DOI: https://doi.org/10.1007/s43621-025-00804-x

تاريخ النشر: 2025-01-21

مراجعة

كشف تأثير الثلاثي للأبعاد على أداء الأعمال

نُشر على الإنترنت: 21 يناير 2025

© المؤلفون 2025 مفتوح

الملخص

لقد أصبح التعامل مع التحديات البيئية والاجتماعية والاقتصادية أولوية عالمية ملحة. يوفر إطار العمل المعروف باسم الثلاثة خطوط الأساسية (TBL) نهجًا شاملاً لتقييم أداء الشركات من خلال دمج الجوانب الاقتصادية والبيئية والاجتماعية. على الرغم من تزايد اعتماده في كل من الأبحاث الإدارية والأكاديمية، لا يزال هناك فجوة كبيرة في فهم كيفية تأثير إطار العمل TBL على أداء الأعمال. لمعالجة ذلك، تقوم الدراسة بإجراء مراجعة ببليومترية لـ 207 منشورات من قاعدة بيانات Web of Science. تسلط المراجعة الضوء على التأثيرات المتعددة الأبعاد للممارسات المرتبطة بأبعاد TBL على أداء الأعمال، بينما تقدم نموذج تأثير TBL على أداء الأعمال. يوفر هذا النموذج رؤى قيمة حول كيفية تطبيق الشركات لمبادئ TBL بشكل فعال لمواجهة التحديات الاجتماعية والبيئية، وتعزيز الابتكار، وتحقيق أداء مستدام على المدى الطويل. تسهم النتائج في تقديم رؤى نظرية وعملية قيمة حول كيفية استفادة المنظمات من مبادئ TBL لتعزيز المرونة والابتكار والأداء في مواجهة التحديات الاجتماعية والبيئية العالمية.

1 المقدمة

مع الأهداف العالمية، والامتثال للوائح، والمساهمة في مستقبل أكثر استدامة، مما يضمن في النهاية نجاحها في عالم مترابط.

