01)&from=En.

European Commission. (2019). Guidelines on reporting climate-related information. Available at: https:// ec.europa.eu/info/files/190618-climate-related-information-reporting-guidelines_en (europa.eu)

European Commission. (2020). Study on sustainability related ratings, data and research. Available at https://op.europa.eu/en/publication-detail/-/publication/d7d85036-509c-11eb-b59f-01aa75ed71a1

European Parliament and Council. (2022). Corporate sustainability reporting directive (Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU as regards sustainability reporting by companies (Text with EEA relevance). Available at https:// eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32022L2464

European Parliament and Council. (2014). Non-financial reporting directive (Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. Available at: https://eur-lex.europa.eu/eli/dir/2014/95/oj

European Stock Markets Authority. (2021). ESMA30-379-423. Retrieved from https://www.esma.europa. eu/sites/default/files/library/esma30-379-423_esma_letter_to_ec_on_esg_ratings.pdf

European Union (EU). (2019). European Green Deal. Available at https://ec.europa.eu/info/strategy/prior ities-2019-2024/european-green-deal_en

Ford, J. D., Berrang-Ford, L., & Paterson, J. (2011). A systematic review of observed climate change adaptation in developed nations. Climatic Change, 106(2), 327-336.

Gimeno, R. & Sols F. (2020). La incorporación de los factores de sostenibilidad en la gestión de carteras, nº39, p. 181-203. Revista de Estabilidad financiera Banco de España. Retrieved from: https://www. bde.es/f/webbde/GAP/Secciones/Publicaciones/InformesBoletinesRevistas/RevistaEstabilidadFi nanciera/20/Factores_sostenibilidad.pdf

Gupta, A., Boas, I., & Oosterveer, P. (2019). Transparency in global sustainability governance: To what effect? Journal of Environmental Policy & Planning, 22(1), 84-97.

Gupta, A., & Mason, M. (2016). Disclosing or obscuring? The politics of transparency in global climate governance. Current Opinion in Environmental Sustainability, 18, 82-90.

IPCC. (2007). Climate change 2007: Synthesis report. Contribution of Working Groups I, II and III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, Pachauri, R.K and Reisinger, A. (eds.)]. IPCC, Geneva, Switzerland, (p. 104).

IPCC. (2023). Climate change 2023: Synthesis report. Contribution of Working Groups I, II and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, H. Lee and J. Romero (eds.)]. IPCC, Geneva, Switzerland, pp. 35-115, doi: https://doi.org/ 10.59327/IPCC/AR6-9789291691647

Khan, M., Serafeim, G., & Yoon, A. (2016). Corporate sustainability: First evidence on materiality. The Accounting Review, 91(6), 1697-1724. https://doi.org/10.2308/accr-51383

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2000). Investor protection and corporate governance. Journal of Financial Economics, 58(1-2), 3-27.

Law 11/2018, of December 28, 2018 (Spanish Law) amending the Commercial Code, the revised Capital Companies Law approved by Legislative Royal Decree 1/2010, of July 2, 2010 and Audit Law 22/2015, of July 20, 2015, as regards non-financial information and diversity.

Maucieri, C., Barbera, A. C., Vymazal, J., & Borin, M. (2017). A review on the main affecting factors of greenhouse gases emission in constructed wetlands. Agricultural and Forest Meteorology, 236, 175-193.

Montzka, S. A., Dlugokencky, E. J., & Butler, J. H. (2011). Non-CO2 greenhouse gases and climate change. Nature, 476(7358), 43-50.

Organisation for Economic Co-operation and Development Social Impact Investment 2019 (2019). The impact imperative for sustainable development. Retrieved from https://www.oecd.org/development/ social-impact-investment-2019-9789264311299-en.htm

Philander, S. G. (2008). Encyclopedia of global warming and climate change:

Refinitiv. (2022). Environmental, social, and governance scores. Retrieved from Refinitiv. Retrieved from https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/refinitivesg-scores-methodology.pdf

Schuldt, J. P., Konrath, S. H., & Schwarz, N. (2011). “Global warming” or “climate change”? Whether the planet is warming depends on question wording. Public Opinion Quarterly, 75(1), 115-124.

Spain. (2006). Orden ECO/3722 de 26 de Diciembre. Código Conthe. Conthe Code updated in June 2013.

Taskforce on Nature-related Financial Disclosures. (2023). Final TNFD Recommendations on nature related issues published and corporates and financial institutions begin adopting. tnfd.global. Retrieved from: https://tnfd.global/final-tnfd-recommendations-on-nature-related-issues-published-andcorporates-and-financial-institutions-begin-adopting.

The European green deal elements. European Commission. (2020). https://commission.europa.eu/strat egy-and-policy/priorities-2019-2024/european-green-deal_en. European Union (EU)

Tucker, III., & Jones. (2020). Environmental, social, and governance investing: Investor demand, the great wealth transfer, and strategies for ESG investing. Journal of Financial Service Professionals, 74(3), 56-75.

