DOI: https://doi.org/10.58251/ekonomi.1450860

تاريخ النشر: 2024-03-13

مسار جديد نحو الاستدامة: دمج البعد الاقتصادي (ECON) في عوامل ESG كـ (ECON-ESG) ومتوافق مع أهداف التنمية المستدامة (SDGs)

مسار جديد نحو الاستدامة: دمج البعد الاقتصادي (ECON) في عوامل ESG كـ (ECON-ESG) ومتوافق مع أهداف التنمية المستدامة (SDGs)

معلومات المقال

الكلمات المفتاحية:

أهداف التنمية المستدامة

عوامل ESG

شكل جديد من الاستدامة

عوامل اقتصادية

الاستدامة

الملخص

مفهوم عوامل ESG التقليدية (البيئية، الاجتماعية، الحوكمة) هو شرط أساسي للاستدامة ويشكل الأسس لاقتصاد مستدام. ومع ذلك، على الرغم من التأثيرات الحتمية للأنشطة الاقتصادية على الاستدامة، فإنه يفتقر إلى البعد الاقتصادي (يمثل ECON). لذلك، تقترح هذه الدراسة إكمال هذا الجانب المفقود، ودمج الاقتصاد في ESG، والحصول على وتقديم ECON-ESG كمفهوم استدامة مركب. بينما تمثل ESG الاستدامة المعتمدة على الشركات والميكرو اقتصاد فقط بناءً على العوامل البيئية والاجتماعية والحوكمة، فإن ECON-ESG يدمج أيضًا الاقتصاد ويمثل الاستدامة، بما في ذلك الماكرو اقتصاد الذي يؤثر على أداء الشركات. بالإضافة إلى ذلك، فإن الربط بين ECON-ESG وSDGs سيوفر للباحثين متغيرًا مركبًا للاستخدام في نماذج الاستدامة.

مقدمة

- تدمج ESG المعتمدة على الشركات الميكرو اقتصاد المحتوى الماكرو اقتصادي مع مؤشرات ماكرو اقتصادية إضافية مثل الناتج المحلي الإجمالي، والبطالة، ومعدلات الفائدة. لذلك، قد تمثل عوامل ECON-ESG الاستدامة، بما في ذلك الاقتصاد، مع التأثير الحتمي للماكرو اقتصاد حيث تتأثر الشركات مباشرة بالسياسات الماكرو اقتصادية.

- يبدأ المستثمرون في التعرف بشكل متزايد على أهمية الاستدامة الاقتصادية جنبًا إلى جنب مع اعتبارات ESG. إن تضمين العوامل الاقتصادية في ESG وجعلها ECON-ESG سيعزز من أهميتها للمستثمرين الذين يسعون لمواءمة استثماراتهم مع الأهداف المالية وأهداف التنمية المستدامة.

- سيشجع شكل ECON-ESG صانعي السياسات على اعتماد سياسات تعزز النمو الاقتصادي المستدام مع معالجة التحديات البيئية والاجتماعية. يعزز هذا التوافق نهجًا متوازنًا في صنع السياسات يدعم الازدهار والرفاهية على المدى الطويل.

- ترتبط الاستقرار الاقتصادي ارتباطًا وثيقًا بالاستدامة العامة. سيساعد تقييم العوامل الاقتصادية جنبًا إلى جنب مع مقاييس ESG في تحديد المخاطر والضعف المحتملة، مما يمكّن أصحاب المصلحة من تنفيذ تدابير استباقية للتخفيف من المخاطر الاقتصادية والبيئية والاجتماعية.