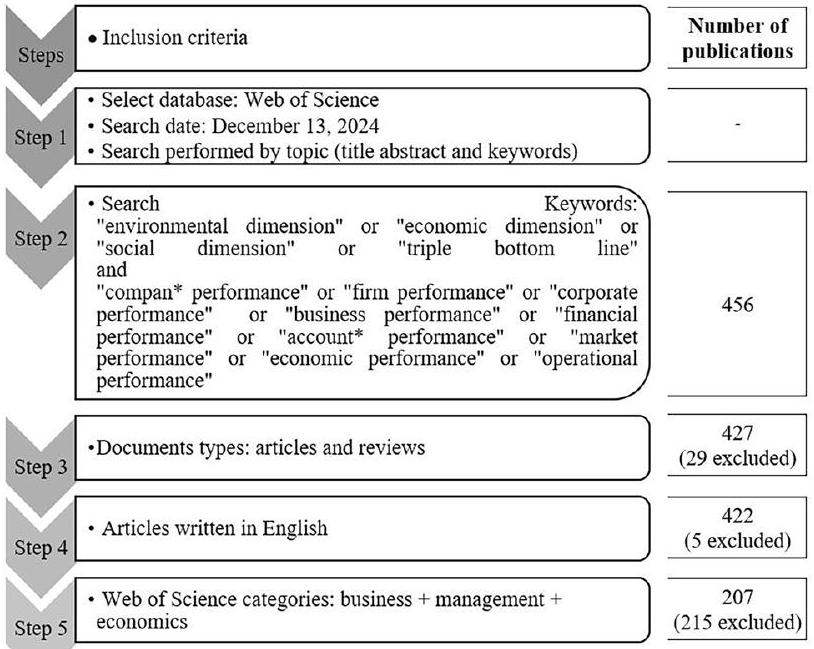

2 المواد والأساليب

2.1 إطار البحث

3 النتائج

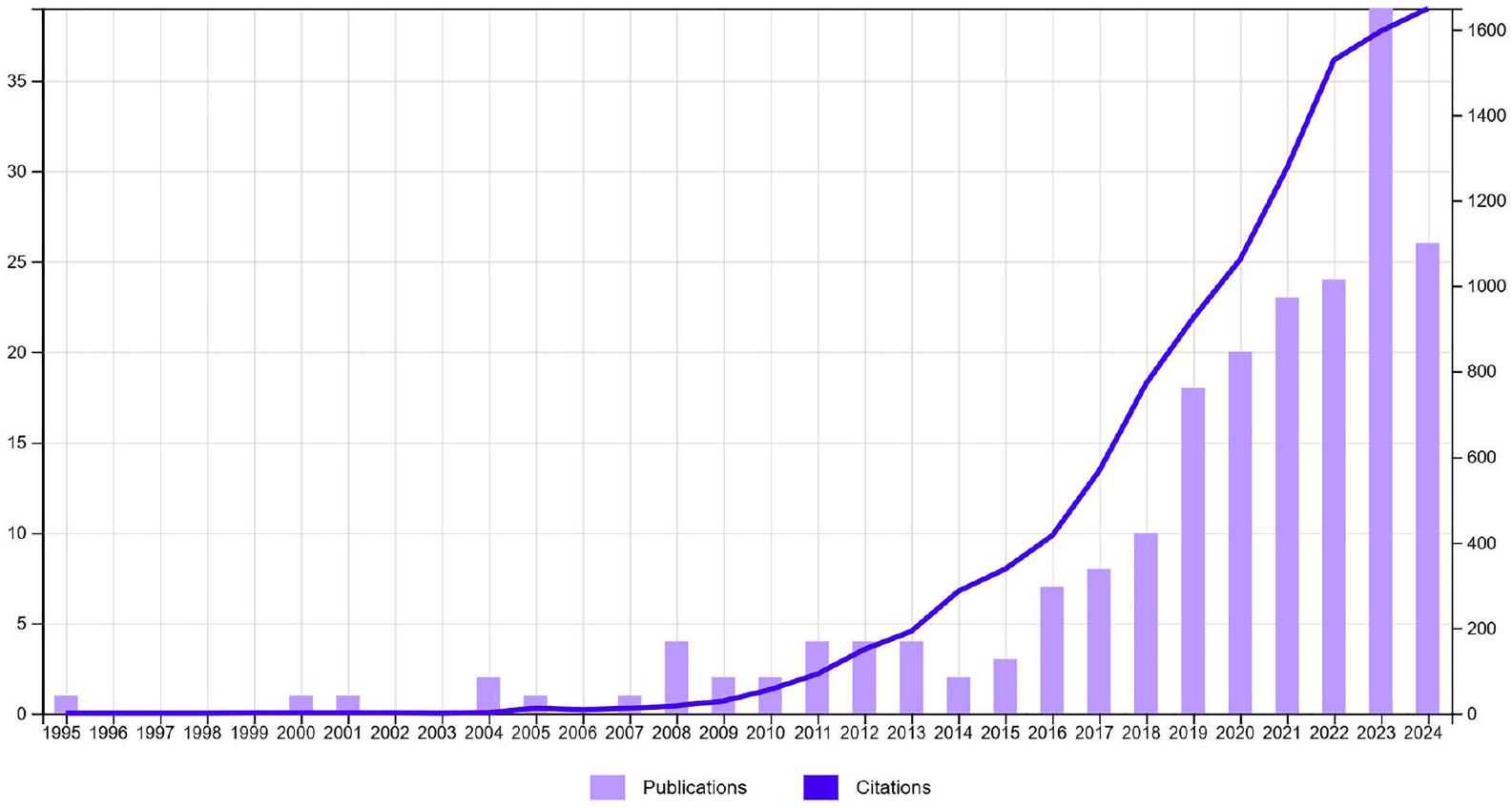

3.1 تطور المنشورات والاستشهادات، المجلات والناشرين

| المجلات | عدد السجلات | % من 198 |

| المسؤولية الاجتماعية للشركات وإدارة البيئة | 17 | 8.21 |

| استراتيجية الأعمال والبيئة | 12 | 5.80 |

| مجلة أخلاقيات الأعمال | 12 | 5.80 |

| مجلة إدارة تكنولوجيا التصنيع | 6 | 2.90 |

| المجلة الدولية لإدارة الإنتاج والعمليات | 5 | 2.53 |

| المجلة الدولية لإدارة الإنتاج والأداء | 5 | 2.42 |

| إدارة الأعمال كوجنت | 4 | 1.93 |

| إدارة التسويق الصناعي | 4 | 1.93 |

| المجلة الدولية لإدارة اللوجستيات | 4 | 1.93 |

| المجلة الدولية لإدارة اللوجستيات والتوزيع الفيزيائي | 4 | 1.93 |

| مجلة أبحاث الأعمال | 4 | 1.93 |

| مجلة إدارة المحاسبة المستدامة والسياسات | 4 | 1.93 |

| الناشرون | عدد السجلات | % من 207 |

| مجموعة إيميرالد للنشر | 74 | 35.75 |

| وايلي | 35 | 16.91 |

| إلسفير | 23 | 11.11 |

| سبرينجر ناتشر | 17 | 8.21 |

| تايلور وفرانسيس | 14 | 6.76 |

3.2 تحليل مقارن مع المراجعات الحالية

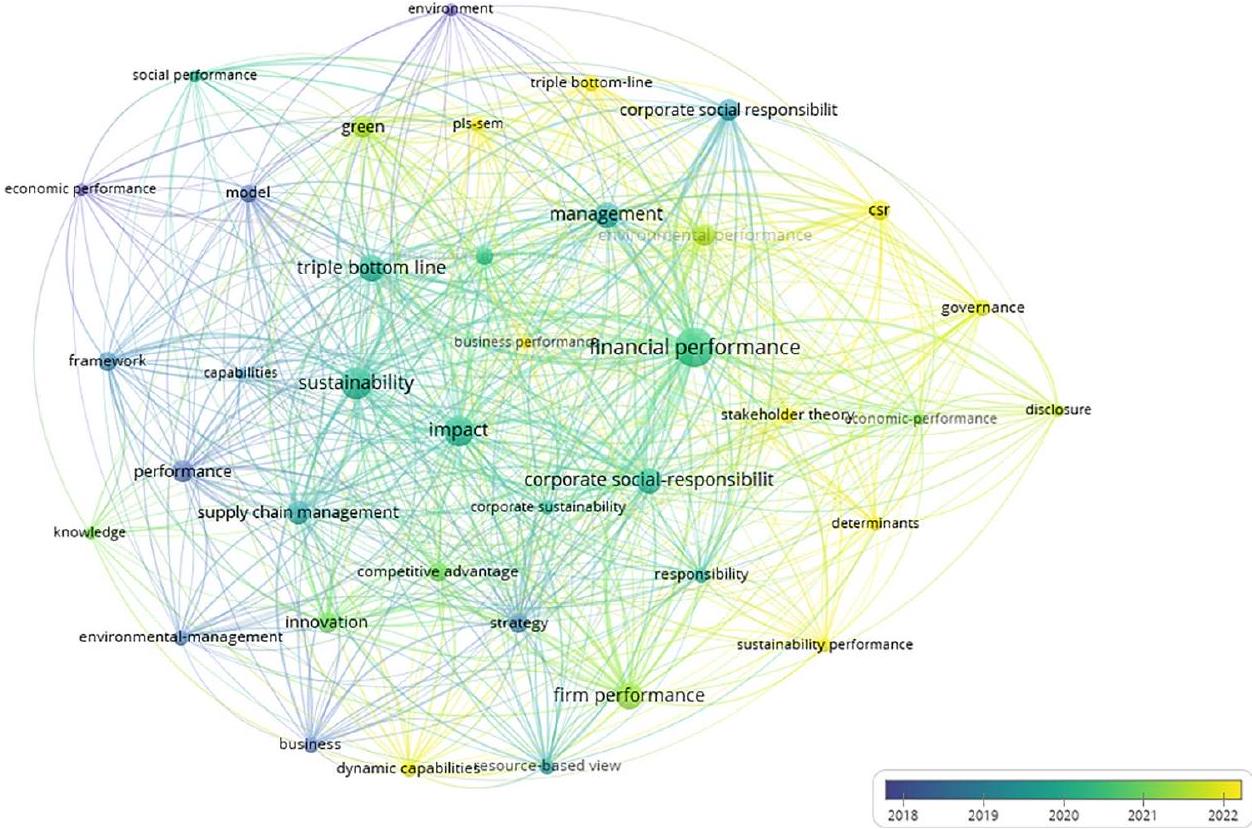

3.3 تحليل التزامن

| المؤلفون | عنوان المقال | الموضوع |

| باترا وآخرون، (2024) [66] | ممارسات الاقتصاد الدائري في تمويل سلسلة التوريد: مراجعة حديثة | مراجعة للأدبيات حول ممارسات الاقتصاد الدائري في تمويل سلسلة التوريد باستخدام طرق تحليل بيبليومترية وشبكية |

| سينغ، (2024) [65] | عقد من استراتيجية العمليات: قضايا البحث واتجاهات البحث المستقبلية | تحليل بيبليومتري منهجي للأدبيات حول استراتيجية العمليات لاستكشاف دورها في تعزيز الميزة التنافسية |

| تومماسيتّي وآخرون، (2023) [67] | المحاسبة البيئية في القطاع العام: مراجعة أدبية منهجية | مراجعة أدبية منهجية تحلل الحالة الحالية والتطورات في المحاسبة البيئية ضمن القطاع العام |

| فهم ومهدي، (2023) [68] | الائتمان التجاري الأخضر وأداء الشركات المستدام خلال COVID-19: مراجعة مفاهيمية | تدرس هذه الدراسة العلاقة بين طلب الائتمان التجاري وأداء الشركات المستدام من خلال الائتمان الأخضر باستخدام نظرية الرؤية المعتمدة على الموارد |

| كوارتيغ وآخرون (2023) [69] | تأثير آليات المجلس على أداء الاستدامة للشركات المدرجة في أفريقيا جنوب الصحراء | تم تطبيق طريقة عامة من خطوتين للتحقيق في كيفية تأثير خصائص المجلس المختلفة على أداء الاستدامة |

| فاروق وآخرون. (2021) [70] | أساسيات المسؤولية الاجتماعية للشركات من المستوى الكلي إلى الجزئي والتقدم في نظرية الخط السفلي الثلاثي | تدمج هذه الدراسة المفاهيم الأساسية الرئيسية للمسؤولية الاجتماعية للشركات مع نظرية الخط السفلي الثلاثي |

| أرسلان، (2020) [71] | الاستدامة الاجتماعية للشركات في إدارة سلسلة التوريد: مراجعة أدبية | مراجعة أدبية تستخدم التحليل الموضوعي لفحص الاستدامة الاجتماعية في سياق إدارة سلسلة التوريد |

| دزينغيز ونيستين، (2020) [72] | الكفاءات من أجل الاستدامة البيئية: مراجعة منهجية حول تأثير القدرة الاستيعابية والقدرات | مراجعة أدبية منهجية تفحص الكفاءات البيئية، التي تعرف بأنها مهارات الإدارة المسؤولة التي تركز على تعزيز الاستدامة البيئية |

| كوبيا-مونتيلا وآخرون (2020) [73] | ما لا تكشفه الشركات عن سياستها البيئية وما قد تفعله الضغوط المؤسسية لاحترام ذلك | دراسة تجريبية تركز على أكبر 500 شركة في العالم في عام 2015، بناءً على تصنيف فورتشن جلوبال 500 |

| يون وHY (2019) [74] | التفاعلات في إدارة سلسلة التوريد المستدامة: مراجعة إطار عمل | مراجعة أدبية منهجية تحلل المقالات من 13 مجلة رائدة في إدارة سلسلة التوريد نشرت بين 2010 و2016 |

| كارتر وآخرون. (2019) [75] | إدارة سلسلة التوريد المستدامة: التطور المستمر والاتجاهات المستقبلية | مراجعة منهجية تحدث كارتر وإيستون (2011) من خلال تحليل أدبيات إدارة سلسلة التوريد المستدامة من المجلات الرائدة في اللوجستيات وسلاسل التوريد التي نشرت بين 2010 و2018 |

| ياوار وسورينغ، (2017) [76] | إدارة القضايا الاجتماعية في سلاسل التوريد: مراجعة أدبية تستكشف القضايا الاجتماعية، والإجراءات، ونتائج الأداء | مراجعة أدبية منظمة تفحص التحديات الاجتماعية ضمن أنظمة سلسلة التوريد |

| تشوجاني وآخرون. (2017) [77] | التحقيق في الأثر البيئي للين، سيغما، واللين سيغما | مراجعة أدبية منهجية تفحص الجوانب البيئية المرتبطة بأساليب اللين، سيغما، واللين سيغما |

| شو وغورصوي، (2015) [78] | إطار عمل مفاهيمي لإدارة سلسلة التوريد المستدامة في الضيافة | إطار عمل سلسلة التوريد في الضيافة مستند إلى أدبيات الاستدامة، مع التركيز على الممارسات البيئية والاجتماعية والاقتصادية المتوافقة مع مبادئ الخط السفلي الثلاثي |

3.4 تحليل العنقود

3.4.1 تم تحديد العناقيد على النحو التالي

4 مناقشة

4.1 مناقشة العنقود

4.1.1 العنقود 1 – وجهات نظر وتطبيقات الخط السفلي الثلاثي في عمليات الأعمال

4.1.2 المجموعة 2 – ممارسات الأعمال المستدامة وتعزيز الأداء

المشتريات، ممارسات سلسلة التوريد المستدامة، والتوجه البيئي للشركات في تحسين الكفاءة التشغيلية، الالتزام الاجتماعي، والأداء المالي. تؤكد هذه الاستراتيجيات المترابطة على أهمية نهج شامل لتحقيق النجاح التنظيمي والقدرة التنافسية على المدى الطويل. يجادل أردا وآخرون [100] بأن ممارسات إدارة البيئة تعمل كوسائط تؤثر بشكل إيجابي على الأداء التشغيلي والاجتماعي والمالي، مما يبرز أهميتها في تحقيق الاستدامة والنجاح المالي.

4.1.3 العنقود 3 – استغلال الاستدامة الاستراتيجية لتعظيم الإمكانيات التنظيمية

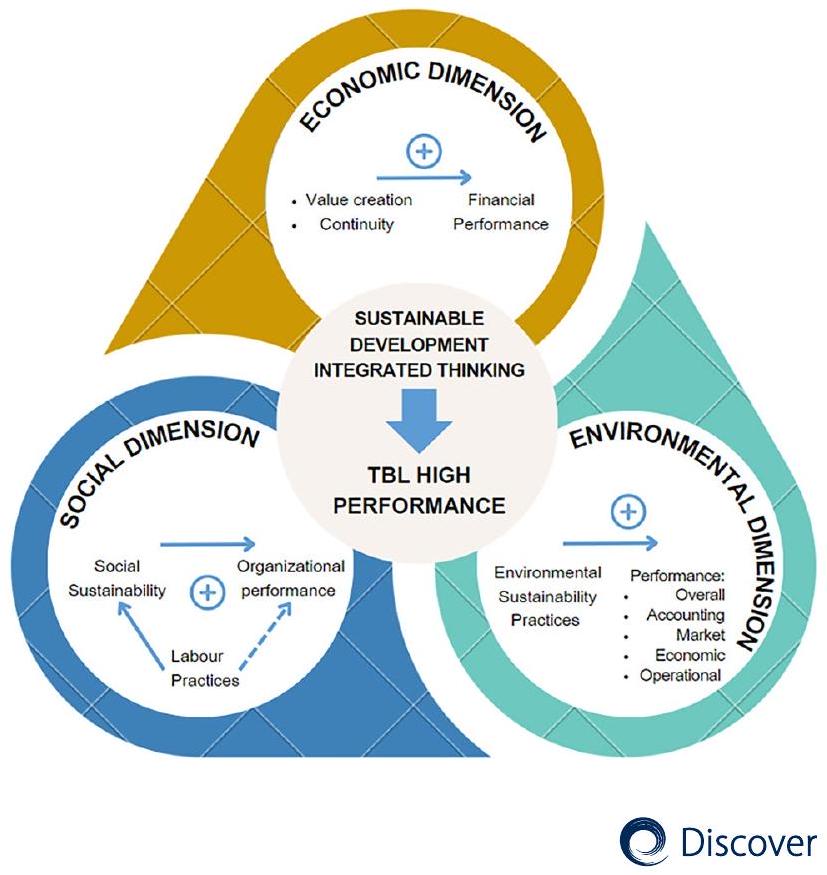

4.2 بناء النموذج

4.3 الآثار

4.3.1 الآثار النظرية

4.3.2 التداعيات العملية

تدمج بشكل متزايد الأدوات الرقمية، والتحليلات المتقدمة، والذكاء الاصطناعي، والتقنيات الذكية لمعالجة التحديات الاجتماعية والبيئية. توفر هذه التكاملات فرصاً لتحسين استخدام الموارد، وزيادة الكفاءة التشغيلية، وتنفيذ استراتيجيات مبتكرة تتماشى مع مبادئ TBL.

