المجلة: International Journal of Multicultural and Multireligious Understanding، المجلد: 11، العدد: 5 DOI: https://doi.org/10.18415/ijmmu.v11i5.5608 تاريخ النشر: 2024-05-08

دورة المال – الحد الأدنى من مدخرات الهروب والسيولة المالية

كونستانتينوس تشالوميسالجامعة الوطنية وكابوديستريان في أثينا، اليونان

تناقش هذه الورقة سرعات الحد الأدنى من المدخرات الهاربة والسيولة المالية. وهذا يعني أنها فحصت سلوك دورة المال في ظل الظروف العادية مع التحكم في سرعة الحد الأدنى من المدخرات الهاربة وسرعة السيولة المالية. لذلك، حددت كيف تعمل الاقتصاد بناءً على دورة المال الخاصة به. المدخرات الهاربة هي المدخرات التي تخرج من الاقتصاد. تعزز المدخرات الهاربة الحد الأدنى في نفس الوقت المدخرات الإلزامية، مما يؤدي بها إلى أقصى مستوى لها. المدخرات الإلزامية هي المدخرات التي تبقى في الاقتصاد. ومن ثم، من الممكن استخلاص استنتاجات حول الاستهلاك والاستثمارات في كل اقتصاد. لهذا التحليل تم استخدام نهج طريقة Q.E.

الكلمات الرئيسية: دورة المال؛ الحد الأدنى من المدخرات الهاربة؛ السيولة المالية

المقدمة

تدرس هذه الورقة سلوك دورة المال عند دمجها مع سرعة الحد الأدنى من المدخرات الهاربة وسرعة السيولة المالية (بيرغكويست وآخرون، 2020؛ كاي، 2017؛ كاموس وجيمبر، 2018؛ غولدشتاين وآخرون، 2020؛ هاي، 2016؛ سنو، 1988؛ سبيل وآخرون، 2018؛ وانغسنس وآخرون، 2020). تحدد العقود والاتفاقيات بين المشاركين في المعاملات الخاضعة للرقابة كيفية توزيع الأرباح والخسائر. يجب أن تذكر الاتفاقيات التغييرات في العقود (أكير ورابيلكي، 2010؛ العبيضي وآخرون، 2021؛ ألتمن، 2012؛ بهويان وفرازماند، 2020؛ غاردينو ومتلر، 2020؛ ميشنر وبراور، 2020؛ راسموسن وكالان، 2016؛ سوانستروم وآخرون، 2002؛ تاب، 2015). هذه هي السبب الذي يجعل السلطات الضريبية يجب أن تقوم بعمليات تفتيش دورية. إن تحديد العقود بشكل دوري مهم لتحليل القابلية للمقارنة (تشالوميس، 2018د، 2019ج، 2019أ، 2020ج، 2021ج، 2021ف، 2022هـ، 2022د، 2023أ، 2023ب، 2023ي، 2023ر، 2023م، 2023ي، 2024ب، 2024ف). تعتبر هذه التفتيشات الدورية للشركات المشاركة في المعاملات الخاضعة للرقابة حاسمة لمبدأ المسافة العادلة. يتم تحديد تقاسم التكاليف بعد ذلك من خلال إجراء فحوصات دورية على الأطراف المختبرة. علاوة على ذلك، يجب أن يتم الإخطار بأن الشركات المشاركة في المعاملات الخاضعة للرقابة وفي نفس الوقت يتم إجراء تفتيشات السلطات الضريبية تحت شرط التعديلات النسبية. تفسير شرط التعديلات النسبية هو أن الشركات التي تشارك في المعاملات الخاضعة للرقابة في كثير من الأحيان لا تمتلك البيانات المناسبة والمعاملات غير الخاضعة للرقابة في ظروف مماثلة للمقارنة وبالتالي تقوم بتعديل بياناتها بشكل نسبي (تشالوميس، 2019ز، 2020د، 2021هـ، 2021ب، 2021أ، 2023هـ، 2023ف، 2023أب، 2023هـ، 2024هـ، 2024د؛ كونستانتينوس تشالوميس، 2024). هذا يعني أنه إذا كانت

الشركات التي هي أطراف مختبرة تستنتج أن أرباح وخسائر الشركات من المعاملات غير الخاضعة للرقابة أعلى بكثير أو أقل بكثير، وبعد ذلك يقومون بعمل تشابه نسبي لمقارنتها ببياناتهم (أندريانسياه وآخرون، 2019؛ إيفانز وآخرون، 1999؛ غفليسياني، 2019؛ خادزيراديفا وآخرون، 2019؛ لاجاس وماكاريو، 2020؛ لابلاين ومازوكاتو، 2020؛ ميلجان، 2020؛ توريس سالسيدو وآخرون، 2015؛ ويليامسون ولوك، 2020). إنتاج السلع أو الخدمات يخلق أرباحًا وتكاليف للشركات:

الرمز يتعلق بعامل التأثير لتحليل القابلية للمقارنة والذي له أي طريقة إلى . الرمز z هو معامل يأخذ قيمًا بين 0 و 1 (تشالوميس، 2018هـ، 2018أ، 2019ب، 2022ج، 2023أد، 2023د، 2023ج، 2023ي، 2023أف، 2023ب، 2023أأ، 2023ج، 2023ن، 2024ج؛ كونستانتينوس تشالوميس، 2023). ما القيمة التي يمكن أن تُستقبل يتم تحديدها من خلال تأثير الطريقة (باستخدام قاعدة أفضل طريقة) على . الرمز لـ يتعلق بالتكلفة التي تنشأ من إنتاج السلع، والرمز لـ يتعلق بالتكلفة التي تنشأ من توزيع السلع.

وفقًا للمعادلة (1) إلى (6) من الممكن تحديد المعادلات التالية:

الرمز لـ في المعادلة السابقة يتعلق بمقدار الضرائب التي يجب دفعها للشركات المشاركة في المعاملات الخاضعة للرقابة في تطبيق مبدأ المسافة العادلة (تشالوميس، 2018ج، 2018ب، 2019د، 2020ب، 2021ي، 2021هـ، 2021ك، 2022ب، 2023أ، 2023ي، 2023ز، 2023أه، 2023و، 2024ج). الرمز هو مقدار الالتزامات الضريبية التي يمكن تجنبها من خلال تخصيص الأرباح والخسائر (AICPA، 2017؛ باككي وبيرناور، 2018؛ ديالو وآخرون، 2021؛ إريكسون، 2016؛ غروف وآخرون، 2020؛ سانشيز وآخرون، 2020؛ شرام، 2018؛ شوارتز، 2019؛ فيكترا وآخرون، 2020). علاوة على ذلك، هو معامل لمعدل الضرائب. ثم، توضح المعادلة (4) حالة مبدأ المسافة العادلة:

الرمز لـ في المعادلة السابقة يظهر الضرائب التي يجب دفعها للمؤسسات المشاركة في المعاملات الخاضعة للرقابة في تطبيق مبدأ الطول الثابت. ثم، هو معامل لمعدل الضرائب في حالة مبدأ الطول الثابت:

الضريبة على الشركات التي تشارك في المعاملات الخاضعة للرقابة لتسعير التحويل في حالة مبدأ الطول الثابت أعلى أو على الأقل تساوي تلك في حالة مبدأ المسافة العادلة. وبالتالي، مع مبدأ الطول الثابت يمكن للشركات المشاركة في المعاملات الخاضعة للرقابة التعامل مع القضايا التي تنشأ من تخصيص الأرباح والخسائر (أندرسون وآخرون، 2020؛ بينتو، 2009؛ إيوارت وآخرون، 2021؛ هاوسمان وآخرون، 2016؛ جونستون وبالارد، 2016؛ لويازا وبينينغز، 2020؛ مينغوي، 2020؛ مولر، 2020؛ نايك، 2019). لذلك، يمكن للسلطات الضريبية مواجهة آثار تسعير التحويل على الإيرادات الضريبية العالمية. يسمح مبدأ الطول الثابت باسترداد خسائر الضرائب من الإيرادات الضريبية العالمية من المعاملات الخاضعة للرقابة لتسعير التحويل (عبدالكافي، 2018؛ دومينغيز وبيكوريلي-بيري، 2013؛ هولكومب، 1998؛ هاوليت، 2020؛ كانانين، 2012؛ كيكينكو، 2020؛ ماكسويل، 2020؛ منظمة التعاون والتنمية الاقتصادية، 2020؛ ستون،

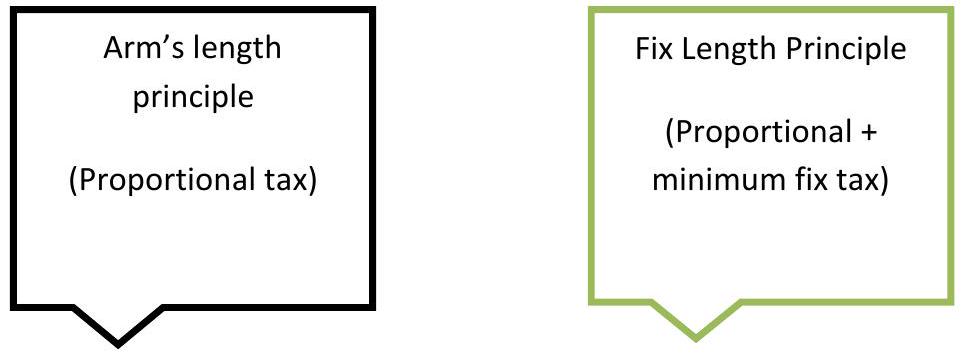

2008). يوضح المخطط التالي الإجراء الذي تتبعه الشركات المشاركة في المعاملات الخاضعة للرقابة لتخصيص أرباحها وخسائرها، التعديلات النسبية للبيانات، ومبدأ الطول الثابت:

الشكل 1: مبدأ المسافة العادلة لمبدأ الطول الثابت

يحدد الشكل 1 إجراء مبدأ الطول الثابت وتحليله الكمي لتحديد سلوك النموذج. يقدم القسم التالي نظرية دورة المال. المنهجية المطبقة هي طريقة Q.E. ونهجها الاقتصاد القياسي.