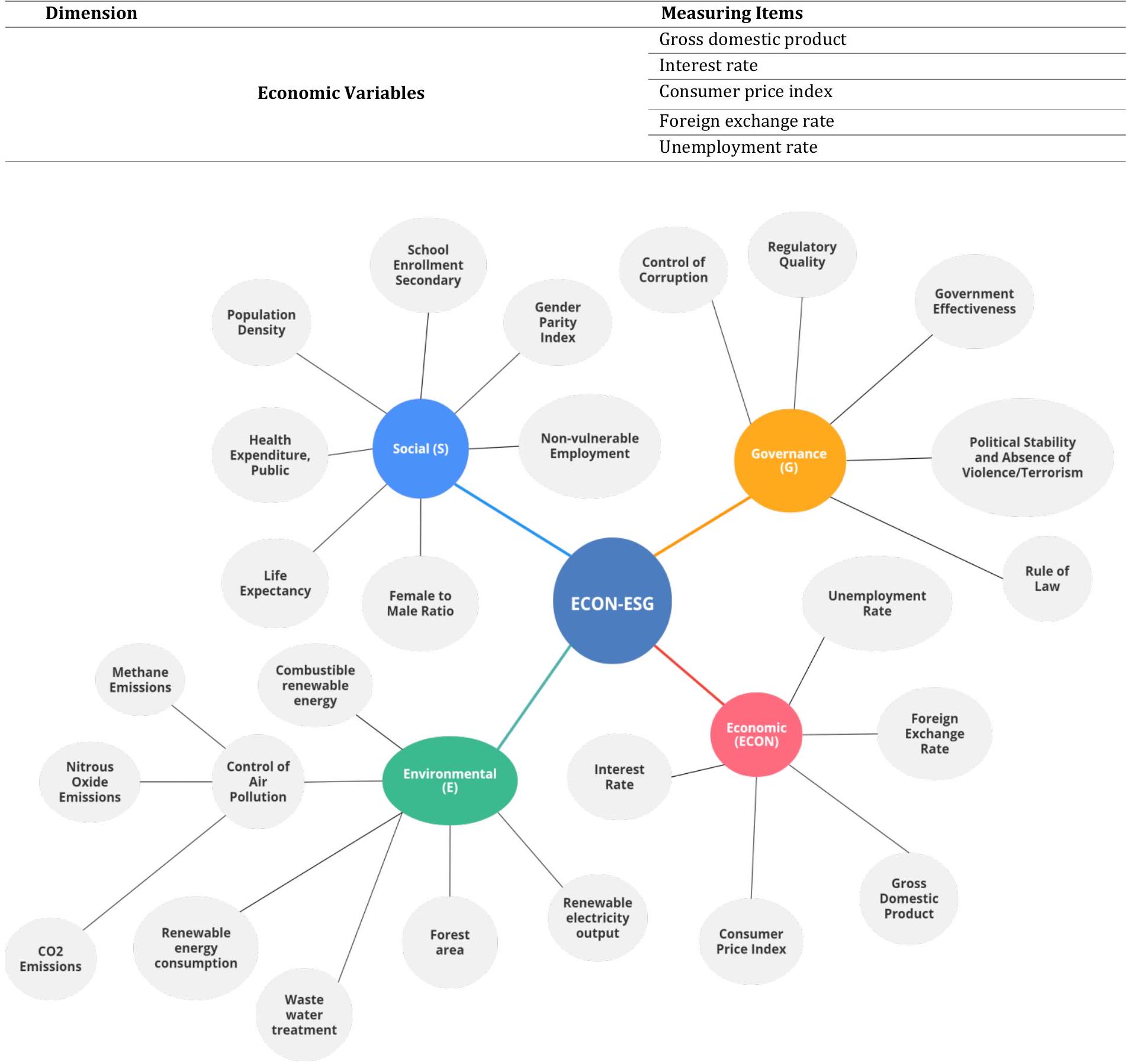

- يربط شكلنا المقترح، ECON-ESG، أهداف التنمية المستدامة للأمم المتحدة (SDGs) من خلال استخدام بعض المؤشرات المختارة (الموضحة في الجدول 1) من 232 مؤشرًا لأهداف التنمية المستدامة. تتوافق هذه المؤشرات المختارة، مثل انبعاثات CO2، ومكافحة الفساد، وفعالية الحكومة، مع البيئة (E)، والاجتماع (S)، والحوكمة (G)، على التوالي. بعد هذه المؤشرات، نضيف مؤشرات ماكرو اقتصادية (ECON) إلى ESG. هذا الربط بين ECON-ESG وSDGs ضروري لأن مؤشرات أهداف التنمية المستدامة هي

- سيمكننا هذا الربط أيضًا من التساؤل عما إذا كانت نتائج الدراسات التجريبية التي تستخدم شكل ECON-ESG تتناغم مع عوامل SDG في إطار مؤشرات SDG المستخدمة.

- سيوفر نفس الربط بين ECON-ESG وSDGs للباحثين متغيرًا مركبًا للاستخدام في نماذج الاستدامة. يمكن لصانعي السياسات الاستفادة من مؤشرات SDG لتحديد المجالات التي يمكن دمج عوامل ESG فيها ضمن أطر السياسات، مما يؤدي إلى حلول سياسية أكثر شمولية وفعالية.

- قد يحسن نفس الربط من آليات المساءلة والتقارير لقياس التقدم؛ يمكن لصانعي السياسات تعزيز الشفافية والمساءلة في مراقبة فعالية السياسات والمبادرات التي تعزز الاستدامة.