4.3.3 التداعيات السياسية

5 استنتاجات

توفر البيانات لم يتم إنشاء أو تحليل أي مجموعات بيانات خلال الدراسة الحالية.

الإعلانات

References

- Cooke FL, Dickmann M, Parry E. Building sustainable societies through human-centred human resource management: emerging issues and research opportunities. Int J Hum Resour Manag. 2022;33:1-15. https://doi.org/10.1080/09585192.2021.2021732.

- Grum DK, Babnik K. The psychological concept of social sustainability in the workplace from the perspective of sustainable goals: a systematic review. Front Psychol. 2022. https://doi.org/10.3389/fpsyg.2022.942204.

- Liu W, Chen X. Natural resources commodity prices volatility and economic uncertainty: evaluating the role of oil and gas rents in COVID19. Resour Policy. 2022. https://doi.org/10.1016/j.resourpol.2021.102338.

- Chofreh AG, Goni FA, Klemeš JJ, et al. Covid-19 shock: development of strategic management framework for global energy. Renew Sustain Energy Rev. 2021. https://doi.org/10.1016/j.rser.2020.110643.

- Larran Jorge M, Herrera Madueno J, Martinez-Martinez D, Lechuga Sancho MP. Competitiveness and environmental performance in Spanish small and medium enterprises: is there a direct link? J Clean Prod. 2015;101:26-37. https://doi.org/10.1016/j.jclepro.2015.04. 016.

- Ammer MA, Aliedan MM, Alyahya MA. Do corporate environmental sustainability practices influence firm value? the role of independent directors: Evidence from Saudi Arabia. Sustainability. 2020;12:1-21. https://doi.org/10.3390/su12229768.

- Mitra S. An exploratory study of sustainability and firm performance for Indian manufacturing small and medium enterprises. J Clean Prod. 2022;371: 133705. https://doi.org/10.1016/j.jclepro.2022.133705.

- D’Souza C, Ahmed T, Khashru MA, et al. The complexity of stakeholder pressures and their influence on social and environmental responsibilities. J Clean Prod. 2022;358: 132038. https://doi.org/10.1016/j.jclepro.2022.132038.

- Subramaniam N, Akbar S, Situ H, et al. Sustainable development goal reporting: contrasting effects of institutional and organisational factors. J Clean Prod. 2023;411: 137339.

- Paruzel A, Schmidt L, Maier GW. Corporate social responsibility and employee innovative behaviors: a meta-analysis. J Clean Prod. 2023;393: 136189. https://doi.org/10.1016/j.jclepro.2023.136189.

- Dhayal KS, Agrawal S, Agrawal R, et al. Green energy innovation initiatives for environmental sustainability: current state and future research directions. Environ Sci Pollut Res. 2024;31:31752-70.

12 Dhayal KS, Giri AK, Esposito L, Agrawal S. Mapping the significance of green venture capital for sustainable development: a systematic review and future research agenda. J Clean Prod. 2023. https://doi.org/10.1016/j.jclepro.2023.136489. - Dhayal KS, Giri AK, Kumar A, et al. Can green finance facilitate industry 5.0 transition to achieve sustainability? a systematic review with future research directions. Environ Sci Pollut Res. 2023;30:102158-80.

- Peng B, Sheng X, Wei G. Does environmental protection promote economic development? from the perspective of coupling coordination between environmental protection and economic development. Environ Sci Pollut Res. 2020;27:39135-48. https://doi.org/10.1007/ s11356-020-09871-1.

- Polcyn J, Us Y, Lyulyov O, et al. Factors influencing the renewable energy consumption in selected European countries. Energies. 2022;15:1-27. https://doi.org/10.3390/en15010108.

16 Chen VZ, Zhong M, Duran P, Sauerwald S. Multistakeholder benefits: a meta-analysis of different theories. Bus Soc. 2022. https://doi.org/ 10.1177/00076503221110181. - Elkington J. Governance for sustainability. Corp Gov. 2006;14:522-9. https://doi.org/10.1111/j.1467-8683.2006.00527.x.

- Elkington J. Cannibals With Forks: The Triple Bottom Line of 21 st Century Business. Oxford, United Kingdom: Capstone Publishing Limited; 1997.

20. Montabon F, Pagell M, Wu ZH. Making sustainability sustainable. J Supply Chain Manag. 2016;52:11-27. https://doi.org/10.1111/jscm. 12103.

22. Hahn T, Pinkse J, Preuss L, Figge F. Tensions in corporate sustainability: towards an integrative framework. J Bus Ethics. 2015;127:297-316. https://doi.org/10.1007/s10551-014-2047-5.

23. Hubbard G. Measuring organizational performance: beyond the triple bottom line. Bus Strateg Environ. 2009;18:177-91. https://doi. org/10.1002/bse.564.

24. Howard M, Bohm S, Eatherley D. Systems resilience and SME multilevel challenges: a place-based conceptualization of the circular economy. J Bus Res. 2022;145:757-68. https://doi.org/10.1016/j.jbusres.2022.03.014.

25. Gu WT, Wang JY. Research on index construction of sustainable entrepreneurship and its impact on economic growth. J Bus Res. 2022;142:266-76. https://doi.org/10.1016/j.jbusres.2021.12.060.

26 Raza A, Alavi AB, Asif L. Sustainability and financial performance in the banking industry of the United Arab Emirates. Disc Sustain. 2024. https://doi.org/10.1007/s43621-024-00414-z.

27. Chabowski BR, Mena JA, Gonzalez-Padron TL. The structure of sustainability research in marketing, 1958-2008: a basis for future research opportunities. J Acad Mark Sci. 2011;39:55-70. https://doi.org/10.1007/s11747-010-0212-7.

28. Kumar G, Goswami M. Sustainable supply chain performance, its practice and impact on barriers to collaboration. Int J Product Perform Manag. 2019;68:1434-56. https://doi.org/10.1108/IJPPM-12-2018-0425.

29. Ferro C, Padin C, Hogevold N, et al. Validating and expanding a framework of a triple bottom line dominant logic for business sustainability through time and across contexts. J Bus Indust Mark. 2019;34:95-116. https://doi.org/10.1108/JBIM-07-2017-0181.

30. He Q, Gallear D, Ghobadian A, Ramanathan R. Managing knowledge in supply chains: a catalyst to triple bottom line sustainability. Prod Plan Contl. 2019;30:448-63. https://doi.org/10.1080/09537287.2018.1501814.

31. Rosli N, Ha NC, Ghazali EM. Bridging the gap between branding and sustainability by fostering brand credibility and brand attachment in travellers’ hotel choice. Bottom Line. 2019;32:308-39. https://doi.org/10.1108/BL-03-2019-0078.

32 Lajnef K, Ellouz S. Nonlinear causality between CSR and firm performance using NARX model: evidence from France. J Sustain Finance Invest. 2022. https://doi.org/10.1080/20430795.2022.2112140.

33. Hammer J, Pivo G. The triple bottom line and sustainable economic development theory and practice. Econ Dev Q. 2017;31:25-36. https://doi.org/10.1177/0891242416674808.

34. Collste D, Pedercini M, Cornell SE. Policy coherence to achieve the SDGs: using integrated simulation models to assess effective policies. Sustain Sci. 2017;12:921-31. https://doi.org/10.1007/s11625-017-0457-x.

35. Nogueira E, Gomes S, Lopes JM. The key to sustainable economic development: a triple bottom line approach. Resources. 2022;11:46. https://doi.org/10.3390/resources11050046.

36. Cupertino S, Vitale G, Taticchi P. Interdependencies between financial and non-financial performances: a holistic and short-term analytical perspective. Int J Product Perform Manag. 2022. https://doi.org/10.1108/IJPPM-02-2022-0075.

37 Alshehhi A, Nobanee H, Khare N. The impact of sustainability practices on corporate financial performance: literature trends and future research potential. Sustainability. 2018. https://doi.org/10.3390/su10020494.

38. Zabolotnyy S, Wasilewski M. The concept of financial sustainability measurement: a case of food companies from Northern Europe. Sustainability. 2019;11:5139. https://doi.org/10.3390/su11185139.

39 Gleißner W, Günther T, Walkshäusl C. Financial sustainability: measurement and empirical evidence. J Bus Econ. 2022. https://doi.org/ 10.1007/s11573-022-01081-0.

40. Li EL, Zhou LX, Wu AQ. The supply-side of environmental sustainability and export performance: the role of knowledge integration and international buyer involvement. Int Bus Rev. 2017;26:724-35. https://doi.org/10.1016/j.ibusrev.2017.01.002.

41. Agyabeng-Mensah Y, Afum E, Ahenkorah E. Exploring financial performance and green logistics management practices: examining the mediating influences of market, environmental and social performances. J Clean Prod. 2020;258: 120613. https://doi.org/10. 1016/j.jclepro.2020.120613.

42. Agyabeng-Mensah Y, Ahenkorah E, Afum E, Owusu D. The influence of lean management and environmental practices on relative competitive quality advantage and performance. J Manuf Technol Manag. 2020;31:1351-72. https://doi.org/10.1108/ JMTM-12-2019-0443.

43. Khan M, Rahman HU, Baloch QB, et al. Is there any difference between the theory and practice for the association between environmental sustainability and firm performance in Pakistan? Bus Strat Dev. 2021;4:371-82. https://doi.org/10.1002/bsd2.164.

44 Malesios C, De D, Moursellas A, et al. Sustainability performance analysis of small and medium sized enterprises: criteria, methods and framework. Socio-Econ Plan Sci. 2021. https://doi.org/10.1016/j.seps.2020.100993.

45. van Emous R, Krušinskas R, Westerman W. Carbon emissions reduction and corporate financial performance: the influence of countrylevel characteristics. Energies. 2021;14:6029. https://doi.org/10.3390/en14196029.