المنهجية

تتوافق الإيرادات الضريبية مع المدخرات التي كان يمكن أن تمتلكها الشركات إذا تم تجنب الضرائب. الطريقة التي يتم بها إدارة هذه المدخرات تختلف من حالة إلى أخرى. ثم يمكن إدارة فوائد الشركات بطريقة مختلفة تمامًا، كما يمكن أن يتم توفيرها أو فرض ضرائب عليها. تظهر نظرية دورة المال متى تعزز المدخرات الاقتصاد ومتى تعزز الضرائب الاقتصاد. يجب أن يكون هذا التحديد فصل المدخرات إلى المدخرات غير العائدة (أو المدخرات الهاربة) والمدخرات العائدة (أو المدخرات الإلزامية:

المتغير لـ يرمز إلى حالة المدخرات الهاربة. وهذا يعني أن هناك مدخرات لا تعود إلى الاقتصاد أو تعود بعد فترة طويلة. المتغير لـ يرمز إلى الحالة التي توجد فيها مدخرات هاربة تأتي من أنشطة تسعير التحويل. المتغير لـ يرمز إلى الحالة التي توجد فيها مدخرات هاربة ليست من أنشطة تسعير التحويل ولكن من أي نشاط تجاري آخر. على سبيل المثال، يمكن أن تشير إلى الأنشطة التجارية التي تأتي من

المعاملات غير الخاضعة للرقابة. المتغير لـ يرمز إلى السيولة المالية في الاقتصاد. المتغير لـ يرمز إلى الاستهلاك في الاقتصاد. المتغير لـ يرمز إلى المدخرات الإلزامية، التي تأتي من المواطنين والشركات الصغيرة والمتوسطة. المتغير لـ يرمز إلى حالة السيولة المالية في الاقتصاد. المتغير لـ يرمز إلى سرعة زيادة أو انخفاض السيولة المالية. المتغير لـ يرمز إلى سرعة المدخرات الهاربة. لذلك، المتغير لـ يرمز إلى مصطلح دورة المال (تشالوميس، 2019f، 2019e، 2021d، 2023o، 2023k، 2023q، 2023v، 2023s، 2023ah، 2023ag، 2024a).

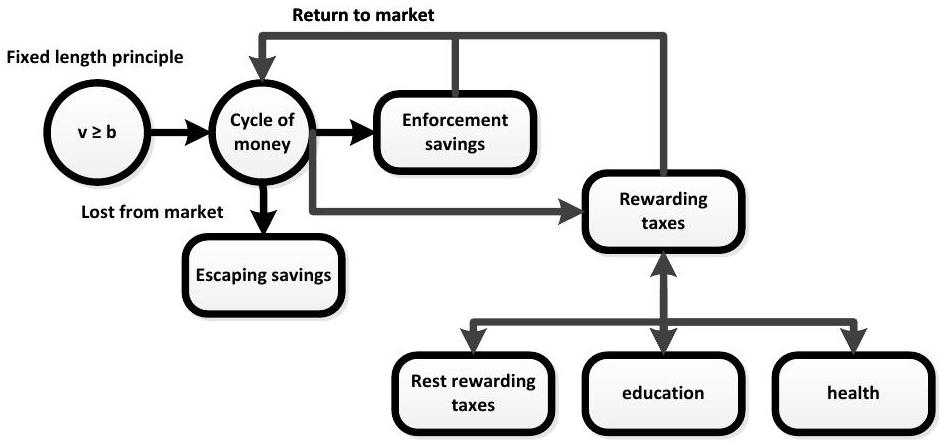

وبالتالي، تُظهر دورة المال مستوى ديناميكية الاقتصاد وقوته. لذلك، تم الحصول على أن دورة المال تنمو عندما يكون هناك نظام ضريبي مثل حالة مبدأ الطول الثابت الذي يسمح بضرائب منخفضة على المعاملات غير الخاضعة للرقابة وضرائب أعلى على المعاملات الخاضعة للرقابة (بارتلس، 2005؛ ديلغادو رودريغيز ودي لوكاس سانتوس، 2018؛ دينغ ولي، 2011؛ خان وليو، 2019؛ كونغاتس وآخرون، 2019؛ سلطانة وآخرون، 2020). يجب الإشارة إلى أنه كما تعتبر المعاملات غير الخاضعة للرقابة، يحدث نفس الشيء مع حالات السيولة المالية للمواطنين والشركات الصغيرة والمتوسطة. علاوة على ذلك، هناك ثلاثة عوامل تأثير أساسية للضرائب المجزية (تشالوميس، 2018f، 2020a، 2021g، 2021j، 2022a، 2023t، 2023l، 2023x). الضرائب المجزية هي الضرائب الوحيدة التي لها دور فوري ومهم في سوق أي اقتصاد. هذه العوامل مرتبطة بالتعليم، ونظام الصحة في كل مجتمع، وبقية العوامل الاقتصادية الهيكلية ذات الصلة بالعاملين السابقين.

الشكل 2: دورة المال مع الضرائب المجزية

يمثل المخطط السابق دورة المال بالإضافة إلى جميع عوامل الضرائب المجزية:

في المعادلتين السابقتين تم استخدام بعض عوامل التأثير، وهيالتي تم توضيحها أيضًا في المعادلة (14)، علاوة على ذلك المتغيراتو. المتغيريرمز إلى عامل التأثير لبقية الضرائب المجزية. رمزهو عامل التأثير للتعليم وأي معرفة تقنية (تشالوميس، 2019g؛ غرافس وآخرون، 2020؛ هاسلمان وستوكر، 2017؛ جومو ووي، 2003؛ كامراد-سكوت وماكنيس، 2012؛ مارومي، 2016؛ ميايله، 2017؛ ناش وآخرون، 2017؛ أوسلاتي، 2015؛ ريباسوسكيني وآخرون، 2019؛ ستراسهيم، 2019؛ سوسلوف وباساريفا، 2020). رمزيتعلق بعامل التأثير للصحة وأي شيء ذي صلة وداعم لهذه القضية. رمزوهما معامل الصحة وعامل التأثير الصحي وفقًا لذلك (أيتكن، 2019؛ آل-

باستخدام المعادلات (6) إلى (15) من الممكن الانتقال إلى المدخرات المختلطة. باستخدام المعادلات (1) إلى (15) من الممكن تحديد سلوك منفعة دورة المال. علاوة على ذلك، بما في ذلك المدخرات المختلطة :

في المعادلات السابقة، يمثلالذي يمثل المدخرات المختلطة. دور المدخرات المختلطة هو تمثيل أن المصانع، والبحث، ومراكز التنمية لديها مدخرات هاربة في نفس الوقت. الرموز المتبقية قد تم تعريفها بالفعل.

في المعادلات السابقة، ووهما القيم الأولية لسرعة المدخرات الهاربة ودورة المال. علاوة على ذلك، تمثل المعادلةالمعادلة العامة لمدخرات الهروب:

المعادلة (26) تتعلق بالشكل العام لسرعة دورة المال. معاملوأخذ اثنان منهما قيمة ثابتة واحدةوالأخرى صفر. يحدث نفس الشيء مع معاملاتالتي تأخذ أيضًا اثنان منهما قيمة ثابتة واحدةوالأخرى صفر. بهذه الطريقة، هناك جميع التركيبات الممكنة لسرعات المدخرات الهاربة والسيولة المالية التي يمكن تعريفها من خلال معادلتين محددتين.

جدول المعاملات لدورة المال هو كما يلي:

جدول: تجميع المعاملات

العوامل

القيم

0.6

0.7

0.9

0.8

تطبيق طريقة Q.E. مع المعاملات السابقة:

الشكل 3: دورة المال مع سرعاتها

المعادلة (29) تمثل سرعة المدخرات الهاربة في الشكل 3a. المعادلة (30) تمثل السيولة المالية في الشكل 2b. سرعة المدخرات الهاربة عندما تكون في أدنى مستوى لها، زادت السيولة المالية مما يوفر دورة مال أعلى. لذلك، تم تعزيز الاقتصاد.

الاستنتاجات

في هذه الورقة، تم الاستنتاج أنه في دورة المال عندما تكون المدخرات الهاربة محدودة، يكون للاقتصاد اتجاه إيجابي أقصى. هذا يعني أن الاستهلاك والاستثمارات ستزداد في أي اقتصاد، إلى أقصى حد. ولكن، تم تحديد أيضًا أن المدخرات الهاربة المحدودة تحول الشكل اللوغاريتمي لسرعة المدخرات الهاربة إلى شكل خطي.

References

Aakre, S., & Rübbelke, D. T. G. (2010). Objectives of public economic policy and the adaptation to climate change. Journal of Environmental Planning and Management, 53(6). https://doi.org/10.1080/09640568.2010.488116.

Abdelkafi, I. (2018). The Relationship Between Public Debt, Economic Growth, and Monetary Policy: Empirical Evidence from Tunisia. Journal of the Knowledge Economy, 9(4). https://doi.org/10.1007/s13132-016-0404-6.

AICPA. (2017). Guiding principles of good tax policy: A framework for evaluating tax proposals. American Institute of Certified Public Accountants, 2017(March 2001).

AL-UBAYDLI, O., LEE, M. S., LIST, J. A., MACKEVICIUS, C. L., & SUSKIND, D. (2021). How can experiments play a greater role in public policy? Twelve proposals from an economic model of scaling. Behavioural Public Policy, 5(1). https://doi.org/10.1017/bpp.2020.17.

Amanor-Boadu, V., Pfromm, P. H., & Nelson, R. (2014). Economic feasibility of algal biodiesel under alternative public policies. Renewable Energy, 67. https://doi.org/10.1016/j.renene.2013.11.029.

Anderson, M., Mckee, M., & Mossialos, E. (2020). Developing a sustainable exit strategy for COVID-19: health, economic and public policy implications. In Journal of the Royal Society of Medicine (Vol. 113, Issue 5). https://doi.org/10.1177/0141076820925229.

Andriansyah, A., Taufiqurokhman, T., & Wekke, I. S. (2019). Responsiveness of public policy and its impact on education management: An empirical assessment from Indonesia. Management Science Letters, 9(3). https://doi.org/10.5267/j.msl.2018.12.008.

Androniceanu, A., Gherghina, R., & Ciobănașu, M. (2019). The interdependence between fiscal public policies and tax evasion. Administratie Si Management Public, 2019(32). https://doi.org/10.24818/amp/2019.32-03.

Anguera-Torrell, O., Aznar-Alarcón, J. P., & Vives-Perez, J. (2020). COVID-19: hotel industry response to the pandemic evolution and to the public sector economic measures. Tourism Recreation Research. https://doi.org/10.1080/02508281.2020.1826225.