UNFCC. (2015). United Nations framework convention on climate change. Report of the Conference of the Parties on its twenty-first session, held in Paris from 30 November to 13 December 2015 FCCC/ CP/2015/10/Add. 1 (Agenda 2030, Paris Treaty). Retrieved from https://unfccc.int/resource/docs/ 2015/cop21/eng/10.pdf

United Nations Framework Convention on Climate Change. (1992). Retrieved from: https://unfccc.int/ resource/docs/convkp/conveng.pdf

World Economic Forum. (2022). Global risks report 2022 the perspective of the dual materiality of the non-financial reporting directive in the context of climate-related reporting. Retrieved from https:// www3.weforum.org/docs/WEF_The_Global_Risks_Report_2022.pdf

المؤلفون والانتماءات

مونيكا أوليفر ييبينيس¹

مونيكا أوليفر ييبينيس

- معلومات المؤلف الموسعة متاحة في الصفحة الأخيرة من المقالة

توجيه التقارير غير المالية. البرلمان الأوروبي والمجلس. (2014). توجيه التقارير غير المالية (التوجيه 2014/95/EU للبرلمان الأوروبي والمجلس بتاريخ 22 أكتوبر 2014 المعدل للتوجيه 2013/34/EU فيما يتعلق بالإفصاح عن المعلومات غير المالية والتنوع من قبل بعض الشركات الكبرى والمجموعات. [رابط: (europa.eu)].

توجيه تقرير الاستدامة المؤسسية. البرلمان الأوروبي والمجلس. (2022). توجيه تقرير الاستدامة المؤسسية (التوجيه (الاتحاد الأوروبي) 2022/2464 للبرلمان الأوروبي والمجلس بتاريخ 14 ديسمبر 2022 المعدل لائحة (الاتحاد الأوروبي) رقم 537/2014، التوجيه 2004/109/EC، التوجيه 2006/43/EC والتوجيه 2013/34/EU فيما يتعلق بتقارير الاستدامة من قبل الشركات (نص ذو صلة بالمنطقة الاقتصادية الأوروبية). https://archive.ipcc.ch/home_languages_main_spanish.shtml.

https://unfccc.int/es/process-and-meetings/que-es-la-convencion-marco-de-las-naciones-unidas-sobre-el-cambio-climatico.

ثاني أكسيد الكربون (CO2)، الميثان (CH4)، المركبات الهالوجينية، الأوزون الطبقي، أكسيد النيتروجين. ناتج بشكل رئيسي عن حرق الوقود الأحفوري لتوليد الكهرباء، النقل، التدفئة، الصناعة والبناء. كما أنه ناتج عن الثروة الحيوانية، الزراعة (خاصة زراعة الأرز)، معالجة مياه الصرف الصحي والمكبات من بين أمور أخرى. هم الفاعلون الرئيسيون الذين يتأثرون بقرارات الشركة (العمال، المنظمات الاجتماعية، المساهمون، العملاء، الموردون، من بين آخرين). تقرير مؤتمر الأطراف في دورته الحادية والعشرين، الذي عقد في باريس من 30 نوفمبر إلى 13 ديسمبر 2015 FCCC/CP/2015/10/Add. 1 (جدول أعمال 2030، معاهدة باريس).

تقرير المخاطر العالمية 2022 | المنتدى الاقتصادي العالمي (2022)https://www.weforum.org. CNMV: اللجنة الوطنية لسوق القيم (لجنة البورصة الإسبانية). مبادئ الاستثمار المسؤول. تنظيم (الاتحاد الأوروبي) 2020/852، الذي نُشر رسميًا في يونيو 2020، يحتوي على أسس نظام التصنيف الأوروبي المشترك للأنشطة الاقتصادية المستدامة بيئيًا، مما يجعل من الممكن تحديد درجة استدامة الاستثمار. توجيه بشأن المعلومات المؤسسية في مجال الاستدامة، قرار تشريعي للبرلمان الأوروبي بتاريخ 10 نوفمبر 2022 بشأن اقتراح توجيه من البرلمان الأوروبي والمجلس بتعديل التوجيه 2013/34/EU، التوجيه 2004/109/EC، التوجيه 2006/43/EC واللائحة (الاتحاد الأوروبي) رقم 537/2014، فيما يتعلق بتقارير الاستدامة المؤسسية. المؤسسات الخارجية لتقييم الائتمان.

مؤشرات الأداء الرئيسية.

الهيئة الأوروبية للأوراق المالية والأسواق. https://www.bde.es/f/webbde/GAP/Secciones/Publicaciones/InformesBoletinesRevistas/RevistaEstabilidadFinanciera/20/Factores_sostenibilidad.pdf. ESA 2010 (2.45): قطاع “الشركات غير المالية” (S.11) يتكون من وحدات مؤسسية ذات شخصية قانونية وهي منتجون في السوق ونشاطها الرئيسي هو إنتاج السلع والخدمات غير المالية. يشمل قطاع الشركات غير المالية أيضًا الشركات شبه غير المالية.