46. Nogueira E, Gomes S, Lopes JM. Triple bottom line, sustainability, and economic development: what binds them together? A Bibliometric Appr Sustain. 2023;15:6706. https://doi.org/10.3390/su15086706.

47. Karman A, Prokop V, Giglio C, Rehman FU. Has the Covid-19 pandemic jeopardized firms’ environmental behavior Bridging green initiatives and firm value through the triple bottom line approach. Corporate Soc Respons Environ Manag. 2023. https://doi.org/10.1002/csr. 2575.

48. Tate WL, Bals L. Achieving shared triple bottom line (TBL) value creation: toward a social resource-based view (SRBV) of the firm. J Bus Ethics. 2018;152:803-26. https://doi.org/10.1007/s10551-016-3344-y.

49. Mair J, Martí I. Social entrepreneurship research: a source of explanation, prediction, and delight. J World Bus. 2006;41:36-44. https:// doi.org/10.1016/j.jwb.2005.09.002.

50. Murphy PJ, Coombes SM. A model of social entrepreneurial discovery. J Bus Ethics. 2009;87:325-36. https://doi.org/10.1007/ s10551-008-9921-y.

51. Certo ST, MillerT. Social entrepreneurship: key issues and concepts. Bus Horiz. 2008;51:267-71. https://doi.org/10.1016/j.bushor.2008. 02.009.

52. Narangajavana Y, Gonzalez-Cruz T, Garrigos-Simon FJ, Cruz-Ros S. Measuring social entrepreneurship and social value with leakage. definition, analysis and policies for the hospitality industry. Int Entre Manag J. 2016;12:911-34. https://doi.org/10.1007/s11365-016-0396-5.

53. Fetrati MA, Hansen D, Akhavan P. How to manage creativity in organizations: connecting the literature on organizational creativity through bibliometric research. Technovation. 2022;115: 102473. https://doi.org/10.1016/j.technovation.2022.102473.

54. Ajmal MM, Khan M, Hussain M, Helo P. Conceptualizing and incorporating social sustainability in the business world. Int J Sust Dev World. 2018;25:327-39. https://doi.org/10.1080/13504509.2017.1408714.

55 Nogueira E, Gomes S, Lopes JM. The contribution of the labour practices to organizational performance: the mediating role of social sustainability. Bus Ethics Environ Respons. 2024. https://doi.org/10.1111/beer.12682.

56. Zupic I, Čater T. Bibliometric methods in management and organization. Organ Res Methods. 2015;18:429-72. https://doi.org/10.1177/ 1094428114562629.

57. Milojevic S, Sugimoto CR, Yan EJ, Ding Y. The cognitive structure of library and information science: analysis of article title words. J Am Soc Inform Sci Technol. 2011;62:1933-53. https://doi.org/10.1002/asi.21602.

58. Zhi W, Yuan L, Ji GD, et al. A bibliometric review on carbon cycling research during 1993-2013. Environ Earth Sci. 2015;74:6065-75. https://doi.org/10.1007/s12665-015-4629-7.

59. Liu Z, Yin Y, Liu W, Dunford M. Visualizing the intellectual structure and evolution of innovation systems research: a bibliometric analysis. Scientometrics. 2015;103:135-58. https://doi.org/10.1007/s11192-014-1517-y.

60. Franceschini S, Faria LGD, Jurowetzki R. Unveiling scientific communities about sustainability and innovation. a bibliometric journey around sustainable terms. J Clean Prod. 2016;127:72-83. https://doi.org/10.1016/j.jclepro.2016.03.142.

61. Lopes JM, Laurett R, Antunes H, Oliveira J. Entrepreneurial marketing: a bibliometric analysis of the second decade of the 21st century and future agenda. J Res Mark Entrep. 2021;23:295-317. https://doi.org/10.1108/JRME-02-2019-0019.

62. Lopes JM, Gomes S, Durão M, Pacheco R. The holy grail of luxury tourism: a holistic bibliometric overview. J Qual Assur Hosp Tour. 2022. https://doi.org/10.1080/1528008X.2022.2089946.

63. Thirumaran K, Jang HJ, Pourabedin Z, Wood J. The role of social media in the luxury tourism business: a research review and trajectory assessment. Sustainability. 2021;13:1-13. https://doi.org/10.3390/su13031216.

64. Ay I, Sc S. Developing a green business portfolio. Long Range Plan. 1995;28:29-38. https://doi.org/10.1016/0024-6301(95)98587-I.

65. Singh A. A decade of operations strategy: research issues and future research directions. Compet Rev. 2024. https://doi.org/10.1108/ CR-06-2024-0116.

66. Patra SP, Wankhede VA, Agrawal R. Circular economy practices in supply chain finance: a state-of-the-art review. Benchmarking: An Int J. 2024. https://doi.org/10.1108/BIJ-10-2022-0627.

67. Tommasetti A, Maione G, Bignardi A, Lentini P. Environmental accounting in the public sector: a systematic literature review. Int J Bus Environ. 2023;14:164-82. https://doi.org/10.1504/IJBE.2023.129907.

68. Fahim F, Mahadi B. Green trade credit and sustainable firm performances during COVID-19: a conceptual review. Vision- J Bus Perspect. 2023;27:593-603. https://doi.org/10.1177/09722629221096050.

69 Kwarteng P, Appiah KO, Addai B. Influence of board mechanisms on sustainability performance for listed firms in Sub-Saharan Africa. Future Bus J. 2023. https://doi.org/10.1186/s43093-023-00258-5.

70. Farooq Q, Fu PH, Liu X, Hao YH. Basics of macro to microlevel corporate social responsibility and advancement in triple bottom line theory. Corp Soc Responsib Environ Manag. 2021;28:969-79. https://doi.org/10.1002/csr.2069.

71. Arslan M. Corporate social sustainability in supply chain management: a literature review. J Global Respons. 2020;11:233-55. https:// doi.org/10.1108/JGR-11-2019-0108.

72. Dzhengiz T, Niesten E. Competences for environmental sustainability: a systematic review on the impact of absorptive capacity and capabilities. J Bus Ethics. 2020;162:881-906. https://doi.org/10.1007/s10551-019-04360-z.

73. Isabel Cubilla-Montilla M, Galindo-Villardon P, Belen Nieto-Librero A, et al. What companies do not disclose about their environmental policy and what institutional pressures may do to respect. Corp Soc Responsib Environ Manag. 2020;27:1181-97. https://doi.org/10. 1002/csr. 1874.

74. Yun G, Yalcin MG, Hales DN, Kwon HY. Interactions in sustainable supply chain management: a framework review. Int J Logist Manag. 2019;30:140-73. https://doi.org/10.1108/IJLM-05-2017-0112.

75. Carter CR, Hatton MR, Wu C, Chen XJ. Sustainable supply chain management: continuing evolution and future directions. Int J Phys Distrib Logist Manag. 2019;50:122-46. https://doi.org/10.1108/IJPDLM-02-2019-0056.

76. Yawar SA, Seuring S. Management of social issues in supply chains: a literature review exploring social issues, actions and performance outcomes. J Bus Ethics. 2017;141:621-43. https://doi.org/10.1007/s10551-015-2719-9.

77. Chugani N, Kumar V, Garza-Reyes JA, et al. Investigating the green impact of Lean, Six Sigma and Lean Six Sigma. Int J Lean Six Sigma. 2017;8:7-32. https://doi.org/10.1108/IJLSS-11-2015-0043.

78. Xu X, Gursoy D. A conceptual framework of sustainable hospitality supply chain management. J Hosp Market Manag. 2015;24:229-59. https://doi.org/10.1080/19368623.2014.909691.

79. Liu RL. A new bibliographic coupling measure with descriptive capability. Scientometrics. 2017;110:915-35. https://doi.org/10.1007/ s11192-016-2196-7.

80. Donthu N, Kumar S, Mukherjee D, et al. How to conduct a bibliometric analysis: an overview and guidelines. J Bus Res. 2021;133:285-96. https://doi.org/10.1016/j.jbusres.2021.04.070.

81 Vhatkar MS, Raut RD, Gokhale R, et al. Leveraging digital technology in retailing business: unboxing synergy between omnichannel retail adoption and sustainable retail performance. J Retail Cons Serv. 2024. https://doi.org/10.1016/j.jretconser.2024.104047.

82. El Akremi A, Gond JP, Swaen V, et al. How do employees perceive corporate responsibility? development and validation of a multidimensional corporate stakeholder responsibility scale. J Manag. 2018;44:619-57. https://doi.org/10.1177/0149206315569311.

83. Grudzien D, Pfutzenreuter T, Galli F, et al. Sustainable strategic operations supported by I4.0 digital technologies. J Indust Integ ManagInnov Entrepreneurship. 2023;08:39-64. https://doi.org/10.1142/S2424862222500270.

84. Wu XD, Amoasi R. The role of CSR in sustaining corporate brands in the global market: the perspective of telecommunication companies in Ghana. Corp Soc Responsib Environ Manag. 2024. https://doi.org/10.1002/csr.2578.

85. Escamilla-Solano S, Fernández-Portillo A, Orden-Cruz C, Sánchez-Escobedo MC. Corporate social responsibility disclosure: mediating effects of the economic dimension on firm performance. Corp Soc Responsib Environ Manag. 2024. https://doi.org/10.1002/csr.2596.

86. Menz KM. Corporate social responsibility: is it rewarded by the corporate bond market? a critical note. J Bus Ethics. 2010;96:117-34. https://doi.org/10.1007/s10551-010-0452-y.

87. Galletta S, Mazzu S, Naciti V, Vermiglio C. Gender diversity and sustainability performance in the banking industry. Corp Soc Responsib Environ Manag. 2022;29:161-74. https://doi.org/10.1002/csr.2191.

88. Dakhli A. Do women on corporate boardrooms have an impact on tax avoidance? the mediating role of corporate social responsibility. Corporate Governance- Int J Bus Soc. 2022;22:821-45. https://doi.org/10.1108/CG-07-2021-0265.

89. Menicucci E, Paolucci G. Board gender equality and ESG performance. evidence from European banking sector. Corporate GovernanceInt J Bus Soc. 2024;24:147-74. https://doi.org/10.1108/CG-04-2023-0146.

90. Zubeltzu-Jaka E, Alvarez-Etxeberria I, Aldaz-Odriozola M. Corporate social responsibility oriented boards and triple bottom line performance: a meta-analytic study. Business Strategy and Development. 2024. https://doi.org/10.1002/bsd2.320.