Arai, R., Naito, K., & Ono, T. (2018). Intergenerational policies, public debt, and economic growth: A politico-economic analysis. Journal of Public Economics, 166. https://doi.org/10.1016/j.jpubeco.2018.08.006.

Arbel, Y., Fialkoff, C., & Kerner, A. (2019). Public policy for reducing tax evasion: implications of the Yule-Simpson paradox. Applied Economics Letters, 26(13). https://doi.org/10.1080/13504851.2018.1537471.

Bakaki, Z., & Bernauer, T. (2018). Do economic conditions affect public support for environmental policy? Journal of Cleaner Production, 195. https://doi.org/10.1016/j.jclepro.2018.05.162.

Baker, S. D., Hollifield, B., & Osambela, E. (2020). Preventing controversial catastrophes. Review of Asset Pricing Studies, 10(1). https://doi.org/10.1093/RAPSTU/RAZ001.

Baldwin, R., Forslid, R., Martin, P., Ottaviano, G., & Robert-Nicoud, F. (2011). Economic geography and public policy. In Economic Geography and Public Policy. https://doi.org/10.1093/jnlecg/lbh045.

Bartels, L. M. (2005). Homer Gets a Tax Cut: Inequality and Public Policy in the American Mind. Perspectives on Politics, 3(1). https://doi.org/10.1017/S1537592705050036.

Bento, a. (2009). Biofuels: Economic and public policy considerations. Biofuels: Environmental Consequences and Implications of Changing Land Use, in RW Howarth and S. Bringezu (Eds.), September 2008.

Bergquist, P., Mildenberger, M., & Stokes, L. C. (2020). Combining climate, economic, and social policy builds public support for climate action in the US. Environmental Research Letters, 15(5). https://doi.org/10.1088/1748-9326/ab81c1.

Bhuiyan, S., & Farazmand, A. (2020). Society and Public Policy in the Middle East and North Africa. In International Journal of Public Administration (Vol. 43, Issue 5). https://doi.org/10.1080/01900692.2019.1707353.

Challoumis, C. (2018a). Analysis of the velocities of escaped savings with that of financial liquidity. Ekonomski Signali, 13(2), 1-14. https://doi.org/10.5937/ekonsig1802001c.

Challoumis, C. (2018b). Identification of Significant Economic Risks to the International Controlled Transactions. Economics and Applied Informatics, 2018(3), 149-153. https://doi.org/https://doi.org/10.26397/eai1584040927.

Challoumis, C. (2018c). Methods of Controlled Transactions and the Behavior of Companies According to the Public and Tax Policy. Economics, 6(1), 33-43. https://doi.org/10.2478/eoik-2018-0003.

Challoumis, C. (2018e). The Keynesian Theory and the Theory of Cycle of Money. Hyperion Economic Journal, 6(3), 3-8. https://hej.hyperion.ro/articles/3(6)_2018/HEJ nr3(6)_2018_A1Challoumis.pdf.

Challoumis, C. (2019b). The cycle of money with and without the escaped savings. Ekonomski Signali, 14(1), 89-99. https://doi.org/336.76 336.741.236.5.

Challoumis, C. (2020d). The Impact Factor of Education on the Public Sector – The Case of the U.S. International Journal of Business and Economic Sciences Applied Research, 13(1), 69-78. https://doi.org/10.25103/ijbesar.131.07.

Challoumis, C. (2021a). Chain of cycle of money. Acta Universitatis Bohemiae Meridionalis, 24(2), 4974.

Challoumis, C. (2021b). Index of the cycle of money – The case of Belarus. Economy and Banks, 2.

Challoumis, C. (2021c). Index of the cycle of money – The case of Greece. IJBESAR (International Journal of Business and Economic Sciences Applied Research), 14(2), 58-67.

Challoumis, C. (2021d). Index of the Cycle of Money – The Case of Latvia. Economics and Culture, 17(2), 5-12. https://doi.org/10.2478/jec-2020-0015.

Challoumis, C. (2021e). Index of the cycle of money – The case of Montenegro. Montenegrin Journal for Social Sciences, 5(1-2), 41-57.

Challoumis, C. (2021f). Index of the cycle of money – The case of Serbia. Open Journal for Research in Economics (OJRE), 4(1). https://centerprode.com/ojre.html.

Challoumis, C. (2021g). Index of the cycle of money – The case of Slovakia. STUDIACOMMERC I A LI A B R A T I S L A VE N S I A Ekonomická Univerzita v Bratislave, 14(49), 176-188.

Challoumis, C. (2021i). Index of the cycle of money – The case of Ukraine. Actual Problems of Economics, 243(9), 102-111. doi:10.32752/1993-6788-2021-1-243-244-102-111.

Challoumis, C. (2021k). The cycle of money with and without the enforcement savings. Complex System Research Centre.

Challoumis, C. (2022a). Conditions of the CM (Cycle of Money). In Social and Economic Studies within the Framework of Emerging Global Developments, Volume -1, V. Kaya (pp. 13-24). https://doi.org/10.3726/b19907.

Challoumis, C. (2022b). Impact Factor of the Rest Rewarding Taxes. In Complex System Research Centre. https://doi.org/10.2139/ssrn. 3154753.

Challoumis, C. (2022c). Index of the cycle of money – The case of Moldova. Eastern European Journal of Regional Economics, 8(1), 77-89.

Challoumis, C. (2022e). Structure of the economy. Actual Problems of Economics, 247(1).

Challoumis, C. (2023a). A comparison of the velocities of minimum escaped savings and financial liquidity. In Social and Economic Studies within the Framework of Emerging Global Developments, Volume – 4, V. Kaya (pp. 41-56). https://doi.org/10.3726/b21202.

Challoumis, C. (2023b). Capital and Risk in the Tax System. In Complex System Research Centre (pp. 241-244).

Challoumis, C. (2023c). Chain of the Cycle of Money with and without Maximum and Minimum Mixed Savings. European Multidisciplinary Journal of Modern Science, 23(2023), 1-16.

Challoumis, C. (2023d). Chain of the Cycle of Money with and Without Maximum Mixed Savings (Three-Dimensional Approach). Academic Journal of Digital Economics and Stability, 34(2023), 4365.

Challoumis, C. (2023e). Chain of the Cycle of Money with and without Minimum Mixed Savings (ThreeDimensional Approach). International Journal of Culture and Modernity, 33(2023), 22-33.

Challoumis, C. (2023f). Comparisons of the Cycle of Money Based on Enforcement and Escaped Savings. Pindus Journal of Culture, Literature, and ELT, 3(10), 19-28.

Challoumis, C. (2023g). Comparisons of the cycle of money with and without the mixed savings. Economics & Law. http://el.swu.bg/ikonomika/.

Challoumis, C. (2023h). Currency rate of the CM (Cycle of Money). Research Papers in Economics and Finance, 7(1).

Challoumis, C. (2023i). FROM SAVINGS TO ESCAPE AND ENFORCEMENT SAVINGS. Cogito, XV(4), 206-216.

Challoumis, C. (2023j). G7 – Global Minimum Corporate Tax Rate of . International Journal of Multicultural and Multireligious Understanding (IJMMU), 10(7).

Challoumis, C. (2023k). Impact factor of bureaucracy to the tax system. Ekonomski Signali.

Challoumis, C. (2023l). Impact Factor of Liability of Tax System According to the Theory of Cycle of Money. In Social and Economic Studies within the Framework of Emerging Global Developments Volume 3, V. Kaya (Vol. 3, pp. 31-42). https://doi.org/10.3726/b20968.

Challoumis, C. (2023s). Multiple Axiomatics Method and the Fuzzy Logic. MIDDLE EUROPEAN SCIENTIFIC BULLETIN, 37(1), 63-68.

Challoumis, C. (2023t). Principles for the Authorities on Activities with Controlled Transactions. Academic Journal of Digital Economics and Stability, 30(1), 136-152.

Challoumis, C. (2023u). Risk on the tax system of the E.U. from 2016 to 2022. Economics, 11(2).

Challoumis, C. (2023v). The Cycle of Money (C.M.) Considers Financial Liquidity with Minimum Mixed Savings. Open Journal for Research in Economics, 6(1), 1-12.

Challoumis, C. (2023w). The Cycle of Money with and Without the Maximum and Minimum Mixed Savings. Middle European Scientific Bulletin, 41(2023), 47-56.

Challoumis, C. (2023x). The cycle of money with and without the maximum mixed savings (Twodimensional approach). International Journal of Culture and Modernity, 33(2023), 34-45.

Challoumis, C. (2023y). The Cycle of Money with and Without the Minimum Mixed Savings. Pindus Journal of Culture, Literature, and ELT, 3(10), 29-39.

Challoumis, C. (2023z). The cycle of money with mixed savings. Open Journal for Research in Economics, 6(2), 41-50.

Challoumis, C. (2023aa). The Theory of Cycle of Money – How Do Principles of the Authorities on Public Policy, Taxes, and Controlled Transactions Affect the Economy and Society? International Journal of Social Science Research and Review (IJSSRR), 6(8).

Challoumis, C. (2023ab). The Velocities of Maximum Escaped Savings with than of Financial Liquidity to the Case of Mixed Savings. International Journal on Economics, Finance and Sustainable Development, 5(6), 124-133.

Challoumis, C. (2023ac). The Velocity of Escaped Savings and Maximum Financial Liquidity. Journal of Digital Economics and Stability, 34(2023), 55-65.

Challoumis, C. (2023ad). The Velocity of Escaped Savings and Velocity of Financial Liquidity. Middle European Scientific Bulletin, 41(2023), 57-66.

Challoumis, C. (2023ae). Utility of cycle of money with and without the enforcement savings. GOSPODARKA I INNOWACJE, 36(1), 269-277.

Challoumis, C. (2023af). Utility of Cycle of Money with and without the Escaping Savings. International Journal of Business Diplomacy and Economy, 2(6), 92-101.

Challoumis, C. (2023ag). Utility of Cycle of Money without the Escaping Savings (Protection of the Economy). In Social and Economic Studies within the Framework of Emerging Global Developments Volume 2, V. Kaya (pp. 53-64). https://doi.org/10.3726/b20509.

Challoumis, C. (2023ah). Velocity of Escaped Savings and Minimum Financial Liquidity According to the Theory of Cycle of Money. European Multidisciplinary Journal of Modern Science, 23(2023), 17-25.

Challoumis, C. (2024a). Impact Factors of Global Tax Revenue – Theory of Cycle of Money. International Journal of Multicultural and Multireligious Understanding, 11(1).