DOI: https://doi.org/10.1007/s40822-023-00251-x

Publication Date: 2024-03-01

Climate change, ESG criteria and recent regulation: challenges and opportunities

Abstract

The application of environmental, social and governance (ESG) criteria has now become a more than essential requirement in the financial world. Therefore, it is necessary to understand, select and assess the risks of these ESG criteria and evaluate how they can impact a product or investment decision. Thus, the main objective of this article is to analyze ESG (Environmental, Social and Governance) indicators and their potential impacts in the framework of non-financial information. Current regulatory developments, such as the European Corporate Sustainability Reporting Directive (CSRD), are pushing to make ESG indicators (within this triple perspective: social, environmental and governance risks) a key set of information to be used for reporters and users of information. This article will study in further detail the main implications these regulations will have in how corporations will reflect social and ecological footprint information in their external reporting. Since these ESG indicators could have relevant financial impacts on the financial drivers of a corporation, stakeholders will be concerned on how enterprises are dealing with these ESG risks. Therefore, this ESG data will increase transparency and would mean a better understanding on how companies and investors have a sustainability compromise to evolve to a neutral carbon economy. In order to understand a company’s commitment with these ESG criteria, stakeholders would have to assess different aspects of the information reported. In this sense, this article will focus on how credit rating agencies incorporate these risks in their assessments. Credit rating agencies are becoming important actors in the sustainability criteria, as they incorporate ESG risks in their assessments, transmitting the importance of these indicators to investors and to markets. This study will look into the different time horizons between financial profitability and sustainability indicators. Current tendency and huge demand of non-financial indicators do not have the same profoundness, framework and tradition as financial indicators. This could lead to a situation in which it would be necessary a period to adapt both worlds and make them join and connect together in a sense in which one need the other one.

Abbreviations

| ESG | Environmental, social, and governance |

| ECAI | External credit assessment institutions |

| UNE | United Nations |

| CSR | Corporate social responsibility |

| CNMV | Comisión Nacional del Mercado de Valores |

| CG | Code of governance/ |

| GREY | Global reporting initiative |

| SASB | Sustainability accounting standard |

| TFCRFD | Task force on climate-related financial disclosures |

| CDP | Carbon disclosure project |

| E | Earnings |

| BV | Book value |

| R | Revenue |

| CF | Cash flow |

| D | Dividend |

| W | Weighted average |

| ROE | Return on equity |

| NFRD | Non-financial reporting directive |

| CSRD | Corporate sustainability reporting directive |

1 Introduction

2 Climate change, ESG and business risk

- Deforestation: thanks to photosynthesis, trees absorb

and return it to the atmosphere in the form of acting oxygen, as well as natural climate regulators. The uncontrolled clearing of rainforests is jeopardizing this beneficial effect. - Fossil fuel combustion: the combustion of coal, oil and gas produces carbon dioxide and nitrous oxide.

- Nitrogen fertilizers: these types of fertilizers are increasingly used in agriculture and produce large amounts of nitrous oxide.

- Livestock development: livestock is one of the main sources of methane emissions. In fact, the United Nations recommends reducing our meat consumption as one of the main recipes to fight climate change.

- Destruction of marine ecosystems: the oceans are also sinks for

generated. In addition to their destruction, the problem is when they reach their

- Population increases: the world’s population continues to grow and consume. A growing population increasingly demands more resources, which generates an increase in the emission of greenhouse gases.

- Environmental risks are those that relate the activity of the company and its impact, both direct and indirect, with the environment and they are currently being recognized as a component of climate change risk (Kedward et al., 2022). All business activity has environmental impacts. With greater or lesser economic impact, what is certain is that compliance with these environmental criteria is increasingly valued as efficiency, transparency, quality, and commitment of the company (Gupta et al., 2016).

- Social risks are those that are based on the relationship of the company with society with special care with those with whom they have a more direct relationship: employees, shareholders, customers, suppliers, or those local communities where they generate their activity (Aula, 2010). These risks may include potential lawsuits, fines, or penalties due to issues with employees, shareholders, communities, government, etc., which would mean a significant impact on financial drivers of corporations that should be identified and considered by investors.

3 Typology of ESG criteria

3.1 Environmental criteria

3.1.1 Physical risks

3.1.2 Transition risks

3.1.3 Geopolitical, regulatory and legal risks

3.1.4 Technological risks

3.1.5 Market risk

3.1.6 Reputational risk

model that can be defined in the assessment, as well as the economic-financial profile of the expert models. An example could be the “Volkswagen” scandal for the manipulation of the emissions of its diesel engines or companies that have made discharges in areas of special ecological value.

3.2 Social criteria

- Competitive benefits (or not) of companies in relation to these social criteria.

- If a company follows these social criteria, it is because its management is adequate and performs its actions correctly according to these social criteria.

- Once the risks materialize, they can affect the company’s specific financial ratios and therefore its cash flows versus financial solvency.

