DOI: https://doi.org/10.1038/s41598-025-93694-y

PMID: https://pubmed.ncbi.nlm.nih.gov/40074861

تاريخ النشر: 2025-03-12

تقارير علمية

افتح

أثر أداء ESG المدفوع بالذكاء الاصطناعي على التنمية المستدامة للشركات المملوكة للدولة المركزية المدرجة

الملخص

يوبينغ شياو

خلفية البحث والدوافع

أهداف البحث

مراجعة الأدبيات

نظرة عامة على أداء ESG والتنمية المستدامة للشركات

نظرة عامة على تطبيق الذكاء الاصطناعي في ممارسات ESG

لردود فعل الموظفين والمشاعر المجتمعية، مما يمكّن الشركات من تعديل استراتيجيات المسؤولية الاجتماعية للشركات بسرعة

نظرة عامة على تحليل ممارسات ESG المعززة بالذكاء الاصطناعي من منظور عالمي وصيني

الفجوات البحثية والافتراضات للدراسة

(1) وفقًا لنظرية RBV، يمكن أن تساعد تقنية الذكاء الاصطناعي الشركات في تحسين تخصيص الموارد وزيادة كفاءة العمليات، لا سيما في مجالات إدارة البيئة، والمسؤولية الاجتماعية، والحوكمة المؤسسية. على سبيل المثال، يمكن أن يعزز الذكاء الاصطناعي فعالية الشركة في استخدام الموارد، والتحكم في الانبعاثات، وغيرها من المجالات البيئية من خلال أنظمة الإدارة الذكية، مما يحسن الأداء البيئي. يمكن أن يسهم تطبيق الذكاء الاصطناعي في إدارة الموظفين، ومراقبة الصحة، وسلامة مكان العمل أيضًا في تعزيز أداء الشركة في المسؤولية الاجتماعية. علاوة على ذلك، يساهم دور الذكاء الاصطناعي في إدارة المخاطر ودعم اتخاذ القرار في تحسين هيكل الحوكمة للشركة.

(2) يمكن لتكنولوجيا الذكاء الاصطناعي، من خلال دفع التحول على مستويات مختلفة داخل المؤسسات، أن تحسن أداء ESG (البيئة، والمجتمع، والحوكمة) وأيضًا تساهم بشكل محتمل في زيادة أداء التنمية المستدامة للشركات. يشمل أداء التنمية المستدامة جوانب متعددة، بما في ذلك الفوائد الاقتصادية، والمسؤولية الاجتماعية، والأثر البيئي. من خلال تحسين الكفاءة التشغيلية وتحسين تخصيص الموارد، قد يكون لتكنولوجيا الذكاء الاصطناعي تأثير طويل الأمد على النتائج البيئية والاجتماعية والحوكمة.

(3) قد لا تكون العلاقات في الفرضيتين 1 و 2 مباشرة وخطية فقط؛ فقد تلعب أداء الشركات في مجال ESG دورًا وسيطًا بين تطبيق تكنولوجيا الذكاء الاصطناعي وأداء التنمية المستدامة للشركات. وفقًا لنظرية تأثير الوساطة، قد يؤثر تطبيق تكنولوجيا الذكاء الاصطناعي، من خلال تعزيز أداء الشركة في مجالات البيئة والمجتمع والحوكمة، بشكل غير مباشر على نتائج التنمية المستدامة. على سبيل المثال، لا يحسن أداء ESG القوي الصورة الاجتماعية للشركة فحسب، بل قد يعزز أيضًا كفاءة تخصيص الموارد، مما يخلق فرص سوق إضافية وميزات تنافسية.

منهجية البحث

تصميم البحث النوعي

(1) المقابلات المتعمقة: إجراء مقابلات متعمقة مع الإدارة وأصحاب المصلحة الرئيسيين في المؤسسات لجمع رؤى حول وجهات نظرهم وتجاربهم فيما يتعلق بتطبيق تكنولوجيا الذكاء الاصطناعي.

(2) تحليل الوثائق: تحليل التقارير السنوية، تقارير الاستدامة، والإعلانات الرسمية للمؤسسات للحصول على معلومات مفصلة حول حالة تنفيذ مشاريع الذكاء الاصطناعي، وتخصيص الموارد، ونتائج التطبيقات.