Challoumis, C. (2024b). Rewarding taxes on the cycle of money. In Social and Economic Studies within the Framework of Emerging Global Developments (Vol. 5).

Challoumis, C. (2024c). The impact factor of Tangibles and Intangibles of controlled transactions on economic performance. Economic Alternatives.

Challoumis, C. (2024d). THE INFLATION ACCORDING TO THE CYCLE OF MONEY (C.M.). Economic Alternatives.

Challoumis, C. (2024e). Velocity of the escaped savings and financial liquidity on maximum mixed savings. Open Journal for Research in Economics, 7(1).

Challoumis, C. (2024f). Velocity of the escaped savings and financial liquidity on minimum mixed savings. Open Journal for Research in Economics, 7(2).

Challoumis, C. (2024g). Velocity of the escaped savings and financial liquidity on mixed savings. Open Journal for Research in Economics, 7(2).

Constantinos Challoumis. (2024). Approach on arm’s length principle and fix length principle mathematical representations. In Innovations and Contemporary Trends in Business & Economics.

Delgado Rodríguez, M. J., & de Lucas Santos, S. (2018). Speed of economic convergence and EU public policy. Cuadernos de Economia, 41(115). https://doi.org/10.1016/j.cesjef.2017.01.001.

Deng, Y., & Li, H. (2011). RETRACTED ARTICLE: Measures of public economic policy under the financial crisis in China. In 2011 International Conference on E-Business and E-Government, ICEE2011 – Proceedings. https://doi.org/10.1109/ICEBEG.2011.5877027.

Diallo, S. Y., Shults, F. L. R., & Wildman, W. J. (2021). Minding morality: ethical artificial societies for public policy modeling. AI and Society, 36(1). https://doi.org/10.1007/s00146-020-01028-5.

Domingues, J. M., & Pecorelli-Pere, L. A. (2013). Electric vehicles, energy efficiency, taxes, and public policy in Brazil. LAW AND BUSINESS REVIEW OF THE AMERICAS, 19(55).

Erickson, K. (2016). Defining the public domain in economic terms – approaches and consequences for policy. In Etikk i Praksis (Vol. 10, Issue 1). https://doi.org/10.5324/eip.v10i1.1951.

Evans, W. N., Ringel, J. S., & Stech, D. (1999). Tobacco Taxes and Public Policy to Discourage Smoking. Tax Policy and the Economy, 13. https://doi.org/10.1086/tpe.13.20061866.

Ewert, B., Loer, K., & Thomann, E. (2021). Beyond nudge: advancing the state-of-the-art of behavioural public policy and administration. Policy and Politics, 49(1). https://doi.org/10.1332/030557320X15987279194319.

Fernando, J. (2022). Gross Domestic Product (GDP) Definition. In Investopedia.

Franko, W., Tolbert, C. J., & Witko, C. (2013). Inequality, Self-Interest, and Public Support for “Robin Hood” Tax Policies. Political Research Quarterly, 66(4). https://doi.org/10.1177/1065912913485441

Goldsztejn, U., Schwartzman, D., & Nehorai, A. (2020). Public policy and economic dynamics of COVID-19 spread: A mathematical modeling study. PLoS ONE, 15(12 December). https://doi.org/10.1371/journal.pone.0244174.

Grabs, J., Auld, G., & Cashore, B. (2020). Private regulation, public policy, and the perils of adverse ontological selection. Regulation and Governance. https://doi.org/10.1111/rego.12354.

Grove, A., Sanders, T., Salway, S., Goyder, E., & Hampshaw, S. (2020). A qualitative exploration of evidence-based decision making in public health practice and policy: The perceived usefulness of a diabetes economic model for decision makers. Evidence and Policy, 15(4). https://doi.org/10.1332/174426418X15245020185055.

Guardino, M., & Mettler, S. (2020). Revealing the “Hidden welfare state”: How policy information influences public attitudes about tax expenditures. Journal of Behavioral Public Administration, 3(1). https://doi.org/10.30636/jbpa.31.108.

GVELESIANI, R. (2019). COMPATIBILITY PROBLEM OF BASIC PUBLIC VALUES WITH ECONOMIC POLICY GOALS AND DECISIONS FOR THEIR IMPLEMENTATION. Globalization and Business, 4(7). https://doi.org/10.35945/gb.2019.07.004.

Hai, D. . (2016). Process of Public Policy Formulation in Developing Countries. Public Policy, C.

Hasselman, L., & Stoker, G. (2017). Market-based governance and water management: the limits to economic rationalism in public policy. Policy Studies, 38(5). https://doi.org/10.1080/01442872.2017.1360437.

Hausman, D., McPherson, M., & Satz, D. (2016). Economic Analysis, Moral Philosophy, and Public Policy. In Economic Analysis, Moral Philosophy, and Public Policy. https://doi.org/10.1017/9781316663011.

Howlett, M. (2020). Challenges in applying design thinking to public policy: Dealing with the varieties of policy formulation and their vicissitudes. Policy and Politics, 48(1). https://doi.org/10.1332/030557319X15613699681219.

Johnston, C. D., & Ballard, A. O. (2016). Economists and public opinion: Expert consensus and economic policy judgments. Journal of Politics, 78(2). https://doi.org/10.1086/684629.

Jomo, K. S., & Wee, C. H. (2003). The political economy of Malaysian federalism: Economic development, public policy and conflict containment. Journal of International Development, 15(4). https://doi.org/10.1002/jid.995.

Kamradt-Scott, A., & McInnes, C. (2012). The securitisation of pandemic influenza: Framing, security and public policy. Global Public Health, 7(SUPPL. 2). https://doi.org/10.1080/17441692.2012.725752.

Kananen, J. (2012). International ideas versus national traditions: Nordic economic and public policy as proposed by the OECD. Journal of Political Power, 5(3). https://doi.org/10.1080/2158379X.2012.735118.

Khadzhyradieva, S., Hrechko, T., & Smalskys, V. (2019). Institutionalisation of behavioural insights in public policy. In Public Policy and Administration (Vol. 18, Issue 3). https://doi.org/10.5755/J01.PPAA.18.3.24726.

Khan, S., & Liu, G. (2019). Socioeconomic and Public Policy Impacts of China Pakistan Economic Corridor on Khyber Pakhtunkhwa. Environmental Management and Sustainable Development, 8(1). https://doi.org/10.5296/emsd.v8i1.13758.

Kiktenko, O. V. (2020). ECONOMIC FEATURES OF PUBLIC POLICY IMPLEMENTATION IN THE EDUCATION SYSTEM. State and Regions. Series: Economics and Business, 2 (113). https://doi.org/10.32840/1814-1161/2020-2-30.

Kongats, K., McGetrick, J. A., Raine, K. D., Voyer, C., & Nykiforuk, C. I. J. (2019). Assessing general public and policy influencer support for healthy public policies to promote healthy eating at the population level in two Canadian provinces. Public Health Nutrition, 22(8). https://doi.org/10.1017/S1368980018004068.

Lajas, R., & Macário, R. (2020). Public policy framework supporting “mobility-as-a-service” implementation. Research in Transportation Economics, 83. https://doi.org/10.1016/j.retrec.2020.100905.

Laplane, A., & Mazzucato, M. (2020). Socializing the risks and rewards of public investments: Economic, policy, and legal issues. Research Policy: X, 2. https://doi.org/10.1016/j.repolx.2020.100008.

Loayza, N., & Pennings, S. M. (2020). Macroeconomic Policy in the Time of COVID-19 : A Primer for Developing Countries. World Bank Research and Policy Briefs, 147291.

Marume, S. B. M. (2016). Public Policy and Factors Influencing Public Policy. International Journal of Engineering Science Invention, 5(6).

Menguy, S. (2020). Tax competition, fiscal policy, and public debt levels in a monetary union. Journal of Economic Integration, 35(3). https://doi.org/10.11130/jei.2020.35.3.353.

Miailhe, N. (2017). Economic, Social and Public Policy Opportunities enabled by Automation. Field Actions Science Reports. The Journal of Field Actions, Special Issue 17.

Michener, J., & Brower, M. T. (2020). What’s policy got to do with it? Race, gender & economic inequality in the United States. Daedalus, 149(1). https://doi.org/10.1162/DAED_a_01776.

Miljand, M. (2020). Using systematic review methods to evaluate environmental public policy: methodological challenges and potential usefulness. Environmental Science and Policy, 105. https://doi.org/10.1016/j.envsci.2019.12.008

Nash, V., Bright, J., Margetts, H., & Lehdonvirta, V. (2017). Public Policy in the Platform Society. In Policy and Internet (Vol. 9, Issue 4). https://doi.org/10.1002/poi3.165.

Nayak, B. S. (2019). Reconceptualising Public Private Partnerships (PPPs) in global public policy. World Journal of Entrepreneurship, Management and Sustainable Development, 15(3). https://doi.org/10.1108/WJEMSD-04-2018-0041.

OECD, E. (2020). SME Policy Index – Eastern Partner Countries 2020 ASSESSING THE IMPLEMENTATION OF THE SMALL BUSINESS ACT FOR EUROPE. In OECD.

Rasmussen, K., & Callan, D. (2016). Schools of public policy and executive education: An opportunity missed? Policy and Society, 35(4). https://doi.org/10.1016/j.polsoc.2016.12.002.

Ribašauskiene, E., Šumyle, D., Volkov, A., Baležentis, T., Streimikiene, D., & Morkunas, M. (2019). Evaluating public policy support for agricultural cooperatives. Sustainability (Switzerland), 11(14). https://doi.org/10.3390/su11143769.

Sánchez, J. M., Rodríguez, J. P., & Espitia, H. E. (2020). Review of artificial intelligence applied in decision-making processes in agricultural public policy. In Processes (Vol. 8, Issue 11). https://doi.org/10.3390/pr8111374.

Schram, A. (2018). When evidence isn’t enough: Ideological, institutional, and interest-based constraints on achieving trade and health policy coherence. Global Social Policy, 18(1). https://doi.org/10.1177/1468018117744153.

Schwartz, M. (2019). Social and Economic Public Policy Goals and Their Impact on Defense Acquisition-A 2019 Update. Defense Acquisition Research Journal, 26(3). https://doi.org/10.22594/dau.19-827.26.03.

Snow, M. S. (1988). Telecommunications literature. A critical review of the economic, technological and public policy issues. Telecommunications Policy, 12(2). https://doi.org/10.1016/0308-5961(88)90007-9.