3.3 Governance criteria

- That there is a CSR (Corporate Social Responsibility) policy that includes the principles or commitments that the company voluntarily assumes with the different stakeholders, and that it identifies, at least, the objectives of that policy, the corporate strategy in terms of sustainability, environment and social issues and the mechanisms for monitoring non-financial risk, ethics and business conduct, among others.

- That the company report, in a separate document or in the management report, matters related to corporate social responsibility, using one of the internationally accepted methodologies.

- These governance criteria are company risks that, once they are realized, can have an impact on the company’s specific financial ratios and therefore its credit quality.

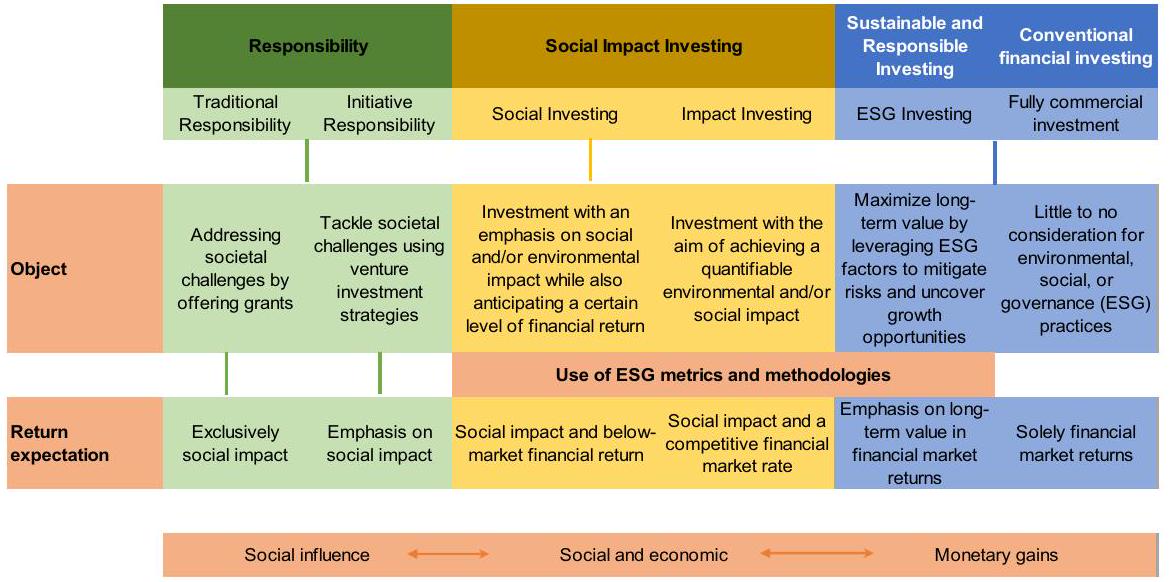

3.4 Importance of ESG criteria

of a financial objective, but with social impact criteria where the consideration of ESG metrics is fundamental. Finally, before reaching an investment solely focused on a financial return, we have sustainable and responsible investment where financial profitability is sought, but with a long-term focus, where ESG criteria serve to mitigate risks and look for opportunities that may be found. These methods in their different varieties seem to be the current trend of investors, beginning to leave aside investors purely focused on financial investment that do not have into consideration the ESG criteria.

- It is difficult to allocate a monetary value to ESG issues and integrate them into predictive financial models.

- Disclosure of ESG-related information by companies may be limited, unverified and non-standardized.

- ESG issues tend to influence long-term financial performance, while many investors, as suggested above, have relatively short-term horizons.

and positive shift in the financial sector. These banks are taking proactive steps to align their operations with global sustainability goals, recognizing the pressing need to address environmental and social considerations in their lending and investment activities. By implementing ESRA management systems, they aim to evaluate and mitigate potential environmental and social risks associated with their portfolios, thereby fostering sustainable development and responsible banking practices. This transition not only underscores the growing importance of ESG factors in the financial industry but also reflects a commitment to a more sustainable, equitable, and environmentally conscious financial landscape.