91. Rath C, Tripathy A, Mangla SK. How the social dimension of ESG influences CEO compensation: role of CEO and board characteristics. Bus Strateg Environ. 2024. https://doi.org/10.1002/bse.4008.

92. Lu J, Rodenburg K, Foti L, Pegoraro A. Are firms with better sustainability performance more resilient during crises? Bus Strateg Environ. 2022;31:1-17. https://doi.org/10.1002/bse.3088.

93. Turker D, Ozmen YS. Understanding how social responsibility drives social innovation: characteristics of radically innovative projects. Eur J Innov Manag. 2022;25:680-702. https://doi.org/10.1108/EJIM-08-2020-0314.

94. Nagiah GR, Suki NM. Linking environmental sustainability, social sustainability, corporate reputation and the business performance of energy companies: insights from an emerging market. Int J Energy Sect Manage. 2024;18:1905-22. https://doi.org/10.1108/ IJESM-06-2023-0003.

95. Vargas-Santander KG, Alvarez-Diez S, Baixauli-Soler S, Belda-Ruiz M. Corporate social responsibility and financial performance: does country sustainability matter? Corp Soc Responsib Environ Manag. 2023;30:3075-94. https://doi.org/10.1002/csr.2539.

96 Jaiwani M, Gopalkrishnan S. Do private and public sector banks respond to ESG in the same way? some evidences from India. Bench-marking-An Int J. 2023. https://doi.org/10.1108/BIJ-05-2023-0340.

97. Alcouffe S , Boitier M, Jabot R. An integrated literature review on the adoption and diffusion of multicapital accounting innovations. Sustain Account Manag Policy J. 2024. https://doi.org/10.1108/SAMPJ-12-2023-0912.

98. de Pilla LHL, Peci A, Leite RD. Is the state a socially responsible shareholder? state-owned enterprises, political ideology, and corporate social performance. J Bus Ethics. 2024. https://doi.org/10.1007/s10551-024-05751-7.

99 Avelar S, Borges-Tiago T, Almeida A, Tiago F. Confluence of sustainable entrepreneurship, innovation, and digitalization in SMEs. J Busi Res. 2024. https://doi.org/10.1016/j.jbusres.2023.114346.

100. Arda OA, Montabon F, Tatoglu E, et al. Toward a holistic understanding of sustainability in corporations: resource-based view of sustainable supply chain management. Supply Chain Manag. 2023;28:193-208. https://doi.org/10.1108/SCM-08-2021-0385.

101. Tran T, Kim S, Son BG, Ramkumar M. Paradoxical association between lean manufacturing sustainability practices and triple bottom line performance. IEEE Trans Eng Manag. 2023. https://doi.org/10.1109/TEM.2023.3290724.

102. Khan SAR, Yu Z, Umar M, Tanveer M. Green capabilities and green purchasing practices: a strategy striving towards sustainable operations. Bus Strateg Environ. 2022;31:1719-29. https://doi.org/10.1002/bse.2979.

103. Saglam YC. Analyzing sustainable reverse logistics capability and triple bottom line: the mediating role of sustainability culture. J Manuf Technol Manag. 2023;34:1162-82. https://doi.org/10.1108/JMTM-01-2023-0009.

104. De Giovanni P. Do internal and external environmental management contribute to the triple bottom line? Int J Oper Prod Manag. 2012;32:265-90. https://doi.org/10.1108/01443571211212574.

105. Ahmad F, Khokhar SG. Examining the impact of sustainable supply chain management practices and supply chain ambidexterity on sustainability performance. Operat Supply Chain Manag-An Int J. 2024;17:179-90.

106. Carter CR, Easton PL. Sustainable supply chain management: evolution and future directions. Int J Phys Distrib Logist Manag. 2011;41:4662. https://doi.org/10.1108/09600031111101420.

107. Oubrahim I, Sefiani N. An integrated multi-criteria decision-making approach for sustainable supply chain performance evaluation from a manufacturing perspective. Int J Product Perform Manag. 2024. https://doi.org/10.1108/IJPPM-09-2023-0464.

108. Morgan YC, Fok L, Zee S. Examining the impact of environmental and organizational priorities on sustainability performance in service industries. Int J Product Perform Manag. 2023. https://doi.org/10.1108/IJPPM-02-2023-0053.

109 Nogueira E, Gomes S, Lopes JM. A meta-regression analysis of environmental sustainability practices and firm performance. J Clean Produ. 2023. https://doi.org/10.1016/j.jclepro.2023.139048.

110. Ertz M, Latrous I, Dakhlaoui A, Sun SH. The impact of big data analytics on firm sustainable performance. Corp Soc Responsib Environ Manag. 2024. https://doi.org/10.1002/csr.2990.

111. Li Y, Li JY, Zhai YF. Intellectual capital and sustainability performance: the mediating role of digitalization. J Intellect Cap. 2024;25:867-90. https://doi.org/10.1108/JIC-06-2023-0129.

112. Huang SS, Wang XQ, Qu H. Impact of perceived corporate social responsibility on peer-to-peer accommodation consumers’ repurchase intention and switching intention. J Hosp Market Manag. 2023;32:893-916. https://doi.org/10.1080/19368623.2023.2214549.

113. Carter CR, Rogers DS. A framework of sustainable supply chain management: moving toward new theory. Int J Phys Distrib Logist Manag. 2008;38:360-87. https://doi.org/10.1108/09600030810882816.

114. Torugsa NA, O’Donohue W, Hecker R. Proactive CSR: An empirical analysis of the role of its economic, social and environmental dimensions on the association between capabilities and performance. J Bus Ethics. 2013;115:383-402. https://doi.org/10.1007/s10551-012-1405-4.

115. Coelho A, Ferreira J, Proença C. The impact of green entrepreneurial orientation on sustainability performance through the effects of green product and process innovation: the moderating role of ambidexterity. Bus Strateg Environ. 2024. https://doi.org/10.1002/bse. 3648.

116. González-Ramos MI, Donate MJ, Guadamillas F. The relationship between knowledge management strategies and corporate social responsibility: effects on innovation capabilities. Technol Forecast Soc Chang. 2023;188: 122287. https://doi.org/10.1016/j.techfore. 2022.122287.

117. Lee MJ, Pak A, Roh T. The interplay of institutional pressures, digitalization capability, environmental, social, and governance strategy, and triple bottom line performance: a moderated mediation model. Bus Strategy Environ. 2024;33:5247-68. https://doi.org/10.1002/ bse. 3755.

118. Marzouk J, El Ebrashi R. The interplay among green absorptive capacity, green entrepreneurial, and learning orientations and their effect on triple bottom line performance. Bus Strateg Environ. 2024. https://doi.org/10.1002/bse.3588.

119 Nogueira E, Gomes S, Lopes JM. Financial sustainability: exploring the influence of the triple bottom line economic dimension on firm performance. Sustainability. 2024. https://doi.org/10.3390/su16156458.

- Elisabete Nogueira, elisabete.s.nogueira@gmail.com; Sofia Gomes, sofiag@upt.pt; João M. Lopes, joao.lopes.1987@gmail.com |

¹Research on Economics, Management and Information Technologies, REMIT, Portucalense University, Rua Dr. António Bernardino Almeida, 541-619, 4200-072 Porto, Portugal.Instituto Superior Miguel Torga, Coimbra, Portugal & NECE-UBI – Research Unit in Business Sciences, University of Beira Interior, Covilhã, Portugal.

DOI: https://doi.org/10.1007/s43621-025-00804-x

Publication Date: 2025-01-21

Review

Unveiling triple bottom line’s influence on business performance

Published online: 21 January 2025

© The Author(s) 2025 OPEN

Abstract

Addressing environmental, social, and economic challenges has become a pressing global priority. The Triple Bottom Line (TBL) framework offers a holistic approach for evaluating corporate performance by integrating economic, environmental, and social perspectives. Despite its increasing adoption in both managerial and academic research, there remains a significant gap in understanding how the TBL framework influences business performance. To address this, the study conducts a bibliometric review of 207 publications from the Web of Science database. The review highlights the multifaceted impact of practices linked to the TBL dimensions on business performance while introducing the TBL Influence on Business Performance model. This model provides valuable insights into how businesses can effectively apply TBL principles to address socio-environmental challenges, foster innovation, and achieve sustained long-term performance. The findings contribute valuable theoretical and practical insights into how organizations can utilize TBL principles to strengthen resilience, innovation, and performance in the face of global socio-environmental challenges.

1 Introduction

with global goals, comply with regulations, and contribute to a more sustainable future, ultimately ensuring their own success in an interconnected world.

2 Materials and methods

2.1 Research framework

3 Results

3.1 Evolution of publications and citations, journals and publishers

| Journals | Record Count | % of 198 |

| Corporate social responsibility and environmental management | 17 | 8.21 |

| Business strategy and the environment | 12 | 5.80 |

| Journal of business ethics | 12 | 5.80 |

| Journal of manufacturing technology management | 6 | 2.90 |

| International journal of operations production management | 5 | 2.53 |

| International journal of productivity and performance management | 5 | 2.42 |

| Cogent business management | 4 | 1.93 |

| Industrial marketing management | 4 | 1.93 |

| International journal of logistics management | 4 | 1.93 |

| International journal of physical distribution logistics management | 4 | 1.93 |

| Journal of business research | 4 | 1.93 |

| Sustainability accounting management and policy journal | 4 | 1.93 |

| Publishers | Record Count | % of 207 |

| Emerald group publishing | 74 | 35.75 |

| Wiley | 35 | 16.91 |

| Elsevier | 23 | 11.11 |

| Springer nature | 17 | 8.21 |

| Taylor & francis | 14 | 6.76 |

3.2 Comparative analysis with existing reviews

3.3 Co-occurrence analysis

| Authors | Article title | Subject |

| Patra et al., (2024) [66] | Circular economy practices in supply chain finance: a state-of-the-art review | A review of literature on circular economy practices in supply chain finance employing bibliometric and network analysis methods |

| Singh, (2024) [65] | A decade of operations strategy: research issues and future research directions | A systematic bibliometric analysis of the literature on operations strategy to explore its role in driving competitive advantage |

| Tommasetti et al., (2023) [67] | Environmental accounting in the public sector: a systematic literature review | Systematic literature review analyzing the current state and developments in environmental accounting within the public sector |