Spiel, C., Schober, B., & Strohmeier, D. (2018). Implementing intervention research into public policythe “I3-approach.” Prevention Science, 19(3). https://doi.org/10.1007/s11121-016-0638-3.

Strassheim, H. (2019). Behavioural mechanisms and public policy design: Preventing failures in behavioural public policy. Public Policy and Administration. https://doi.org/10.1177/0952076719827062.

Sultana, A., Or Rashid, M. H., Akter Eva, S., & Sultana, A. (2020). Assessment of Relationship Among Regional Economic Development Policy, Urban Development Policy and Public Policy. Sumerianz Journal of Economics and Finance, 310. https://doi.org/10.47752/sjef.310.171.177.

Swanstrom, T., Dreier, P., & Mollenkopf, J. (2002). Economic Inequality and Public Policy: The Power of Place. City & Community, 1(4). https://doi.org/10.1111/1540-6040.00030.

Taub, R. (2015). New Deal Ruins: Race, Economic Justice, and Public Housing Policy. Contemporary Sociology: A Journal of Reviews, 44(4). https://doi.org/10.1177/0094306115588487x.

Torres Salcido, G., del Roble Pensado Leglise, M., & Smolski, A. (2015). Food distribution’s socioeconomic relationships and public policy: Mexico City’s municipal public markets. Development in Practice, 25(3). https://doi.org/10.1080/09614524.2015.1016481.

Victral, D. M., Grossi, L. B., Ramos, A. M., & Gontijo, H. M. (2020). Economic sustainability of water supply public policy in Brazil semiarid regions. Research, Society and Development, 9(6). https://doi.org/10.33448/rsd-v9i6.3435.

Wangsness, P. B., Proost, S., & Rødseth, K. L. (2020). Vehicle choices and urban transport externalities. Are Norwegian policy makers getting it right? Transportation Research Part D: Transport and Environment, 86. https://doi.org/10.1016/j.trd.2020.102384.

Williamson, A. K., & Luke, B. (2020). Agenda-setting and Public Policy in Private Foundations. Nonprofit Policy Forum, 11(1). https://doi.org/10.1515/npf-2019-0049.

حقوق الطبع والنشر

تحتفظ المؤلف(ون) بحقوق الطبع والنشر لهذه المقالة، مع منح حقوق النشر الأولى للمجلة.

هذه مقالة مفتوحة الوصول موزعة بموجب الشروط والأحكام الخاصة برخصة المشاع الإبداعي (http://creativecommons.org/licenses/by/4.0/).

Journal: International Journal of Multicultural and Multireligious Understanding, Volume: 11, Issue: 5 DOI: https://doi.org/10.18415/ijmmu.v11i5.5608 Publication Date: 2024-05-08

The Cycle of Money – Minimum Escape Savings and Financial Liquidity

Constantinos ChalloumisNational and Kapodistrian University of Athens, Greece

This paper discusses the velocities of the minimum escape savings and financial liquidity. This means that it examined the behavior of the money cycle under normal conditions while controlling for the velocity of minimum escape savings and the velocity of financial liquidity. Therefore, it has determined how the economy works based on its cycle of money. Escape savings are the savings that leave the economy. The minimum escape savings simultaneously enhance the enforcement savings, leading them to their maximum level. The enforcement savings are the savings that stay in the economy. Thence, it is plausible to extract conclusions about the consumption and the investments in each economy. For this analysis has used a Q.E. method approach.

Keywords: Cycle of Money; Minimum Escape Savings; Financial Liquidity

Introduction

This paper examines the behavior of the money cycle when combined with the velocity of minimum escape savings and the velocity of financial liquidity (Bergquist et al., 2020; Cai, 2017; Camous & Gimber, 2018; Goldsztejn et al., 2020; Hai, 2016; Snow, 1988; Spiel et al., 2018; Wangsness et al., 2020). Contracts and agreements between participants in control transactions determine how profits and losses are allocated. The agreements should be mentioned the changes in the contracts (Aakre & Rübbelke, 2010; AL-UBAYDLI et al., 2021; Altman, 2012; Bhuiyan & Farazmand, 2020; Guardino & Mettler, 2020; Michener & Brower, 2020; Rasmussen & Callan, 2016; Swanstrom et al., 2002; Taub, 2015). This is the reason why the tax authorities should make periodic inspections. The periodic specification of contracts is important for the comparability analysis (Challoumis, 2018d, 2019c, 2019a, 2020c, 2021c, 2021f, 2022e, 2022d, 2023ac, 2023b, 2023j, 2023r, 2023m, 2023u, 2024b, 2024f). These periodic inspections of companies involved in controlled transactions are critical to the arm’s length principle. The cost-sharing is then determined by conducting periodic checks on tested parties. Moreover, should be notified that the companies of controlled transactions and the same time the inspections of tax authorities are done under the condition of proportional adjustments. The interpretation of the condition of the proportional adjustments is that the companies that participate in controlled transactions many times don’t have the appropriate data and uncontrolled transactions of similar circumstances to compare and therefore they proportionally adjust their data (Challoumis, 2019g, 2020d, 2021e, 2021b, 2021a, 2023e, 2023f, 2023ab, 2023h, 2024e, 2024d; Constantinos Challoumis, 2024). This means that if the

companies that are tested parties conclude that the profits and losses of companies from uncontrolled transactions are much higher or much fewer, and after that they make a proportional analogy to compare them with their data (Andriansyah et al., 2019; Evans et al., 1999; GVELESIANI, 2019; Khadzhyradieva et al., 2019; Lajas & Macário, 2020; Laplane & Mazzucato, 2020; Miljand, 2020; Torres Salcido et al., 2015; Williamson & Luke, 2020). The production of goods or services creates profits and costs for the companies:

The symbol is about the impact factor of the comparability analysis which has any method to the . The symbol z is a coefficient which takes values between 0 and 1 (Challoumis, 2018e, 2018a, 2019b, 2022c, 2023ad, 2023d, 2023g, 2023y, 2023af, 2023p, 2023aa, 2023c, 2023n, 2024g; Constantinos Challoumis, 2023). What value could be received is determined by the influence of the method (using the best method rule) on the . The symbol of is about the cost which comes up from the production of goods, and the symbol of is about the cost which comes from the distribution of the goods.

According to Eq. (1) to (6) is plausible to determine the following equations:

The symbol of in the prior equation is about the amount of taxes that should be paid to the companies of controlled transactions in the application of the arm’s length principle (Challoumis, 2018c, 2018b, 2019d, 2020b, 2021i, 2021h, 2021k, 2022b, 2023a, 2023i, 2023z, 2023ae, 2023w, 2024c). The is the amount of tax obligations that can be avoided through the allocations of profits and losses (AICPA, 2017; Bakaki & Bernauer, 2018; Diallo et al., 2021; Erickson, 2016; Grove et al., 2020; Sánchez et al., 2020; Schram, 2018; Schwartz, 2019; Victral et al., 2020). Moreover, is a coefficient for the rate of taxes. Then, the Eq. (4) shows the case of the arm’s length principle:

The symbol of in the previous equation shows the taxes that should be paid to the enterprises of controlled transactions in the application of the fixed length principle. Then, is a coefficient for the rate of taxes in the case of the fixed length principle:

The tax for the companies that participate in controlled transactions of transfer pricing in the case of the fixed length principle is higher or at least equal to that of the case of the arm’s length principle. Thereupon, with the fixed length principle the enterprises of controlled transactions can tackle issues that come from the allocation of profits and losses (Anderson et al., 2020; Bento, 2009; Ewert et al., 2021; Hausman et al., 2016; Johnston & Ballard, 2016; Loayza & Pennings, 2020; Menguy, 2020; Mueller, 2020; Nayak, 2019). Therefore, the tax authorities can face the transfer pricing effects on the global tax revenue. The fixed length principle permits the recovery of the tax losses of the global tax revenue from the controlled transactions of the transfer pricing (Abdelkafi, 2018; Domingues & Pecorelli-Pere, 2013; Holcombe, 1998; Howlett, 2020; Kananen, 2012; Kiktenko, 2020; Maxwell, 2020; OECD, 2020; Stone,

2008). The next scheme illustrates the procedure that companies of controlled transactions follow for their allocations of profits and losses, the proportional adjustments of data, and the fixed length principle:

Figure 1: Arm’s length principle of fixed length principle

Fig. 1 determines the procedure of the fixed length principle and its quantity analysis for the determination of the behavior of the model. The next section presents the theory of cycle of money. The applied methodology is the Q.E. method and its econometric approach.

Methodology

The tax revenues correspond to the savings that the companies could have if the taxes were avoided. The way that these savings are administrated is different from case to case. Then the benefits of the companies could be managed in a completely different way, as could be saved or could be taxed. The theory of cycle of money shows when the savings robust the economy and when the taxes robust the economy. This determination must be a separation of savings into the non-returned savings (or escape savings) and the returned savings (or enforcement savings:

The variable of symbolizes the case of the escape savings. This means that there are savings that are not returning to the economy or come back after a long-term period. The variable of symbolizes the case that there are escape savings that come from transfer pricing activities. The variable of symbolizes the case that there are escape savings not from transfer pricing activities but from any other commercial activity. For instance, could refer to the commercial activities that come from

uncontrolled transactions. The variable of symbolizes the financial liquidity in an economy. The variable of symbolizes the consumption in an economy. The variable of symbolizes the enforcement savings, which come from the citizens and small and medium-sized enterprises. The variable of symbolizes the condition of financial liquidity in an economy. The variable of symbolizes the velocity of financial liquidity increases or decreases. The variable of symbolizes the velocity of escape savings. Therefore, the variable of symbolizes the term of the cycle of money (Challoumis, 2019f, 2019e, 2021d, 2023o, 2023k, 2023q, 2023v, 2023s, 2023ah, 2023ag, 2024a).