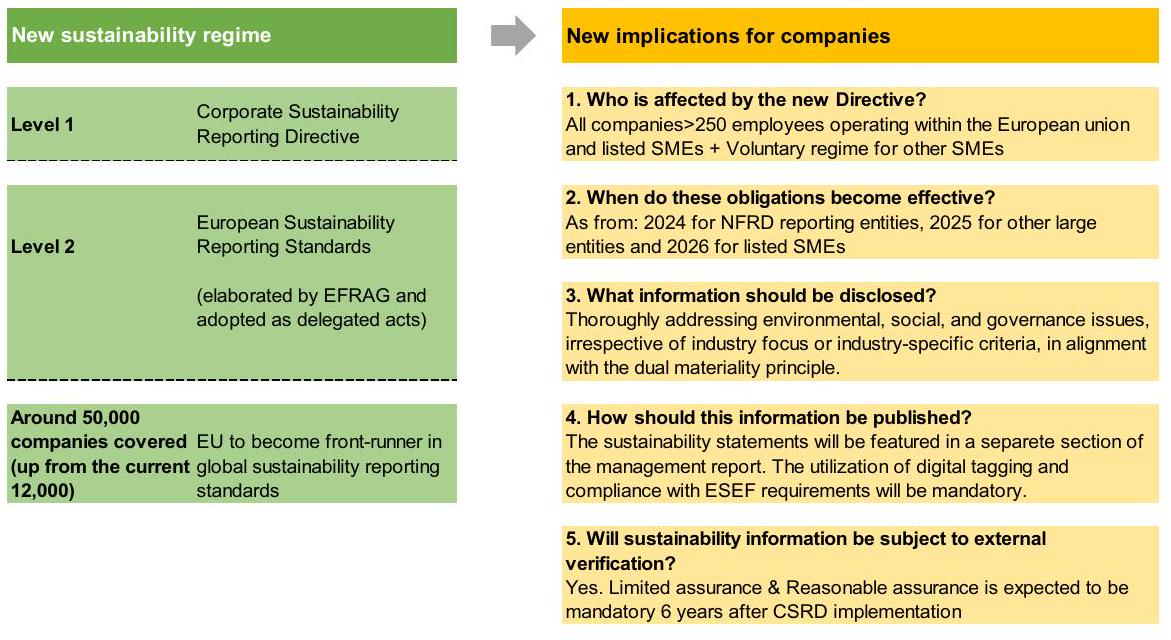

4 ESG and non-financial reporting regulations

(b) Adaptation to climate change.

(c) Sustainable use and protection of water and marine resources.

(d) The transition to a circular economy.

(e) Pollution prevention and control.

(f) The protection and restoration of biodiversity and ecosystems.

INVESTORS, GOBERNANCE, MARKETS

ENVIRONMENTAL & SOCIAL MATERIALITY

CONSUMERS, CIVIL SOCIETY, EMPLOYEES, INVESTORS

RECOMMENDATIONS OF THE TCFD

NON FINANCIAL REPORTING DIRECTIVE

Gráfico 8

CORRELACIÓN ENTRE RATINGS DE CRÉDITO Y RATINGS VERDES

them, and the information necessary to understand the impact they have on people and the environment (Figs. 7, 8).

covered by both the taxonomy and the reporting directives. In the NFRD, respectively, the CSRD, the CCRs fall under the “environment” dimension. To what extent CCR information can be extracted separately from the company report will depend on the European sustainability reporting standards currently being developed.

- Policy and legal: financial impact of carbon pricing, reporting obligations, regulations of existing products and services, exposure to litigation.

- Technology: financial impact of replacing existing products and services with lower emission options, failed investment in new technologies

- Market: financial impact of changing customer behaviors, uncertainty in market signals, rising cost of raw materials

- Reputation: financial impact of changing consumer preferences, increased stakeholder concern/negative comments, stigmatization of the sector.

- Resource efficiency: use of transport modes, more efficient production, and distribution processes, use of recycling, transfer to more efficient buildings, reduced use and consumption of water.

- Energy source: use of low-emission energy sources, use of supportive policy incentives, use of new technologies.

- Products and services: development and/or expansion of low-emission goods and services, development of climate adaptation solutions, development of new products or services through

and innovation. - Markets: access to new markets, use of public sector incentives.

| Physical Risk | Nonphysical Risk | Opportunities | |||||

| Severe | Long- lasting | Policy/Legal/Litigation | Technology | Market/Economic | Reputation | Financial | |

| Description | The physical impact of more intense weather events on investments | The physical impact of more frequent catastrophic events | All targets, mandates, legislation, and regulations at the international, national, and subnational levels aimed at addressing climate change, which encompass potential risks associated with policy-driven shifts toward a low-carbon economy | The pace of technological advancements and investments in support of a lowcarbon economy or the reduction of carbon emissions (transition risks) | Alterations in supply, demand, or competitive dynamics, the possible revaluation of carbon-intensive financial assets, and the rapidity of such revaluation. | Harm to one’s financial or nonfinancial reputation resulting from a direct or indirect connection to an asset or company. | The economic advantages for companies, investors, and economies resulting from policy, market, and technology-led shifts towards a more sustainable, lowcarbon economy, encompassing both climate adaptation and mitigation strategies. |

| Financial Impacts | Disruptions to operational processes, transportation, supply chains, distribution networks, etc., as well as damage to physical assets | The degradation or restrictions on the availability of resources can impact companies and investments that rely on these resources | Costs related to compliance, liabilities, limitations on the use of carbonintensive assets, investments in new technologies, stranded assets, and asset impairments can impact the value of operational assets and investments. | Write-offs of investmenst in existing tehcnologies, necessary investments in new technologies, operational and process modifications to accommodate these new technologies can influence the value of operational assets and investments | The sustainability of specific business models, company or securities valuations, and asset impairments can impact the value of operational assets and investments | Harm to brand reputation, revenue loss, and extra costs | Enhanced natural resource efficiency, improved operational effectiveness, cost savings, the discovery of new revenue sources, increased demand for new products, potentially better market liquidity through improved pricing and transparency, accelerated technological innovation, and reduced asset impairments due to increased investment in climate-resilient infrastructure |

- Resilience: participation in renewable energy programs and adoption of energy efficiency measures, substitution/diversification of resources.