| Fahim and Mahadi, (2023) [68] | Green Trade Credit and Sustainable Firm Performances During COVID-19: A Conceptual Review | This study examines the relationship between trade credit demand and sustainable firm performance through green credit using the ResourceBased View theory |

| Kwarteng et al. (2023) [69] | Influence of board mechanisms on sustainability performance for listed firms in Sub-Saharan Africa | A two-step system generalized method of moments approach is applied to investigate how various board characteristics influence sustainability performance |

| Farooq et al. (2021) [70] | Basics of macro to microlevel corporate social responsibility and advancement in triple bottom line theory | This research integrates key foundational CSR concepts with TBL theory |

| Arslan, (2020) [71] | Corporate social sustainability in supply chain management: a literature review | Literature review utilizing thematic analysis to examine social sustainability within the context of supply chain management |

| Dzhengiz & Niesten, (2020) [72] | Competences for Environmental Sustainability: A Systematic Review on the Impact of Absorptive Capacity and Capabilities | Systematic literature review examining environmental competences, defined as responsible management skills focused on enhancing environmental sustainability |

| Cubilla-Montilla et al. (2020) [73] | What companies do not disclose about their environmental policy and what institutional pressures may do to respect | Empirical study focused on the world’s 500 largest companies in 2015, based on the Fortune Global 500 ranking |

| Yun and HY (2019) [74] | Interactions in sustainable supply chain management: a framework review | Systematic literature review analyzing articles from 13 leading supply chain management journals published between 2010 and 2016 |

| Carter et al. (2019) [75] | Sustainable supply chain management: continuing evolution and future directions | Systematic review updating Carter and Easton (2011) by analyzing sustainable supply chain management literature from leading logistics and supply chain journals published between 2010 and 2018 |

| Yawar and Seuring, (2017) [76] | Management of Social Issues in Supply Chains: A Literature Review Exploring Social Issues, Actions and Performance Outcomes | Structured literature review examining social challenges within supply chain systems |

| Chugani et al. (2017) [77] | Investigating the green impact of Lean, Six Sigma and Lean Six Sigma | Systematic literature review examining the environmental aspects linked to Lean, Six Sigma, and Lean Six Sigma methodologies |

| Xu and Gursoy, (2015) [78] | A Conceptual Framework of Sustainable Hospitality Supply Chain Management | Hospitality supply chain framework grounded in sustainability literature, emphasizing environmental, social, and economic practices aligned with triple bottom line principles |

3.4 Cluster analysis

3.4.1 The clusters were delineated as follows

4 Discussion

4.1 Cluster discussion

4.1.1 Cluster 1-perspectives and applications of TBL in business operations

4.1.2 Cluster 2-sustainable business practices and performance enhancements

procurement, sustainable supply chain practices, and corporate environmental orientation in improving operational efficiency, social commitment, and financial performance. These interconnected strategies emphasize the importance of a holistic approach to achieving long-term organizational success and competitiveness. Arda et al. [100] argue that environmental management practices serve as mediators that positively impact operational, social, and financial performance, underscoring their importance in achieving sustainability and financial success.

4.1.3 Cluster 3-leveraging strategic sustainability to maximize organizational potential

4.2 Building the model

4.3 Implications

4.3.1 Theoretical Implications

4.3.2 Practical implications

increasingly integrating digital tools, advanced analytics, artificial intelligence, and smart technologies to address socio-environmental challenges. This integration provides opportunities to optimize resource use, improve operational efficiency, and implement innovative strategies aligned with TBL principles.

4.3.3 Policy implications

5 Conclusions

Data availability No datasets were generated or analysed during the current study.

Declarations

References

- Cooke FL, Dickmann M, Parry E. Building sustainable societies through human-centred human resource management: emerging issues and research opportunities. Int J Hum Resour Manag. 2022;33:1-15. https://doi.org/10.1080/09585192.2021.2021732.

- Grum DK, Babnik K. The psychological concept of social sustainability in the workplace from the perspective of sustainable goals: a systematic review. Front Psychol. 2022. https://doi.org/10.3389/fpsyg.2022.942204.

- Liu W, Chen X. Natural resources commodity prices volatility and economic uncertainty: evaluating the role of oil and gas rents in COVID19. Resour Policy. 2022. https://doi.org/10.1016/j.resourpol.2021.102338.

- Chofreh AG, Goni FA, Klemeš JJ, et al. Covid-19 shock: development of strategic management framework for global energy. Renew Sustain Energy Rev. 2021. https://doi.org/10.1016/j.rser.2020.110643.

- Larran Jorge M, Herrera Madueno J, Martinez-Martinez D, Lechuga Sancho MP. Competitiveness and environmental performance in Spanish small and medium enterprises: is there a direct link? J Clean Prod. 2015;101:26-37. https://doi.org/10.1016/j.jclepro.2015.04. 016.

- Ammer MA, Aliedan MM, Alyahya MA. Do corporate environmental sustainability practices influence firm value? the role of independent directors: Evidence from Saudi Arabia. Sustainability. 2020;12:1-21. https://doi.org/10.3390/su12229768.

- Mitra S. An exploratory study of sustainability and firm performance for Indian manufacturing small and medium enterprises. J Clean Prod. 2022;371: 133705. https://doi.org/10.1016/j.jclepro.2022.133705.

- D’Souza C, Ahmed T, Khashru MA, et al. The complexity of stakeholder pressures and their influence on social and environmental responsibilities. J Clean Prod. 2022;358: 132038. https://doi.org/10.1016/j.jclepro.2022.132038.

- Subramaniam N, Akbar S, Situ H, et al. Sustainable development goal reporting: contrasting effects of institutional and organisational factors. J Clean Prod. 2023;411: 137339.

- Paruzel A, Schmidt L, Maier GW. Corporate social responsibility and employee innovative behaviors: a meta-analysis. J Clean Prod. 2023;393: 136189. https://doi.org/10.1016/j.jclepro.2023.136189.

- Dhayal KS, Agrawal S, Agrawal R, et al. Green energy innovation initiatives for environmental sustainability: current state and future research directions. Environ Sci Pollut Res. 2024;31:31752-70.

12 Dhayal KS, Giri AK, Esposito L, Agrawal S. Mapping the significance of green venture capital for sustainable development: a systematic review and future research agenda. J Clean Prod. 2023. https://doi.org/10.1016/j.jclepro.2023.136489. - Dhayal KS, Giri AK, Kumar A, et al. Can green finance facilitate industry 5.0 transition to achieve sustainability? a systematic review with future research directions. Environ Sci Pollut Res. 2023;30:102158-80.

- Peng B, Sheng X, Wei G. Does environmental protection promote economic development? from the perspective of coupling coordination between environmental protection and economic development. Environ Sci Pollut Res. 2020;27:39135-48. https://doi.org/10.1007/ s11356-020-09871-1.

- Polcyn J, Us Y, Lyulyov O, et al. Factors influencing the renewable energy consumption in selected European countries. Energies. 2022;15:1-27. https://doi.org/10.3390/en15010108.

16 Chen VZ, Zhong M, Duran P, Sauerwald S. Multistakeholder benefits: a meta-analysis of different theories. Bus Soc. 2022. https://doi.org/ 10.1177/00076503221110181. - Elkington J. Governance for sustainability. Corp Gov. 2006;14:522-9. https://doi.org/10.1111/j.1467-8683.2006.00527.x.

- Elkington J. Cannibals With Forks: The Triple Bottom Line of 21 st Century Business. Oxford, United Kingdom: Capstone Publishing Limited; 1997.

20. Montabon F, Pagell M, Wu ZH. Making sustainability sustainable. J Supply Chain Manag. 2016;52:11-27. https://doi.org/10.1111/jscm. 12103.

22. Hahn T, Pinkse J, Preuss L, Figge F. Tensions in corporate sustainability: towards an integrative framework. J Bus Ethics. 2015;127:297-316. https://doi.org/10.1007/s10551-014-2047-5.

23. Hubbard G. Measuring organizational performance: beyond the triple bottom line. Bus Strateg Environ. 2009;18:177-91. https://doi. org/10.1002/bse.564.

24. Howard M, Bohm S, Eatherley D. Systems resilience and SME multilevel challenges: a place-based conceptualization of the circular economy. J Bus Res. 2022;145:757-68. https://doi.org/10.1016/j.jbusres.2022.03.014.

25. Gu WT, Wang JY. Research on index construction of sustainable entrepreneurship and its impact on economic growth. J Bus Res. 2022;142:266-76. https://doi.org/10.1016/j.jbusres.2021.12.060.

26 Raza A, Alavi AB, Asif L. Sustainability and financial performance in the banking industry of the United Arab Emirates. Disc Sustain. 2024. https://doi.org/10.1007/s43621-024-00414-z.

27. Chabowski BR, Mena JA, Gonzalez-Padron TL. The structure of sustainability research in marketing, 1958-2008: a basis for future research opportunities. J Acad Mark Sci. 2011;39:55-70. https://doi.org/10.1007/s11747-010-0212-7.

28. Kumar G, Goswami M. Sustainable supply chain performance, its practice and impact on barriers to collaboration. Int J Product Perform Manag. 2019;68:1434-56. https://doi.org/10.1108/IJPPM-12-2018-0425.

29. Ferro C, Padin C, Hogevold N, et al. Validating and expanding a framework of a triple bottom line dominant logic for business sustainability through time and across contexts. J Bus Indust Mark. 2019;34:95-116. https://doi.org/10.1108/JBIM-07-2017-0181.

30. He Q, Gallear D, Ghobadian A, Ramanathan R. Managing knowledge in supply chains: a catalyst to triple bottom line sustainability. Prod Plan Contl. 2019;30:448-63. https://doi.org/10.1080/09537287.2018.1501814.

31. Rosli N, Ha NC, Ghazali EM. Bridging the gap between branding and sustainability by fostering brand credibility and brand attachment in travellers’ hotel choice. Bottom Line. 2019;32:308-39. https://doi.org/10.1108/BL-03-2019-0078.

32 Lajnef K, Ellouz S. Nonlinear causality between CSR and firm performance using NARX model: evidence from France. J Sustain Finance Invest. 2022. https://doi.org/10.1080/20430795.2022.2112140.

33. Hammer J, Pivo G. The triple bottom line and sustainable economic development theory and practice. Econ Dev Q. 2017;31:25-36. https://doi.org/10.1177/0891242416674808.