Thereupon, the cycle of money shows the level of the dynamic of an economy and its robustness. Therefore, it has been obtained that the cycle of money grows when there is a tax system like the case of the fixed length principle which permits the low taxation of uncontrolled transactions and the higher taxation of controlled transactions (Bartels, 2005; Delgado Rodríguez & de Lucas Santos, 2018; Deng & Li, 2011; Khan & Liu, 2019; Kongats et al., 2019; Sultana et al., 2020). Should be mentioned that as uncontrolled transactions are considered the same happens with the cases of the financial liquidity of citizens and the small and middle-sized companies. Moreover, there are three basic impact factors of the rewarding taxes (Challoumis, 2018f, 2020a, 2021g, 2021j, 2022a, 2023t, 2023l, 2023x). The rewarding taxes are the only taxes that have an immediate and important role in the market of any economy. These factors are affiliated with education, with the health system of each society, and with the rest relevant structural economic factors of the prior two impact factors:

Figure 2: The cycle of money with rewarding taxes

The previous scheme represents the cycle of money additionally with all the rewarding tax factors:

In the prior two equations used some impact factors, which are the which is also demonstrated in Eq. (14), moreover the variables and the . The variable symbolizes the impact factor of the rest rewarding taxes. The symbol of is the impact factor of education and any technical knowledge (Challoumis, 2019g; Grabs et al., 2020; Hasselman & Stoker, 2017; Jomo & Wee, 2003; Kamradt-Scott & McInnes, 2012; Marume, 2016; Miailhe, 2017; Nash et al., 2017; Oueslati, 2015; Ribašauskiene et al., 2019; Strassheim, 2019; Suslov & Basareva, 2020). The symbol of is about the impact factor of health anything relevant and supporting of this issue. The symbol of , and of the , are the coefficients of the health and the health impact factor accordingly (Aitken, 2019; AL-

UBAYDLI et al., 2021; Altman, 2012; Amanor-Boadu et al., 2014; Andriansyah et al., 2019; Androniceanu et al., 2019; Anguera-Torrell et al., 2020; Arai et al., 2018; Arbel et al., 2019; Azzone, 2018; Baker et al., 2020; Baldwin et al., 2011; Fernando, 2022; Franko et al., 2013).

Results

Using Eq. (6) to (15) it is plausible to proceed to the mixed savings. Using Eq. (1) to (15) it is plausible to define the behavior of the utility of the cycle of money. Moreover, including the mixed savings :

In the previous equations the which represents the mixed savings. The role of mixed savings is to represent that simultaneously the factories, the research, and the development centers have escape savings. The rest symbols are already defined.

In the prior equations the and the are accordingly the initial values of the velocity of escape savings and the cycle of money. Moreover, the equation of represents the general equation of the escape savings:

Eq. (26) is about the general form of the velocity of the cycle of money. The coefficients of , took two of them one constant value , and the other one is zero. The same happens with the coefficients of which also two of them take one constant value and the other one is zero. In that way, there are all the possible combinations of velocities of escape savings and financial liquidities to be defined by two concrete equations.

The table of coefficients for the cycle of money is this:

Table: compiling coefficients

Factors

Values

0.6

0.7

0.9

0.8

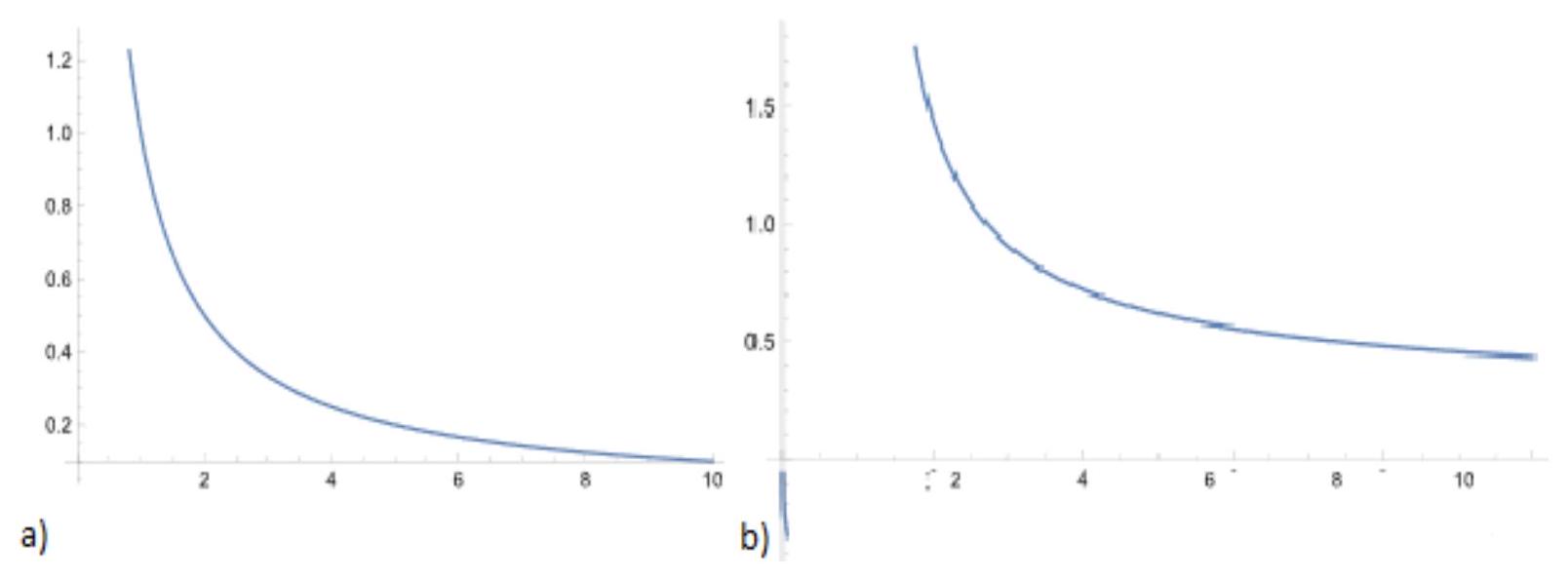

Applying the Q.E. method with the prior coefficients:

Figure 3: Cycle of money with its velocities

Eq. (29) represents the velocity of escape savings in Fig. 3a. Eq. (30) represents the financial liquidity in Fig. 2b. The velocity of escape savings when it is at its minimum level the financial liquidity has increased offering a higher cycle of money. Therefore, the economy has been boosted.

Conclusions

In this paper, it has concluded that in the cycle of money when there the escape savings are limited the economy has a maximum positive orientation. This means that the consumption and the investments would be increased in any economy, at the maximum level. But, also it has determined that limited escape savings transform the logarithmic form of the velocity of escape savings into a linear form.

References

Aakre, S., & Rübbelke, D. T. G. (2010). Objectives of public economic policy and the adaptation to climate change. Journal of Environmental Planning and Management, 53(6). https://doi.org/10.1080/09640568.2010.488116.

Abdelkafi, I. (2018). The Relationship Between Public Debt, Economic Growth, and Monetary Policy: Empirical Evidence from Tunisia. Journal of the Knowledge Economy, 9(4). https://doi.org/10.1007/s13132-016-0404-6.

AICPA. (2017). Guiding principles of good tax policy: A framework for evaluating tax proposals. American Institute of Certified Public Accountants, 2017(March 2001).

AL-UBAYDLI, O., LEE, M. S., LIST, J. A., MACKEVICIUS, C. L., & SUSKIND, D. (2021). How can experiments play a greater role in public policy? Twelve proposals from an economic model of scaling. Behavioural Public Policy, 5(1). https://doi.org/10.1017/bpp.2020.17.

Amanor-Boadu, V., Pfromm, P. H., & Nelson, R. (2014). Economic feasibility of algal biodiesel under alternative public policies. Renewable Energy, 67. https://doi.org/10.1016/j.renene.2013.11.029.

Anderson, M., Mckee, M., & Mossialos, E. (2020). Developing a sustainable exit strategy for COVID-19: health, economic and public policy implications. In Journal of the Royal Society of Medicine (Vol. 113, Issue 5). https://doi.org/10.1177/0141076820925229.

Andriansyah, A., Taufiqurokhman, T., & Wekke, I. S. (2019). Responsiveness of public policy and its impact on education management: An empirical assessment from Indonesia. Management Science Letters, 9(3). https://doi.org/10.5267/j.msl.2018.12.008.

Androniceanu, A., Gherghina, R., & Ciobănașu, M. (2019). The interdependence between fiscal public policies and tax evasion. Administratie Si Management Public, 2019(32). https://doi.org/10.24818/amp/2019.32-03.

Anguera-Torrell, O., Aznar-Alarcón, J. P., & Vives-Perez, J. (2020). COVID-19: hotel industry response to the pandemic evolution and to the public sector economic measures. Tourism Recreation Research. https://doi.org/10.1080/02508281.2020.1826225.

Arai, R., Naito, K., & Ono, T. (2018). Intergenerational policies, public debt, and economic growth: A politico-economic analysis. Journal of Public Economics, 166. https://doi.org/10.1016/j.jpubeco.2018.08.006.

Arbel, Y., Fialkoff, C., & Kerner, A. (2019). Public policy for reducing tax evasion: implications of the Yule-Simpson paradox. Applied Economics Letters, 26(13). https://doi.org/10.1080/13504851.2018.1537471.

Bakaki, Z., & Bernauer, T. (2018). Do economic conditions affect public support for environmental policy? Journal of Cleaner Production, 195. https://doi.org/10.1016/j.jclepro.2018.05.162.

Baker, S. D., Hollifield, B., & Osambela, E. (2020). Preventing controversial catastrophes. Review of Asset Pricing Studies, 10(1). https://doi.org/10.1093/RAPSTU/RAZ001.

Baldwin, R., Forslid, R., Martin, P., Ottaviano, G., & Robert-Nicoud, F. (2011). Economic geography and public policy. In Economic Geography and Public Policy. https://doi.org/10.1093/jnlecg/lbh045.

Bartels, L. M. (2005). Homer Gets a Tax Cut: Inequality and Public Policy in the American Mind. Perspectives on Politics, 3(1). https://doi.org/10.1017/S1537592705050036.

Bento, a. (2009). Biofuels: Economic and public policy considerations. Biofuels: Environmental Consequences and Implications of Changing Land Use, in RW Howarth and S. Bringezu (Eds.), September 2008.

Bergquist, P., Mildenberger, M., & Stokes, L. C. (2020). Combining climate, economic, and social policy builds public support for climate action in the US. Environmental Research Letters, 15(5). https://doi.org/10.1088/1748-9326/ab81c1.

Bhuiyan, S., & Farazmand, A. (2020). Society and Public Policy in the Middle East and North Africa. In International Journal of Public Administration (Vol. 43, Issue 5). https://doi.org/10.1080/01900692.2019.1707353.

Challoumis, C. (2018a). Analysis of the velocities of escaped savings with that of financial liquidity. Ekonomski Signali, 13(2), 1-14. https://doi.org/10.5937/ekonsig1802001c.