مراجعة الأدبيات

المؤشرات المستخدمة لعوامل ESG

| البعد | عناصر القياس |

| البيئة | استهلاك الطاقة المتجددة |

| الطاقة المتجددة القابلة للاحتراق (% من إجمالي الطاقة) | |

| إنتاج الكهرباء المتجددة | |

| مساحة الغابات | |

| مراقبة تلوث الهواء (انبعاثات CO2، انبعاثات الميثان، انبعاثات أكسيد النيتروز) | |

| استنفاد الموارد الطبيعية | |

| الوصول إلى الوقود والتقنيات النظيفة للطهي | |

| معالجة مياه الصرف الصحي | |

| الاجتماع | التحاق المدارس الثانوية |

| الإنفاق الصحي، العام | |

| متوسط العمر المتوقع | |

| كثافة السكان | |

| نسبة الإناث إلى الذكور | |

| مؤشر المساواة بين الجنسين | |

| التوظيف غير المعرض للخطر | |

| الحوكمة | مكافحة الفساد |

| جودة التنظيم | |

| سيادة القانون | |

| فعالية الحكومة | |

| الاستقرار السياسي وغياب العنف/الإرهاب |

المؤشرات المستخدمة لعوامل الاقتصاد

5. المنهجية

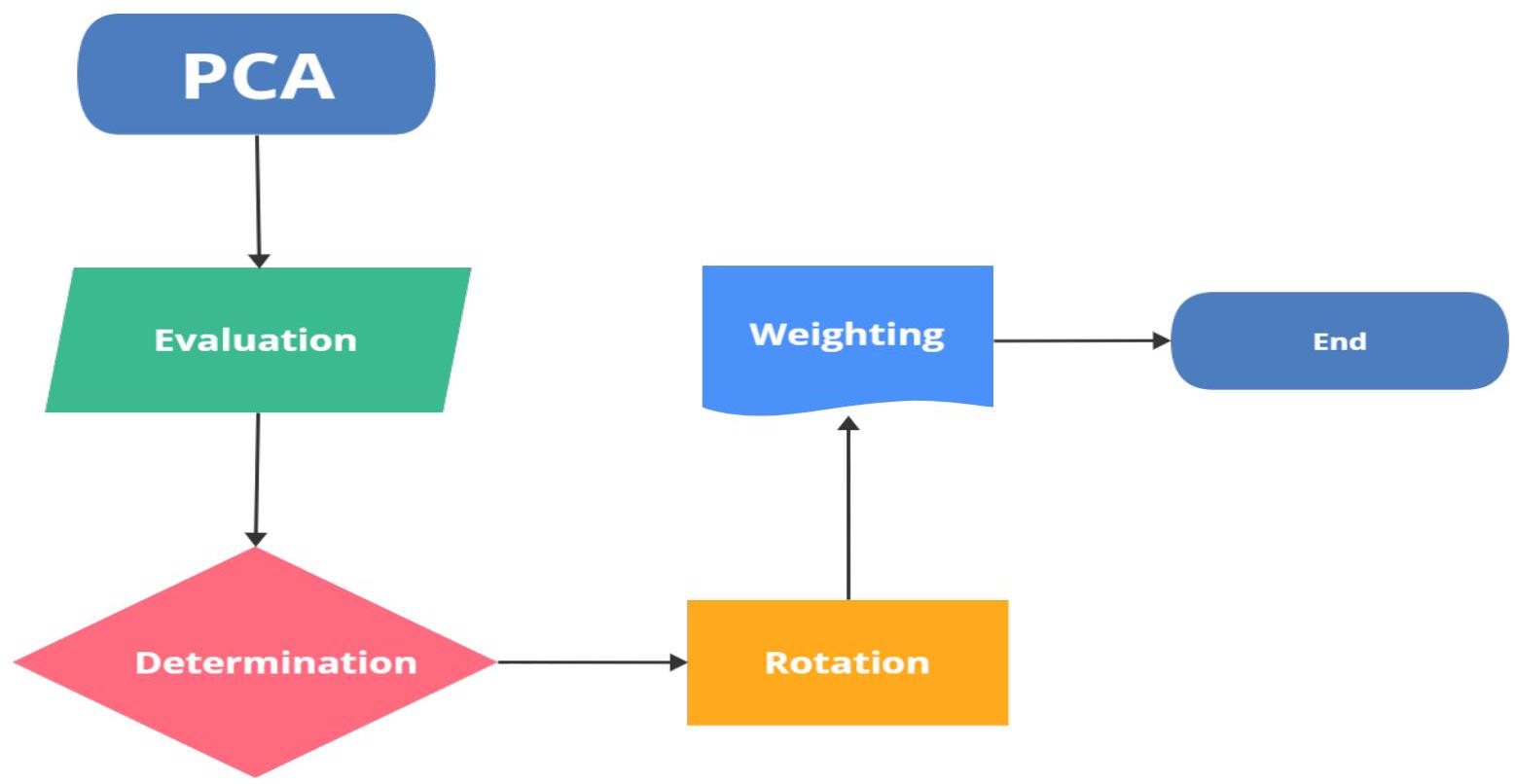

- التقييم: تقييم علاقات المتغيرات باستخدام مقياس كايزر-ماير-أولكين (KMO)، مع إحصائية KMO عتبة تبلغ 0.6، للمتابعة مع تحليل العوامل (Kaiser and Rice, 1974). يقيم هذا المقياس مدى ملاءمة المتغيرات لتحليل العوامل من خلال مقارنة مجموع التباينات المربعة مع مجموع التباينات الجزئية المربعة.

- التحديد: تحديد عدد العوامل المطلوبة وحسابها من خلال PCA. العوامل هي معاملات (أحمال) تقيس الارتباطات بين المؤشرات الفردية والعوامل الكامنة. يشكل PCA تركيبات خطية من المؤشرات الأساسية، حيث يلتقط المكون الرئيسي الأول أعلى تباين في العينة، تليه مكونات متعاقبة تفسر أجزاء أصغر من التباين وتكون غير مرتبطة ببعضها البعض.

- الدوران: تدوير العوامل لتبسيط التفسير. يعد دوران العوامل خطوة قياسية في تحليل العوامل تهدف إلى تقليل عدم اليقين في النتائج. طريقة فاريمكس، المستخدمة هنا، تقلل من عدد المتغيرات ذات الأحمال العالية على نفس العامل، مما يقرب من “هيكل بسيط” حيث يحمل كل مؤشر بشكل رئيسي على عامل واحد محتفظ به. يعزز ذلك من قابلية تفسير العوامل.

- الوزن: بناء أوزان للمؤشرات الملخصة بناءً على أحمال العوامل ومساهمتها في التباين المفسر. يتم وزن المؤشرات التفصيلية وفقًا لنسبة التباين المفسر بواسطة العوامل المرتبطة (الأحمال المربعة العادية). في المقابل، يتم وزن العوامل بناءً على مساهمتها في التباين المفسر في مجموعة البيانات (مجموع الأحمال المربعة العادية).