34. Collste D, Pedercini M, Cornell SE. Policy coherence to achieve the SDGs: using integrated simulation models to assess effective policies. Sustain Sci. 2017;12:921-31. https://doi.org/10.1007/s11625-017-0457-x.

35. Nogueira E, Gomes S, Lopes JM. The key to sustainable economic development: a triple bottom line approach. Resources. 2022;11:46. https://doi.org/10.3390/resources11050046.

36. Cupertino S, Vitale G, Taticchi P. Interdependencies between financial and non-financial performances: a holistic and short-term analytical perspective. Int J Product Perform Manag. 2022. https://doi.org/10.1108/IJPPM-02-2022-0075.

37 Alshehhi A, Nobanee H, Khare N. The impact of sustainability practices on corporate financial performance: literature trends and future research potential. Sustainability. 2018. https://doi.org/10.3390/su10020494.

38. Zabolotnyy S, Wasilewski M. The concept of financial sustainability measurement: a case of food companies from Northern Europe. Sustainability. 2019;11:5139. https://doi.org/10.3390/su11185139.

39 Gleißner W, Günther T, Walkshäusl C. Financial sustainability: measurement and empirical evidence. J Bus Econ. 2022. https://doi.org/ 10.1007/s11573-022-01081-0.

40. Li EL, Zhou LX, Wu AQ. The supply-side of environmental sustainability and export performance: the role of knowledge integration and international buyer involvement. Int Bus Rev. 2017;26:724-35. https://doi.org/10.1016/j.ibusrev.2017.01.002.

41. Agyabeng-Mensah Y, Afum E, Ahenkorah E. Exploring financial performance and green logistics management practices: examining the mediating influences of market, environmental and social performances. J Clean Prod. 2020;258: 120613. https://doi.org/10. 1016/j.jclepro.2020.120613.

42. Agyabeng-Mensah Y, Ahenkorah E, Afum E, Owusu D. The influence of lean management and environmental practices on relative competitive quality advantage and performance. J Manuf Technol Manag. 2020;31:1351-72. https://doi.org/10.1108/ JMTM-12-2019-0443.

43. Khan M, Rahman HU, Baloch QB, et al. Is there any difference between the theory and practice for the association between environmental sustainability and firm performance in Pakistan? Bus Strat Dev. 2021;4:371-82. https://doi.org/10.1002/bsd2.164.

44 Malesios C, De D, Moursellas A, et al. Sustainability performance analysis of small and medium sized enterprises: criteria, methods and framework. Socio-Econ Plan Sci. 2021. https://doi.org/10.1016/j.seps.2020.100993.

45. van Emous R, Krušinskas R, Westerman W. Carbon emissions reduction and corporate financial performance: the influence of countrylevel characteristics. Energies. 2021;14:6029. https://doi.org/10.3390/en14196029.

46. Nogueira E, Gomes S, Lopes JM. Triple bottom line, sustainability, and economic development: what binds them together? A Bibliometric Appr Sustain. 2023;15:6706. https://doi.org/10.3390/su15086706.

47. Karman A, Prokop V, Giglio C, Rehman FU. Has the Covid-19 pandemic jeopardized firms’ environmental behavior Bridging green initiatives and firm value through the triple bottom line approach. Corporate Soc Respons Environ Manag. 2023. https://doi.org/10.1002/csr. 2575.

48. Tate WL, Bals L. Achieving shared triple bottom line (TBL) value creation: toward a social resource-based view (SRBV) of the firm. J Bus Ethics. 2018;152:803-26. https://doi.org/10.1007/s10551-016-3344-y.

49. Mair J, Martí I. Social entrepreneurship research: a source of explanation, prediction, and delight. J World Bus. 2006;41:36-44. https:// doi.org/10.1016/j.jwb.2005.09.002.

50. Murphy PJ, Coombes SM. A model of social entrepreneurial discovery. J Bus Ethics. 2009;87:325-36. https://doi.org/10.1007/ s10551-008-9921-y.

51. Certo ST, MillerT. Social entrepreneurship: key issues and concepts. Bus Horiz. 2008;51:267-71. https://doi.org/10.1016/j.bushor.2008. 02.009.

52. Narangajavana Y, Gonzalez-Cruz T, Garrigos-Simon FJ, Cruz-Ros S. Measuring social entrepreneurship and social value with leakage. definition, analysis and policies for the hospitality industry. Int Entre Manag J. 2016;12:911-34. https://doi.org/10.1007/s11365-016-0396-5.

53. Fetrati MA, Hansen D, Akhavan P. How to manage creativity in organizations: connecting the literature on organizational creativity through bibliometric research. Technovation. 2022;115: 102473. https://doi.org/10.1016/j.technovation.2022.102473.

54. Ajmal MM, Khan M, Hussain M, Helo P. Conceptualizing and incorporating social sustainability in the business world. Int J Sust Dev World. 2018;25:327-39. https://doi.org/10.1080/13504509.2017.1408714.

55 Nogueira E, Gomes S, Lopes JM. The contribution of the labour practices to organizational performance: the mediating role of social sustainability. Bus Ethics Environ Respons. 2024. https://doi.org/10.1111/beer.12682.

56. Zupic I, Čater T. Bibliometric methods in management and organization. Organ Res Methods. 2015;18:429-72. https://doi.org/10.1177/ 1094428114562629.

57. Milojevic S, Sugimoto CR, Yan EJ, Ding Y. The cognitive structure of library and information science: analysis of article title words. J Am Soc Inform Sci Technol. 2011;62:1933-53. https://doi.org/10.1002/asi.21602.

58. Zhi W, Yuan L, Ji GD, et al. A bibliometric review on carbon cycling research during 1993-2013. Environ Earth Sci. 2015;74:6065-75. https://doi.org/10.1007/s12665-015-4629-7.

59. Liu Z, Yin Y, Liu W, Dunford M. Visualizing the intellectual structure and evolution of innovation systems research: a bibliometric analysis. Scientometrics. 2015;103:135-58. https://doi.org/10.1007/s11192-014-1517-y.

60. Franceschini S, Faria LGD, Jurowetzki R. Unveiling scientific communities about sustainability and innovation. a bibliometric journey around sustainable terms. J Clean Prod. 2016;127:72-83. https://doi.org/10.1016/j.jclepro.2016.03.142.

61. Lopes JM, Laurett R, Antunes H, Oliveira J. Entrepreneurial marketing: a bibliometric analysis of the second decade of the 21st century and future agenda. J Res Mark Entrep. 2021;23:295-317. https://doi.org/10.1108/JRME-02-2019-0019.

62. Lopes JM, Gomes S, Durão M, Pacheco R. The holy grail of luxury tourism: a holistic bibliometric overview. J Qual Assur Hosp Tour. 2022. https://doi.org/10.1080/1528008X.2022.2089946.

63. Thirumaran K, Jang HJ, Pourabedin Z, Wood J. The role of social media in the luxury tourism business: a research review and trajectory assessment. Sustainability. 2021;13:1-13. https://doi.org/10.3390/su13031216.

64. Ay I, Sc S. Developing a green business portfolio. Long Range Plan. 1995;28:29-38. https://doi.org/10.1016/0024-6301(95)98587-I.

65. Singh A. A decade of operations strategy: research issues and future research directions. Compet Rev. 2024. https://doi.org/10.1108/ CR-06-2024-0116.

66. Patra SP, Wankhede VA, Agrawal R. Circular economy practices in supply chain finance: a state-of-the-art review. Benchmarking: An Int J. 2024. https://doi.org/10.1108/BIJ-10-2022-0627.

67. Tommasetti A, Maione G, Bignardi A, Lentini P. Environmental accounting in the public sector: a systematic literature review. Int J Bus Environ. 2023;14:164-82. https://doi.org/10.1504/IJBE.2023.129907.

68. Fahim F, Mahadi B. Green trade credit and sustainable firm performances during COVID-19: a conceptual review. Vision- J Bus Perspect. 2023;27:593-603. https://doi.org/10.1177/09722629221096050.

69 Kwarteng P, Appiah KO, Addai B. Influence of board mechanisms on sustainability performance for listed firms in Sub-Saharan Africa. Future Bus J. 2023. https://doi.org/10.1186/s43093-023-00258-5.

70. Farooq Q, Fu PH, Liu X, Hao YH. Basics of macro to microlevel corporate social responsibility and advancement in triple bottom line theory. Corp Soc Responsib Environ Manag. 2021;28:969-79. https://doi.org/10.1002/csr.2069.

71. Arslan M. Corporate social sustainability in supply chain management: a literature review. J Global Respons. 2020;11:233-55. https:// doi.org/10.1108/JGR-11-2019-0108.

72. Dzhengiz T, Niesten E. Competences for environmental sustainability: a systematic review on the impact of absorptive capacity and capabilities. J Bus Ethics. 2020;162:881-906. https://doi.org/10.1007/s10551-019-04360-z.

73. Isabel Cubilla-Montilla M, Galindo-Villardon P, Belen Nieto-Librero A, et al. What companies do not disclose about their environmental policy and what institutional pressures may do to respect. Corp Soc Responsib Environ Manag. 2020;27:1181-97. https://doi.org/10. 1002/csr. 1874.

74. Yun G, Yalcin MG, Hales DN, Kwon HY. Interactions in sustainable supply chain management: a framework review. Int J Logist Manag. 2019;30:140-73. https://doi.org/10.1108/IJLM-05-2017-0112.

75. Carter CR, Hatton MR, Wu C, Chen XJ. Sustainable supply chain management: continuing evolution and future directions. Int J Phys Distrib Logist Manag. 2019;50:122-46. https://doi.org/10.1108/IJPDLM-02-2019-0056.

76. Yawar SA, Seuring S. Management of social issues in supply chains: a literature review exploring social issues, actions and performance outcomes. J Bus Ethics. 2017;141:621-43. https://doi.org/10.1007/s10551-015-2719-9.

77. Chugani N, Kumar V, Garza-Reyes JA, et al. Investigating the green impact of Lean, Six Sigma and Lean Six Sigma. Int J Lean Six Sigma. 2017;8:7-32. https://doi.org/10.1108/IJLSS-11-2015-0043.

78. Xu X, Gursoy D. A conceptual framework of sustainable hospitality supply chain management. J Hosp Market Manag. 2015;24:229-59. https://doi.org/10.1080/19368623.2014.909691.