Challoumis, C. (2018b). Identification of Significant Economic Risks to the International Controlled Transactions. Economics and Applied Informatics, 2018(3), 149-153. https://doi.org/https://doi.org/10.26397/eai1584040927.

Challoumis, C. (2018c). Methods of Controlled Transactions and the Behavior of Companies According to the Public and Tax Policy. Economics, 6(1), 33-43. https://doi.org/10.2478/eoik-2018-0003.

Challoumis, C. (2018e). The Keynesian Theory and the Theory of Cycle of Money. Hyperion Economic Journal, 6(3), 3-8. https://hej.hyperion.ro/articles/3(6)_2018/HEJ nr3(6)_2018_A1Challoumis.pdf.

Challoumis, C. (2019b). The cycle of money with and without the escaped savings. Ekonomski Signali, 14(1), 89-99. https://doi.org/336.76 336.741.236.5.

Challoumis, C. (2020d). The Impact Factor of Education on the Public Sector – The Case of the U.S. International Journal of Business and Economic Sciences Applied Research, 13(1), 69-78. https://doi.org/10.25103/ijbesar.131.07.

Challoumis, C. (2021a). Chain of cycle of money. Acta Universitatis Bohemiae Meridionalis, 24(2), 4974.

Challoumis, C. (2021b). Index of the cycle of money – The case of Belarus. Economy and Banks, 2.

Challoumis, C. (2021c). Index of the cycle of money – The case of Greece. IJBESAR (International Journal of Business and Economic Sciences Applied Research), 14(2), 58-67.

Challoumis, C. (2021d). Index of the Cycle of Money – The Case of Latvia. Economics and Culture, 17(2), 5-12. https://doi.org/10.2478/jec-2020-0015.

Challoumis, C. (2021e). Index of the cycle of money – The case of Montenegro. Montenegrin Journal for Social Sciences, 5(1-2), 41-57.

Challoumis, C. (2021f). Index of the cycle of money – The case of Serbia. Open Journal for Research in Economics (OJRE), 4(1). https://centerprode.com/ojre.html.

Challoumis, C. (2021g). Index of the cycle of money – The case of Slovakia. STUDIACOMMERC I A LI A B R A T I S L A VE N S I A Ekonomická Univerzita v Bratislave, 14(49), 176-188.

Challoumis, C. (2021i). Index of the cycle of money – The case of Ukraine. Actual Problems of Economics, 243(9), 102-111. doi:10.32752/1993-6788-2021-1-243-244-102-111.

Challoumis, C. (2021k). The cycle of money with and without the enforcement savings. Complex System Research Centre.

Challoumis, C. (2022a). Conditions of the CM (Cycle of Money). In Social and Economic Studies within the Framework of Emerging Global Developments, Volume -1, V. Kaya (pp. 13-24). https://doi.org/10.3726/b19907.

Challoumis, C. (2022b). Impact Factor of the Rest Rewarding Taxes. In Complex System Research Centre. https://doi.org/10.2139/ssrn. 3154753.

Challoumis, C. (2022c). Index of the cycle of money – The case of Moldova. Eastern European Journal of Regional Economics, 8(1), 77-89.

Challoumis, C. (2022e). Structure of the economy. Actual Problems of Economics, 247(1).

Challoumis, C. (2023a). A comparison of the velocities of minimum escaped savings and financial liquidity. In Social and Economic Studies within the Framework of Emerging Global Developments, Volume – 4, V. Kaya (pp. 41-56). https://doi.org/10.3726/b21202.

Challoumis, C. (2023b). Capital and Risk in the Tax System. In Complex System Research Centre (pp. 241-244).

Challoumis, C. (2023c). Chain of the Cycle of Money with and without Maximum and Minimum Mixed Savings. European Multidisciplinary Journal of Modern Science, 23(2023), 1-16.

Challoumis, C. (2023d). Chain of the Cycle of Money with and Without Maximum Mixed Savings (Three-Dimensional Approach). Academic Journal of Digital Economics and Stability, 34(2023), 4365.

Challoumis, C. (2023e). Chain of the Cycle of Money with and without Minimum Mixed Savings (ThreeDimensional Approach). International Journal of Culture and Modernity, 33(2023), 22-33.

Challoumis, C. (2023f). Comparisons of the Cycle of Money Based on Enforcement and Escaped Savings. Pindus Journal of Culture, Literature, and ELT, 3(10), 19-28.

Challoumis, C. (2023g). Comparisons of the cycle of money with and without the mixed savings. Economics & Law. http://el.swu.bg/ikonomika/.

Challoumis, C. (2023h). Currency rate of the CM (Cycle of Money). Research Papers in Economics and Finance, 7(1).

Challoumis, C. (2023i). FROM SAVINGS TO ESCAPE AND ENFORCEMENT SAVINGS. Cogito, XV(4), 206-216.

Challoumis, C. (2023j). G7 – Global Minimum Corporate Tax Rate of . International Journal of Multicultural and Multireligious Understanding (IJMMU), 10(7).

Challoumis, C. (2023k). Impact factor of bureaucracy to the tax system. Ekonomski Signali.

Challoumis, C. (2023l). Impact Factor of Liability of Tax System According to the Theory of Cycle of Money. In Social and Economic Studies within the Framework of Emerging Global Developments Volume 3, V. Kaya (Vol. 3, pp. 31-42). https://doi.org/10.3726/b20968.

Challoumis, C. (2023s). Multiple Axiomatics Method and the Fuzzy Logic. MIDDLE EUROPEAN SCIENTIFIC BULLETIN, 37(1), 63-68.

Challoumis, C. (2023t). Principles for the Authorities on Activities with Controlled Transactions. Academic Journal of Digital Economics and Stability, 30(1), 136-152.

Challoumis, C. (2023u). Risk on the tax system of the E.U. from 2016 to 2022. Economics, 11(2).

Challoumis, C. (2023v). The Cycle of Money (C.M.) Considers Financial Liquidity with Minimum Mixed Savings. Open Journal for Research in Economics, 6(1), 1-12.

Challoumis, C. (2023w). The Cycle of Money with and Without the Maximum and Minimum Mixed Savings. Middle European Scientific Bulletin, 41(2023), 47-56.

Challoumis, C. (2023x). The cycle of money with and without the maximum mixed savings (Twodimensional approach). International Journal of Culture and Modernity, 33(2023), 34-45.

Challoumis, C. (2023y). The Cycle of Money with and Without the Minimum Mixed Savings. Pindus Journal of Culture, Literature, and ELT, 3(10), 29-39.

Challoumis, C. (2023z). The cycle of money with mixed savings. Open Journal for Research in Economics, 6(2), 41-50.

Challoumis, C. (2023aa). The Theory of Cycle of Money – How Do Principles of the Authorities on Public Policy, Taxes, and Controlled Transactions Affect the Economy and Society? International Journal of Social Science Research and Review (IJSSRR), 6(8).

Challoumis, C. (2023ab). The Velocities of Maximum Escaped Savings with than of Financial Liquidity to the Case of Mixed Savings. International Journal on Economics, Finance and Sustainable Development, 5(6), 124-133.

Challoumis, C. (2023ac). The Velocity of Escaped Savings and Maximum Financial Liquidity. Journal of Digital Economics and Stability, 34(2023), 55-65.

Challoumis, C. (2023ad). The Velocity of Escaped Savings and Velocity of Financial Liquidity. Middle European Scientific Bulletin, 41(2023), 57-66.

Challoumis, C. (2023ae). Utility of cycle of money with and without the enforcement savings. GOSPODARKA I INNOWACJE, 36(1), 269-277.

Challoumis, C. (2023af). Utility of Cycle of Money with and without the Escaping Savings. International Journal of Business Diplomacy and Economy, 2(6), 92-101.

Challoumis, C. (2023ag). Utility of Cycle of Money without the Escaping Savings (Protection of the Economy). In Social and Economic Studies within the Framework of Emerging Global Developments Volume 2, V. Kaya (pp. 53-64). https://doi.org/10.3726/b20509.

Challoumis, C. (2023ah). Velocity of Escaped Savings and Minimum Financial Liquidity According to the Theory of Cycle of Money. European Multidisciplinary Journal of Modern Science, 23(2023), 17-25.

Challoumis, C. (2024a). Impact Factors of Global Tax Revenue – Theory of Cycle of Money. International Journal of Multicultural and Multireligious Understanding, 11(1).

Challoumis, C. (2024b). Rewarding taxes on the cycle of money. In Social and Economic Studies within the Framework of Emerging Global Developments (Vol. 5).

Challoumis, C. (2024c). The impact factor of Tangibles and Intangibles of controlled transactions on economic performance. Economic Alternatives.

Challoumis, C. (2024d). THE INFLATION ACCORDING TO THE CYCLE OF MONEY (C.M.). Economic Alternatives.

Challoumis, C. (2024e). Velocity of the escaped savings and financial liquidity on maximum mixed savings. Open Journal for Research in Economics, 7(1).

Challoumis, C. (2024f). Velocity of the escaped savings and financial liquidity on minimum mixed savings. Open Journal for Research in Economics, 7(2).

Challoumis, C. (2024g). Velocity of the escaped savings and financial liquidity on mixed savings. Open Journal for Research in Economics, 7(2).

Constantinos Challoumis. (2024). Approach on arm’s length principle and fix length principle mathematical representations. In Innovations and Contemporary Trends in Business & Economics.

Delgado Rodríguez, M. J., & de Lucas Santos, S. (2018). Speed of economic convergence and EU public policy. Cuadernos de Economia, 41(115). https://doi.org/10.1016/j.cesjef.2017.01.001.

Deng, Y., & Li, H. (2011). RETRACTED ARTICLE: Measures of public economic policy under the financial crisis in China. In 2011 International Conference on E-Business and E-Government, ICEE2011 – Proceedings. https://doi.org/10.1109/ICEBEG.2011.5877027.

Diallo, S. Y., Shults, F. L. R., & Wildman, W. J. (2021). Minding morality: ethical artificial societies for public policy modeling. AI and Society, 36(1). https://doi.org/10.1007/s00146-020-01028-5.

Domingues, J. M., & Pecorelli-Pere, L. A. (2013). Electric vehicles, energy efficiency, taxes, and public policy in Brazil. LAW AND BUSINESS REVIEW OF THE AMERICAS, 19(55).

Erickson, K. (2016). Defining the public domain in economic terms – approaches and consequences for policy. In Etikk i Praksis (Vol. 10, Issue 1). https://doi.org/10.5324/eip.v10i1.1951.