- A brief description of the Group’s business model, including its business environment, organization and structure, the markets in which it operates, its objectives and strategies, and the main factors and trends that may affect its future development.

- A description of the policies applied by the group with respect to such matters, including the due diligence procedures applied for the identification, assessment,

prevention, and mitigation of significant risks and impacts and verification and control, including what measures have been taken. - The results of those policies, including relevant non-financial key performance indicators to monitor and evaluate progress and to promote comparability between companies and sectors, in accordance with the national, European, or international reference frameworks used for each subject.

- The main risks related to those issues linked to the group’s activities, including, where relevant and proportionate, its business relationships, products or services that may have negative effects in those areas, and how the group manages those risks, explaining the procedures used to identify and assess them in accordance with national frameworks, European or international reference for each subject. Information should be included on the impacts that have been identified, providing a breakdown of these, on the main risks in the short, medium, and long term.

- Non-financial key performance indicators that are relevant to the business activity, and that meet the criteria of comparability, materiality, relevance and reliability. To facilitate the comparison of information, both over time and between entities, standards of key non-financial indicators that can be generally applied and that comply with the guidelines of the European Commission in this matter and the standards of the Global Reporting Initiative will be used, and the national framework must be mentioned in the report, European or international used for each subject. The key non-financial performance indicators should apply to each of the sections of the non-financial reporting statement. These indicators should be useful, considering specific circumstances and consistent with the parameters used in their internal risk management and assessment procedures. In any case, the information submitted must be accurate, comparable, and verifiable.

- Detailed information on the current and foreseeable effects of the undertaking’s activities on the environment and, where applicable, health and safety, environmental assessment or certification procedures; resources dedicated to the prevention of environmental risks; the application of the precautionary principle, the number of provisions and guarantees for environmental risks.

- Pollution: measures to prevent, reduce or repair carbon emissions that seriously affect the environment; considering any form of air pollution specific to an activity, including noise and light pollution.

- Circular economy and waste prevention and management: measures for prevention, recycling, reuse, other forms of waste recovery and disposal; Actions to combat food waste.

- Sustainable use of resources: water consumption and water supply according to local constraints; consumption of raw materials and measures taken to improve the efficiency of their use; direct and indirect energy consumption, measures taken to improve energy efficiency and the use of renewable energies.

- Climate change: the significant elements of greenhouse gas emissions generated as a result of the company’s activities, including the use of the goods and services it produces; measures taken to adapt to the consequences of climate change; the reduction goals established voluntarily in the medium and long term to reduce greenhouse gas emissions and the means implemented for this purpose.

- Protection of biodiversity: measures taken to preserve or restore biodiversity; impacts caused by activities or operations in protected areas.

5 Consideration of ESG factors by credit rating agencies./ESG factors and credit rating agencies

can have an impact on companies. Fundamentally, they focus on physical risks and transition risks.

| MOODY’S | S&P | FITCH | DBRS | |

| 1 | Air pollution & carbon emissions regulations | Greenhouse gas emissions | Greenhouse gas emissions & air quality | Carbon emissions and greenhouse effect |

| 2 | Land pollution-restrictions on use | Biodiversity, water and land use | Energy management | Biodiversity and impact on soil |

| 3 | Water pollution water scarcity | Pollution and waste | Water and water waste management | Sewage waste resources and management |

| 4 | Natural hazards and human impact | Natural conditions (exposure to adverse weather conditions) | Exposure to environmental impacts | Climate risks |

6 Conclusions

greater transparency, traceability, and harmonization of financial information of companies (Gupta et al, 2019).

this relationship is not clearly identified. The main reason is the lack of homogenization of the data reported by companies, as well as the unavailability of a historical series of sustainability data with a scope at least similar to that of financial information.

Declarations

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/ licenses/by/4.0/.

References

Aula, P. (2010). Social media, reputation risk and ambient publicity management. Strategy & Leadership, 38(6), 43-49. https://doi.org/10.1108/10878571011088069

Aizebeokhai, A. P. (2009). Global warming and climate change: realities, uncertainties and measures. International Journal of Physical Sciences, 4(13), 868-879.

Benedetti, D., Biffis, E., Chatzimichalakis, F., Fedele, L. L., & Simm, I. (2021). Climate change investment risk: Optimal portfolio construction ahead of the transition to a lower-carbon economy. Annals of Operations Research, 299(1), 847-871.