79. Liu RL. A new bibliographic coupling measure with descriptive capability. Scientometrics. 2017;110:915-35. https://doi.org/10.1007/ s11192-016-2196-7.

80. Donthu N, Kumar S, Mukherjee D, et al. How to conduct a bibliometric analysis: an overview and guidelines. J Bus Res. 2021;133:285-96. https://doi.org/10.1016/j.jbusres.2021.04.070.

81 Vhatkar MS, Raut RD, Gokhale R, et al. Leveraging digital technology in retailing business: unboxing synergy between omnichannel retail adoption and sustainable retail performance. J Retail Cons Serv. 2024. https://doi.org/10.1016/j.jretconser.2024.104047.

82. El Akremi A, Gond JP, Swaen V, et al. How do employees perceive corporate responsibility? development and validation of a multidimensional corporate stakeholder responsibility scale. J Manag. 2018;44:619-57. https://doi.org/10.1177/0149206315569311.

83. Grudzien D, Pfutzenreuter T, Galli F, et al. Sustainable strategic operations supported by I4.0 digital technologies. J Indust Integ ManagInnov Entrepreneurship. 2023;08:39-64. https://doi.org/10.1142/S2424862222500270.

84. Wu XD, Amoasi R. The role of CSR in sustaining corporate brands in the global market: the perspective of telecommunication companies in Ghana. Corp Soc Responsib Environ Manag. 2024. https://doi.org/10.1002/csr.2578.

85. Escamilla-Solano S, Fernández-Portillo A, Orden-Cruz C, Sánchez-Escobedo MC. Corporate social responsibility disclosure: mediating effects of the economic dimension on firm performance. Corp Soc Responsib Environ Manag. 2024. https://doi.org/10.1002/csr.2596.

86. Menz KM. Corporate social responsibility: is it rewarded by the corporate bond market? a critical note. J Bus Ethics. 2010;96:117-34. https://doi.org/10.1007/s10551-010-0452-y.

87. Galletta S, Mazzu S, Naciti V, Vermiglio C. Gender diversity and sustainability performance in the banking industry. Corp Soc Responsib Environ Manag. 2022;29:161-74. https://doi.org/10.1002/csr.2191.

88. Dakhli A. Do women on corporate boardrooms have an impact on tax avoidance? the mediating role of corporate social responsibility. Corporate Governance- Int J Bus Soc. 2022;22:821-45. https://doi.org/10.1108/CG-07-2021-0265.

89. Menicucci E, Paolucci G. Board gender equality and ESG performance. evidence from European banking sector. Corporate GovernanceInt J Bus Soc. 2024;24:147-74. https://doi.org/10.1108/CG-04-2023-0146.

90. Zubeltzu-Jaka E, Alvarez-Etxeberria I, Aldaz-Odriozola M. Corporate social responsibility oriented boards and triple bottom line performance: a meta-analytic study. Business Strategy and Development. 2024. https://doi.org/10.1002/bsd2.320.

91. Rath C, Tripathy A, Mangla SK. How the social dimension of ESG influences CEO compensation: role of CEO and board characteristics. Bus Strateg Environ. 2024. https://doi.org/10.1002/bse.4008.

92. Lu J, Rodenburg K, Foti L, Pegoraro A. Are firms with better sustainability performance more resilient during crises? Bus Strateg Environ. 2022;31:1-17. https://doi.org/10.1002/bse.3088.

93. Turker D, Ozmen YS. Understanding how social responsibility drives social innovation: characteristics of radically innovative projects. Eur J Innov Manag. 2022;25:680-702. https://doi.org/10.1108/EJIM-08-2020-0314.

94. Nagiah GR, Suki NM. Linking environmental sustainability, social sustainability, corporate reputation and the business performance of energy companies: insights from an emerging market. Int J Energy Sect Manage. 2024;18:1905-22. https://doi.org/10.1108/ IJESM-06-2023-0003.

95. Vargas-Santander KG, Alvarez-Diez S, Baixauli-Soler S, Belda-Ruiz M. Corporate social responsibility and financial performance: does country sustainability matter? Corp Soc Responsib Environ Manag. 2023;30:3075-94. https://doi.org/10.1002/csr.2539.

96 Jaiwani M, Gopalkrishnan S. Do private and public sector banks respond to ESG in the same way? some evidences from India. Bench-marking-An Int J. 2023. https://doi.org/10.1108/BIJ-05-2023-0340.

97. Alcouffe S , Boitier M, Jabot R. An integrated literature review on the adoption and diffusion of multicapital accounting innovations. Sustain Account Manag Policy J. 2024. https://doi.org/10.1108/SAMPJ-12-2023-0912.

98. de Pilla LHL, Peci A, Leite RD. Is the state a socially responsible shareholder? state-owned enterprises, political ideology, and corporate social performance. J Bus Ethics. 2024. https://doi.org/10.1007/s10551-024-05751-7.

99 Avelar S, Borges-Tiago T, Almeida A, Tiago F. Confluence of sustainable entrepreneurship, innovation, and digitalization in SMEs. J Busi Res. 2024. https://doi.org/10.1016/j.jbusres.2023.114346.

100. Arda OA, Montabon F, Tatoglu E, et al. Toward a holistic understanding of sustainability in corporations: resource-based view of sustainable supply chain management. Supply Chain Manag. 2023;28:193-208. https://doi.org/10.1108/SCM-08-2021-0385.

101. Tran T, Kim S, Son BG, Ramkumar M. Paradoxical association between lean manufacturing sustainability practices and triple bottom line performance. IEEE Trans Eng Manag. 2023. https://doi.org/10.1109/TEM.2023.3290724.

102. Khan SAR, Yu Z, Umar M, Tanveer M. Green capabilities and green purchasing practices: a strategy striving towards sustainable operations. Bus Strateg Environ. 2022;31:1719-29. https://doi.org/10.1002/bse.2979.

103. Saglam YC. Analyzing sustainable reverse logistics capability and triple bottom line: the mediating role of sustainability culture. J Manuf Technol Manag. 2023;34:1162-82. https://doi.org/10.1108/JMTM-01-2023-0009.

104. De Giovanni P. Do internal and external environmental management contribute to the triple bottom line? Int J Oper Prod Manag. 2012;32:265-90. https://doi.org/10.1108/01443571211212574.

105. Ahmad F, Khokhar SG. Examining the impact of sustainable supply chain management practices and supply chain ambidexterity on sustainability performance. Operat Supply Chain Manag-An Int J. 2024;17:179-90.

106. Carter CR, Easton PL. Sustainable supply chain management: evolution and future directions. Int J Phys Distrib Logist Manag. 2011;41:4662. https://doi.org/10.1108/09600031111101420.

107. Oubrahim I, Sefiani N. An integrated multi-criteria decision-making approach for sustainable supply chain performance evaluation from a manufacturing perspective. Int J Product Perform Manag. 2024. https://doi.org/10.1108/IJPPM-09-2023-0464.

108. Morgan YC, Fok L, Zee S. Examining the impact of environmental and organizational priorities on sustainability performance in service industries. Int J Product Perform Manag. 2023. https://doi.org/10.1108/IJPPM-02-2023-0053.

109 Nogueira E, Gomes S, Lopes JM. A meta-regression analysis of environmental sustainability practices and firm performance. J Clean Produ. 2023. https://doi.org/10.1016/j.jclepro.2023.139048.

110. Ertz M, Latrous I, Dakhlaoui A, Sun SH. The impact of big data analytics on firm sustainable performance. Corp Soc Responsib Environ Manag. 2024. https://doi.org/10.1002/csr.2990.

111. Li Y, Li JY, Zhai YF. Intellectual capital and sustainability performance: the mediating role of digitalization. J Intellect Cap. 2024;25:867-90. https://doi.org/10.1108/JIC-06-2023-0129.

112. Huang SS, Wang XQ, Qu H. Impact of perceived corporate social responsibility on peer-to-peer accommodation consumers’ repurchase intention and switching intention. J Hosp Market Manag. 2023;32:893-916. https://doi.org/10.1080/19368623.2023.2214549.

113. Carter CR, Rogers DS. A framework of sustainable supply chain management: moving toward new theory. Int J Phys Distrib Logist Manag. 2008;38:360-87. https://doi.org/10.1108/09600030810882816.

114. Torugsa NA, O’Donohue W, Hecker R. Proactive CSR: An empirical analysis of the role of its economic, social and environmental dimensions on the association between capabilities and performance. J Bus Ethics. 2013;115:383-402. https://doi.org/10.1007/s10551-012-1405-4.

115. Coelho A, Ferreira J, Proença C. The impact of green entrepreneurial orientation on sustainability performance through the effects of green product and process innovation: the moderating role of ambidexterity. Bus Strateg Environ. 2024. https://doi.org/10.1002/bse. 3648.

116. González-Ramos MI, Donate MJ, Guadamillas F. The relationship between knowledge management strategies and corporate social responsibility: effects on innovation capabilities. Technol Forecast Soc Chang. 2023;188: 122287. https://doi.org/10.1016/j.techfore. 2022.122287.

117. Lee MJ, Pak A, Roh T. The interplay of institutional pressures, digitalization capability, environmental, social, and governance strategy, and triple bottom line performance: a moderated mediation model. Bus Strategy Environ. 2024;33:5247-68. https://doi.org/10.1002/ bse. 3755.

118. Marzouk J, El Ebrashi R. The interplay among green absorptive capacity, green entrepreneurial, and learning orientations and their effect on triple bottom line performance. Bus Strateg Environ. 2024. https://doi.org/10.1002/bse.3588.

119 Nogueira E, Gomes S, Lopes JM. Financial sustainability: exploring the influence of the triple bottom line economic dimension on firm performance. Sustainability. 2024. https://doi.org/10.3390/su16156458.

- Elisabete Nogueira, elisabete.s.nogueira@gmail.com; Sofia Gomes, sofiag@upt.pt; João M. Lopes, joao.lopes.1987@gmail.com |

¹Research on Economics, Management and Information Technologies, REMIT, Portucalense University, Rua Dr. António Bernardino Almeida, 541-619, 4200-072 Porto, Portugal.Instituto Superior Miguel Torga, Coimbra, Portugal & NECE-UBI – Research Unit in Business Sciences, University of Beira Interior, Covilhã, Portugal.