Evans, W. N., Ringel, J. S., & Stech, D. (1999). Tobacco Taxes and Public Policy to Discourage Smoking. Tax Policy and the Economy, 13. https://doi.org/10.1086/tpe.13.20061866.

Ewert, B., Loer, K., & Thomann, E. (2021). Beyond nudge: advancing the state-of-the-art of behavioural public policy and administration. Policy and Politics, 49(1). https://doi.org/10.1332/030557320X15987279194319.

Fernando, J. (2022). Gross Domestic Product (GDP) Definition. In Investopedia.

Franko, W., Tolbert, C. J., & Witko, C. (2013). Inequality, Self-Interest, and Public Support for “Robin Hood” Tax Policies. Political Research Quarterly, 66(4). https://doi.org/10.1177/1065912913485441

Goldsztejn, U., Schwartzman, D., & Nehorai, A. (2020). Public policy and economic dynamics of COVID-19 spread: A mathematical modeling study. PLoS ONE, 15(12 December). https://doi.org/10.1371/journal.pone.0244174.

Grabs, J., Auld, G., & Cashore, B. (2020). Private regulation, public policy, and the perils of adverse ontological selection. Regulation and Governance. https://doi.org/10.1111/rego.12354.

Grove, A., Sanders, T., Salway, S., Goyder, E., & Hampshaw, S. (2020). A qualitative exploration of evidence-based decision making in public health practice and policy: The perceived usefulness of a diabetes economic model for decision makers. Evidence and Policy, 15(4). https://doi.org/10.1332/174426418X15245020185055.

Guardino, M., & Mettler, S. (2020). Revealing the “Hidden welfare state”: How policy information influences public attitudes about tax expenditures. Journal of Behavioral Public Administration, 3(1). https://doi.org/10.30636/jbpa.31.108.

GVELESIANI, R. (2019). COMPATIBILITY PROBLEM OF BASIC PUBLIC VALUES WITH ECONOMIC POLICY GOALS AND DECISIONS FOR THEIR IMPLEMENTATION. Globalization and Business, 4(7). https://doi.org/10.35945/gb.2019.07.004.

Hai, D. . (2016). Process of Public Policy Formulation in Developing Countries. Public Policy, C.

Hasselman, L., & Stoker, G. (2017). Market-based governance and water management: the limits to economic rationalism in public policy. Policy Studies, 38(5). https://doi.org/10.1080/01442872.2017.1360437.

Hausman, D., McPherson, M., & Satz, D. (2016). Economic Analysis, Moral Philosophy, and Public Policy. In Economic Analysis, Moral Philosophy, and Public Policy. https://doi.org/10.1017/9781316663011.

Howlett, M. (2020). Challenges in applying design thinking to public policy: Dealing with the varieties of policy formulation and their vicissitudes. Policy and Politics, 48(1). https://doi.org/10.1332/030557319X15613699681219.

Johnston, C. D., & Ballard, A. O. (2016). Economists and public opinion: Expert consensus and economic policy judgments. Journal of Politics, 78(2). https://doi.org/10.1086/684629.

Jomo, K. S., & Wee, C. H. (2003). The political economy of Malaysian federalism: Economic development, public policy and conflict containment. Journal of International Development, 15(4). https://doi.org/10.1002/jid.995.

Kamradt-Scott, A., & McInnes, C. (2012). The securitisation of pandemic influenza: Framing, security and public policy. Global Public Health, 7(SUPPL. 2). https://doi.org/10.1080/17441692.2012.725752.

Kananen, J. (2012). International ideas versus national traditions: Nordic economic and public policy as proposed by the OECD. Journal of Political Power, 5(3). https://doi.org/10.1080/2158379X.2012.735118.

Khadzhyradieva, S., Hrechko, T., & Smalskys, V. (2019). Institutionalisation of behavioural insights in public policy. In Public Policy and Administration (Vol. 18, Issue 3). https://doi.org/10.5755/J01.PPAA.18.3.24726.

Khan, S., & Liu, G. (2019). Socioeconomic and Public Policy Impacts of China Pakistan Economic Corridor on Khyber Pakhtunkhwa. Environmental Management and Sustainable Development, 8(1). https://doi.org/10.5296/emsd.v8i1.13758.

Kiktenko, O. V. (2020). ECONOMIC FEATURES OF PUBLIC POLICY IMPLEMENTATION IN THE EDUCATION SYSTEM. State and Regions. Series: Economics and Business, 2 (113). https://doi.org/10.32840/1814-1161/2020-2-30.

Kongats, K., McGetrick, J. A., Raine, K. D., Voyer, C., & Nykiforuk, C. I. J. (2019). Assessing general public and policy influencer support for healthy public policies to promote healthy eating at the population level in two Canadian provinces. Public Health Nutrition, 22(8). https://doi.org/10.1017/S1368980018004068.

Lajas, R., & Macário, R. (2020). Public policy framework supporting “mobility-as-a-service” implementation. Research in Transportation Economics, 83. https://doi.org/10.1016/j.retrec.2020.100905.

Laplane, A., & Mazzucato, M. (2020). Socializing the risks and rewards of public investments: Economic, policy, and legal issues. Research Policy: X, 2. https://doi.org/10.1016/j.repolx.2020.100008.

Loayza, N., & Pennings, S. M. (2020). Macroeconomic Policy in the Time of COVID-19 : A Primer for Developing Countries. World Bank Research and Policy Briefs, 147291.

Marume, S. B. M. (2016). Public Policy and Factors Influencing Public Policy. International Journal of Engineering Science Invention, 5(6).

Menguy, S. (2020). Tax competition, fiscal policy, and public debt levels in a monetary union. Journal of Economic Integration, 35(3). https://doi.org/10.11130/jei.2020.35.3.353.

Miailhe, N. (2017). Economic, Social and Public Policy Opportunities enabled by Automation. Field Actions Science Reports. The Journal of Field Actions, Special Issue 17.

Michener, J., & Brower, M. T. (2020). What’s policy got to do with it? Race, gender & economic inequality in the United States. Daedalus, 149(1). https://doi.org/10.1162/DAED_a_01776.

Miljand, M. (2020). Using systematic review methods to evaluate environmental public policy: methodological challenges and potential usefulness. Environmental Science and Policy, 105. https://doi.org/10.1016/j.envsci.2019.12.008

Nash, V., Bright, J., Margetts, H., & Lehdonvirta, V. (2017). Public Policy in the Platform Society. In Policy and Internet (Vol. 9, Issue 4). https://doi.org/10.1002/poi3.165.

Nayak, B. S. (2019). Reconceptualising Public Private Partnerships (PPPs) in global public policy. World Journal of Entrepreneurship, Management and Sustainable Development, 15(3). https://doi.org/10.1108/WJEMSD-04-2018-0041.

OECD, E. (2020). SME Policy Index – Eastern Partner Countries 2020 ASSESSING THE IMPLEMENTATION OF THE SMALL BUSINESS ACT FOR EUROPE. In OECD.

Rasmussen, K., & Callan, D. (2016). Schools of public policy and executive education: An opportunity missed? Policy and Society, 35(4). https://doi.org/10.1016/j.polsoc.2016.12.002.

Ribašauskiene, E., Šumyle, D., Volkov, A., Baležentis, T., Streimikiene, D., & Morkunas, M. (2019). Evaluating public policy support for agricultural cooperatives. Sustainability (Switzerland), 11(14). https://doi.org/10.3390/su11143769.

Sánchez, J. M., Rodríguez, J. P., & Espitia, H. E. (2020). Review of artificial intelligence applied in decision-making processes in agricultural public policy. In Processes (Vol. 8, Issue 11). https://doi.org/10.3390/pr8111374.

Schram, A. (2018). When evidence isn’t enough: Ideological, institutional, and interest-based constraints on achieving trade and health policy coherence. Global Social Policy, 18(1). https://doi.org/10.1177/1468018117744153.

Schwartz, M. (2019). Social and Economic Public Policy Goals and Their Impact on Defense Acquisition-A 2019 Update. Defense Acquisition Research Journal, 26(3). https://doi.org/10.22594/dau.19-827.26.03.

Snow, M. S. (1988). Telecommunications literature. A critical review of the economic, technological and public policy issues. Telecommunications Policy, 12(2). https://doi.org/10.1016/0308-5961(88)90007-9.

Spiel, C., Schober, B., & Strohmeier, D. (2018). Implementing intervention research into public policythe “I3-approach.” Prevention Science, 19(3). https://doi.org/10.1007/s11121-016-0638-3.

Strassheim, H. (2019). Behavioural mechanisms and public policy design: Preventing failures in behavioural public policy. Public Policy and Administration. https://doi.org/10.1177/0952076719827062.

Sultana, A., Or Rashid, M. H., Akter Eva, S., & Sultana, A. (2020). Assessment of Relationship Among Regional Economic Development Policy, Urban Development Policy and Public Policy. Sumerianz Journal of Economics and Finance, 310. https://doi.org/10.47752/sjef.310.171.177.

Swanstrom, T., Dreier, P., & Mollenkopf, J. (2002). Economic Inequality and Public Policy: The Power of Place. City & Community, 1(4). https://doi.org/10.1111/1540-6040.00030.

Taub, R. (2015). New Deal Ruins: Race, Economic Justice, and Public Housing Policy. Contemporary Sociology: A Journal of Reviews, 44(4). https://doi.org/10.1177/0094306115588487x.

Torres Salcido, G., del Roble Pensado Leglise, M., & Smolski, A. (2015). Food distribution’s socioeconomic relationships and public policy: Mexico City’s municipal public markets. Development in Practice, 25(3). https://doi.org/10.1080/09614524.2015.1016481.

Victral, D. M., Grossi, L. B., Ramos, A. M., & Gontijo, H. M. (2020). Economic sustainability of water supply public policy in Brazil semiarid regions. Research, Society and Development, 9(6). https://doi.org/10.33448/rsd-v9i6.3435.

Wangsness, P. B., Proost, S., & Rødseth, K. L. (2020). Vehicle choices and urban transport externalities. Are Norwegian policy makers getting it right? Transportation Research Part D: Transport and Environment, 86. https://doi.org/10.1016/j.trd.2020.102384.

Williamson, A. K., & Luke, B. (2020). Agenda-setting and Public Policy in Private Foundations. Nonprofit Policy Forum, 11(1). https://doi.org/10.1515/npf-2019-0049.

Copyrights

Copyright for this article is retained by the author(s), with first publication rights granted to the journal.

This is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).