Boffo, R., & Patalano, R. (2020). “ESG Investing: Practices, Progress and Challenges”, OECD Paris. https://www.oecd.org/finance/ESG-Investing-Practices-Progress-and-Challenges.pdf

Carbon Disclosure Project (CDP). (2020). The time to green finance diclosure insight action. CDP Financial Services. Disclosure Report 2020. https://www.cdp.net, https://cdn.cdp.net/cdp-production/cms/ reports/documents/000/005/741/original/CDP-Financial-Services-Disclosure-Report-2020.pdf? 1619537981

Charlo Molina, M. J., Moya Clemente, I., & Muñoz Rubio, A. M. (2013). Factores diferenciadores de las empresas del índice de responsabilidad español. Cuadernos De Gestión, 2(13), 15-37.

CNMV. (2014). Comision Nacional del Mercado de Valores. (Spanish Stocks Exchange Commision Authority). Good Governance of Listed (CGGLC) “Código de Buen Gobierno”.

Delmas, M., & Blass, V. (2010). Measuring corporate environmental performance: The trade-offs of sustainability ratings. Business Strategy and the Environment, 19(4), 245-260.

Diaz, D., & Moore, F. (2017). Quantifying the economic risks of climate change. Nature Climate Change, 7(11), 774-782.

Eccle, R., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11), 2835-2857. https://doi.org/10.1287/ mnsc. 2014.1984

Eccles, R.G., & Stroehle, J. (2018). Exploring social origins in the construction of ESG measures (2018). Available at SSRN: https://ssrn.com/abstract=3212685 or https://doi.org/10.2139/ssrn.3212685

European Commission. (2017). European commission on non-financial reporting – methodology for nonfinancial reporting – (2017/C 215/01)10, and the standards of the Global Reporting Initiative will be used. Available at https://eur-lex.europa.eu/legal-content/ES/TXT/PDF/?uri=CELEX:52017XC070 5(01)&from=En.

European Commission. (2019). Guidelines on reporting climate-related information. Available at: https:// ec.europa.eu/info/files/190618-climate-related-information-reporting-guidelines_en (europa.eu)

European Commission. (2020). Study on sustainability related ratings, data and research. Available at https://op.europa.eu/en/publication-detail/-/publication/d7d85036-509c-11eb-b59f-01aa75ed71a1

European Parliament and Council. (2022). Corporate sustainability reporting directive (Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU as regards sustainability reporting by companies (Text with EEA relevance). Available at https:// eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32022L2464

European Parliament and Council. (2014). Non-financial reporting directive (Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. Available at: https://eur-lex.europa.eu/eli/dir/2014/95/oj

European Stock Markets Authority. (2021). ESMA30-379-423. Retrieved from https://www.esma.europa. eu/sites/default/files/library/esma30-379-423_esma_letter_to_ec_on_esg_ratings.pdf

European Union (EU). (2019). European Green Deal. Available at https://ec.europa.eu/info/strategy/prior ities-2019-2024/european-green-deal_en

Ford, J. D., Berrang-Ford, L., & Paterson, J. (2011). A systematic review of observed climate change adaptation in developed nations. Climatic Change, 106(2), 327-336.

Gimeno, R. & Sols F. (2020). La incorporación de los factores de sostenibilidad en la gestión de carteras, nº39, p. 181-203. Revista de Estabilidad financiera Banco de España. Retrieved from: https://www. bde.es/f/webbde/GAP/Secciones/Publicaciones/InformesBoletinesRevistas/RevistaEstabilidadFi nanciera/20/Factores_sostenibilidad.pdf

Gupta, A., Boas, I., & Oosterveer, P. (2019). Transparency in global sustainability governance: To what effect? Journal of Environmental Policy & Planning, 22(1), 84-97.

Gupta, A., & Mason, M. (2016). Disclosing or obscuring? The politics of transparency in global climate governance. Current Opinion in Environmental Sustainability, 18, 82-90.

IPCC. (2007). Climate change 2007: Synthesis report. Contribution of Working Groups I, II and III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, Pachauri, R.K and Reisinger, A. (eds.)]. IPCC, Geneva, Switzerland, (p. 104).

IPCC. (2023). Climate change 2023: Synthesis report. Contribution of Working Groups I, II and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, H. Lee and J. Romero (eds.)]. IPCC, Geneva, Switzerland, pp. 35-115, doi: https://doi.org/ 10.59327/IPCC/AR6-9789291691647

Khan, M., Serafeim, G., & Yoon, A. (2016). Corporate sustainability: First evidence on materiality. The Accounting Review, 91(6), 1697-1724. https://doi.org/10.2308/accr-51383

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2000). Investor protection and corporate governance. Journal of Financial Economics, 58(1-2), 3-27.

Law 11/2018, of December 28, 2018 (Spanish Law) amending the Commercial Code, the revised Capital Companies Law approved by Legislative Royal Decree 1/2010, of July 2, 2010 and Audit Law 22/2015, of July 20, 2015, as regards non-financial information and diversity.

Maucieri, C., Barbera, A. C., Vymazal, J., & Borin, M. (2017). A review on the main affecting factors of greenhouse gases emission in constructed wetlands. Agricultural and Forest Meteorology, 236, 175-193.