6. الخاتمة

6.1 الفجوة المستقبلية والقيود

الامتثال للمعايير الأخلاقية

موافقة الأخلاقيات والموافقة على المشاركة: غير قابل للتطبيق.

الموافقة على النشر: غير قابل للتطبيق

التمويل: غير قابل للتطبيق

References

Zarnowitz, V., & Braun, P. (1989). New Indexes of Coincident and Leading Economic Indicators: Comment. NBER Macroeconomics Annual, 4, 397. https://doi.org/10.2307/3584987.

- Corresponding author. E-mail address: cemisik@anadolu.edu.tr (C. Işık).

Received: 11 March 2024; Received in revised from 28 March 2024; Accepted 01 April 2024

http://dx.doi.org/10.58251/ekonomi. 1450860

DOI: https://doi.org/10.58251/ekonomi.1450860

Publication Date: 2024-03-13

Ekonomi

journal homepage: https://dergipark.org.tr/ekonomi

A new pathway to sustainability: Integrating economic dimension (ECON) into ESG factors as (ECON-ESG) and aligned with sustainable development goals (SDGs)

ARTICLE INFO

Keywords:

SDGs

ESG factors

New form of sustainability

Economic factors

Sustainability

Abstract

The concept of traditional ESG (Environmental, Social, Governance) factors is a sine qua non for sustainability and constitutes the cornerstones of a sustainable economy. However, although the inevitable impacts of economic activities on sustainability, it lacks the economic dimension (denotes ECON). Therefore, this study proposes to complete this missing leg, integrate economics into ESG, and obtain and introduce ECON-ESG as a composite sustainability concept. While ESG represents firm and microeconomics-based sustainability based only on environmental, social, and governance factors, ECON-ESG also incorporates the economy and represents sustainability, including macroeconomics affecting the firm’s performance. Additionally, the linkage between ECON-ESG and SDGs will provide scholars with a composite form variable for use in sustainability models.