Montzka, S. A., Dlugokencky, E. J., & Butler, J. H. (2011). Non-CO2 greenhouse gases and climate change. Nature, 476(7358), 43-50.

Organisation for Economic Co-operation and Development Social Impact Investment 2019 (2019). The impact imperative for sustainable development. Retrieved from https://www.oecd.org/development/ social-impact-investment-2019-9789264311299-en.htm

Philander, S. G. (2008). Encyclopedia of global warming and climate change:

Refinitiv. (2022). Environmental, social, and governance scores. Retrieved from Refinitiv. Retrieved from https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/refinitivesg-scores-methodology.pdf

Schuldt, J. P., Konrath, S. H., & Schwarz, N. (2011). “Global warming” or “climate change”? Whether the planet is warming depends on question wording. Public Opinion Quarterly, 75(1), 115-124.

Spain. (2006). Orden ECO/3722 de 26 de Diciembre. Código Conthe. Conthe Code updated in June 2013.

Taskforce on Nature-related Financial Disclosures. (2023). Final TNFD Recommendations on nature related issues published and corporates and financial institutions begin adopting. tnfd.global. Retrieved from: https://tnfd.global/final-tnfd-recommendations-on-nature-related-issues-published-andcorporates-and-financial-institutions-begin-adopting.

The European green deal elements. European Commission. (2020). https://commission.europa.eu/strat egy-and-policy/priorities-2019-2024/european-green-deal_en. European Union (EU)

Tucker, III., & Jones. (2020). Environmental, social, and governance investing: Investor demand, the great wealth transfer, and strategies for ESG investing. Journal of Financial Service Professionals, 74(3), 56-75.

UNFCC. (2015). United Nations framework convention on climate change. Report of the Conference of the Parties on its twenty-first session, held in Paris from 30 November to 13 December 2015 FCCC/ CP/2015/10/Add. 1 (Agenda 2030, Paris Treaty). Retrieved from https://unfccc.int/resource/docs/ 2015/cop21/eng/10.pdf

United Nations Framework Convention on Climate Change. (1992). Retrieved from: https://unfccc.int/ resource/docs/convkp/conveng.pdf

World Economic Forum. (2022). Global risks report 2022 the perspective of the dual materiality of the non-financial reporting directive in the context of climate-related reporting. Retrieved from https:// www3.weforum.org/docs/WEF_The_Global_Risks_Report_2022.pdf

Authors and Affiliations

Mónica Oliver Yébenes¹

Mónica Oliver Yébenes

- Extended author information available on the last page of the article

Non Financial Reporting Directive. European Parliament and Council. (2014). Non-Financial Reporting Directive (DIRECTIVE 2014/95/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. [URL: (europa.eu)].

Corporate Sustainability Reporting Directive. European Parliament and Council. (2022). Corporate Sustainability Reporting Directive (DIRECTIVE (EU) 2022/2464 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU as regards sustainability reporting by companies (Text with EEA relevance). https://archive.ipcc.ch/home_languages_main_spanish.shtml.

https://unfccc.int/es/process-and-meetings/que-es-la-convencion-marco-de-las-naciones-unidas-sobre-el-cambio-climatico.

Carbon dioxide (CO2), Methane (CH4), Halogenated compounds, Tropospheric ozone, Nitrogen oxide. Pmainly caused by the burning of fossil fuels for electricity generation, transport, heating, industry and building. Also caused by livestock, agriculture (mainly rice cultivation), wastewater treatment and landfills among others. They are the key actors that are affected by the decisions of a company (workers, social organizations, shareholders and, customers, suppliers, among many). Report of the Conference of the Parties on its twenty-first session, held in Paris from 30 November to 13 December 2015 FCCC/CP/2015/10/Add. 1 (Agenda 2030, Paris Treaty).

Global Risks Report 2022 | World Economic Forum (2022) https://www.weforum.org. CNMV: Comisión Nacional del Mercado de Valores (Spanish Stock Exchange Commission). Principles for Responsible Investment. Regulation (EU) 2020/852, officially published in June 2020, contains the foundations of the common European classification system of environmentally sustainable economic activities, which in turn makes it possible to determine the degree of sustainability of an investment. Directiva sobre información corporativa en materia de sostenibilidad, European Parliament legislative resolution of 10 November 2022 on the proposal for a Directive of the European Parliament and of the Council amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as regards corporate sustainability reporting. External Credit Assessment Institutions.

Key Performance Indicators.

European Securities and Market Authority. https://www.bde.es/f/webbde/GAP/Secciones/Publicaciones/InformesBoletinesRevistas/RevistaEst abilidadFinanciera/20/Factores_sostenibilidad.pdf. ESA 2010 (2.45): The “non-financial corporations” sector (S.11) is composed of institutional units with legal personality which are market producers and whose main activity is the production of goods and services not financial. The non-financial corporations sector also includes quasi-non-financial corporations.