I. Introduction

- Firm-based microeconomic ESG incorporates macroeconomic content with added macroeconomic indicators such as GDP, unemployment, and interest rates. Therefore, ECON-ESG factors may represent sustainability, including the economy, with the inevitable impact of macroeconomics since firms are directly affected by macroeconomic policies.

- Investors increasingly recognize the importance of economic sustainability alongside ESG considerations. Including economic factors into ESG and making it ECON-ESG will enhance its relevance to investors seeking to align their investments with both financial and sustainable development goals.

- ECON-ESG form will encourage policymakers to adopt policies that foster sustainable economic growth while addressing environmental and social challenges. This alignment promotes a balanced approach to policymaking that supports long-term prosperity and well-being.

- Economic stability is closely linked to overall sustainability. Assessing economic factors alongside ESG metrics will help identify potential risks and vulnerabilities, enabling stakeholders to implement proactive measures to mitigate economic, environmental, and social risks.

- Our proposed form, ECON-ESG, links the United Nations’s sustainable development goals (SDGs) by using some selected indicators (shown in Table 1) of 232 SDG indicators. These selected indicators, such as CO2 emissions, control of corruption, and government effectiveness, correspond to the environment (E), social (S), and governance (G), respectively. Following these indicators, we add macroeconomic indicators (ECON) to ESG. This link between ECON-ESG and SDGs is necessary because the Sustainable Development Goals indicators are

- This link will also enable us to question whether the results of empirical studies using the ECON-ESG form harmonize with the SDG factors within the framework of the used SDG indicators.

- The same link between ECON-ESG and SDGs will provide scholars with a composite form variable for use in sustainability models. Policymakers can leverage SDG indicators to identify areas where ESG factors can be incorporated into policy frameworks, leading to more holistic and effective policy solutions.

- The same link may improve accountability and reporting mechanisms to measure progress; policymakers can enhance transparency and accountability in monitoring the effectiveness of policies and initiatives promoting sustainability.

2. Literature Review

3. Indicators Used for ESG Factors

| Dimension | Measuring Items |

| Environmental | Renewable energy consumption |

| Combustible renewable energy (% of total energy) | |

| Renewable electricity output | |

| Forest area | |

| Control air pollution (CO2 emissions, Methane emissions, Nitrous oxide emission) | |

| Natural resources depletion | |

| Access to clean fuels and technologies for cooking | |

| Waste water treatment | |

| Social | School enrollment secondary |

| Health expenditure, public | |

| Life expectancy | |

| Population density | |

| Female to male Ratio | |

| Gender parity index | |

| Non-vulnerable employment | |

| Governance | Control of corruption |

| Regulatory quality | |

| Rule of law | |

| Government effectiveness | |

| Political stability and absence of violence/terrorism |

4. Indicators Used for Economic Factors

5. Methodology

- Evaluation: Evaluating variable relationships using the Kaiser-Meyer-Olkin (KMO) measure, with a threshold KMO statistic of 0.6 , to proceed with factor analysis (Kaiser and Rice, 1974). This measure assesses how well-suited the variables are for factor analysis by comparing the sum of squared correlations to the sum of squared partial correlations.

- Determination: Determining the number of factors needed and their calculation through PCA. Factors are coefficients (loadings) that measure correlations between individual indicators and latent factors. PCA forms linear combinations of fundamental indicators, with the first principal component capturing the highest variance in the sample, followed by successive components explaining smaller portions of variance and being uncorrelated with each other.

- Rotation: Rotating factors to simplify interpretation. Factor rotation is a standard step in factor analysis aimed at reducing indeterminacy in results. The varimax method, employed here, minimizes the number of variables with high loadings on the same factor, thereby approximating a “simple structure” where each indicator predominantly loads on one retained factor. This enhances factor interpretability.

- Weighting: Constructing weights for summary indicators based on factor loadings and their contribution to explained variance. Detailed indicators are weighted according to the proportion of variance explained by associated factors (normalized squared loading). In contrast, factors are weighted based on their contribution to the explained variance in the dataset (normalized sum of squared loadings).

6. Conclusion

6.1 Future Gap and Limitations

Compliance with ethical standards

Ethics approval and consent to participate: Not applicable.

Consent for publication: Not applicable

Funding: Not applicable

References

Zarnowitz, V., & Braun, P. (1989). New Indexes of Coincident and Leading Economic Indicators: Comment. NBER Macroeconomics Annual, 4, 397. https://doi.org/10.2307/3584987.

- Corresponding author. E-mail address: cemisik@anadolu.edu.tr (C. Işık).

Received: 11 March 2024; Received in revised from 28 March 2024; Accepted 01 April 2024

http://dx.doi.org/10.58251/ekonomi. 1450860