تصميم البحث الكمي

| بعد | رقم العنصر | محتوى البيان | أوافق بشدة (5) | موافق (4) | محايد (3) | اختلاف (2) | أعارض بشدة (1) |

| حوكمة الشركات | الربع الأول | عملية اتخاذ القرار في الشركة شفافة | |||||

| الربع الثاني | تستخدم الشركة تقنية الذكاء الاصطناعي لإدارة المخاطر | ||||||

| الربع الثالث | تلتزم الشركة بشكل صارم بالقوانين واللوائح | ||||||

| الربع الرابع | مجلس الإدارة فعال في الإشراف على عمليات الشركة | ||||||

| Q5 | تتخذ الشركة تدابير نشطة لتعزيز كفاءة هيكلها الإداري | ||||||

| حماية البيئة | س6 | تستخدم الشركة تقنية الذكاء الاصطناعي لمراقبة وإدارة تأثيرها البيئي | |||||

| Q7 | لقد حسنت تقنية الذكاء الاصطناعي الأداء البيئي للشركة | ||||||

| الكويت | تستخدم الشركة تقنية الذكاء الاصطناعي لتقليل الفاقد وتعزيز كفاءة الموارد | ||||||

| Q9 | تستخدم الشركة تقنية الذكاء الاصطناعي لتتبع وإدارة بصمتها الكربونية واستهلاكها للطاقة. | ||||||

| Q10 | إن سياسة الشركة في تطبيق حماية البيئة قوية | ||||||

| المسؤولية الاجتماعية | س11 | تحسن الشركة رفاهية الموظفين من خلال تكنولوجيا الذكاء الاصطناعي | |||||

| Q12 | تؤدي الشركة بشكل جيد في المشاركة المجتمعية والأنشطة الخيرية | ||||||

| س13 | تستخدم الشركة تقنية الذكاء الاصطناعي لتعزيز تأثير مبادراتها في المسؤولية الاجتماعية | ||||||

| س14 | تضمن الشركة تحقيق المسؤولية الاجتماعية في إدارة سلسلة التوريد | ||||||

| س15 | تتخذ الشركة بنشاط تدابير لتعزيز الشفافية وفعالية مساهماتها الاجتماعية |

بناء نموذج الانحدار

| نوع المتغير | اسم المتغير | الرمز | طريقة القياس |

| تفسيري | استخدام الذكاء الاصطناعي | الذكاء الاصطناعي | اللوغاريتم الطبيعي لتكرار المصطلحات + 1 |

| تابع | أداء التنمية المستدامة | SDI | يتم قياسه باستخدام SDI |

| وسيط | أداء ESG | ESG | مؤشر Huazheng ESG |

| ضابط | حجم الشركة | الحجم | اللوغاريتم الطبيعي لإجمالي الأصول |

| ضابط | نسبة الرفع | Lev | إجمالي الالتزامات في نهاية السنة / إجمالي الأصول في نهاية السنة |

| ضابط | نسبة دوران الأصول | AT | الإيرادات السنوية / إجمالي الأصول |

| ضابط | معدل نمو الإيرادات | RG | نمو الإيرادات من سنة إلى أخرى |

| ضابط | Q توبين | Q توبين | (القيمة السوقية للأسهم القابلة للتداول + الأسهم غير القابلة للتداول * القيمة الدفترية للسهم + القيمة الدفترية للالتزامات) / إجمالي الأصول |

تصميم تجريبي وتقييم الأداء

جمع مجموعات البيانات

(1) تمثيل الصناعة

(2) مستوى أداء ESG

(3) درجة تطبيق الذكاء الاصطناعي

(4) إمكانية الوصول إلى البيانات

التقارير. يتم حساب تكرار المصطلحات المتعلقة بالذكاء الاصطناعي لبناء مؤشر كمي لاستخدام تكنولوجيا الذكاء الاصطناعي. يتم الحصول على بيانات المتغيرات الضابطة من محطة ويند المالية، وقاعدة بيانات لجنة تنظيم الأوراق المالية الصينية (CSRC)، والبيانات المالية المعلنة من بورصتي شنغهاي وشنتشن، ومصادر أخرى ذات صلة. يتم تقديم الإحصائيات الوصفية لجميع المتغيرات في الجدول 3.

بيئة التجربة وإعداد المعلمات

(1) إعداد البيانات

(2) اختيار الميزات

(3) معالجة البيانات

(4) تدريب النموذج

تُستخدم دالة النواة

| اسم المتغير | حجم العينة | المتوسط | الانحراف المعياري | الحد الأدنى | الحد الأقصى |

| الذكاء الاصطناعي | 2788 | 3.54 | 1.09 | 1.69 | 5.29 |

| SDI | 2788 | 63.02 | 4.87 | 39.82 | 90.00 |

| ESG | 2788 | 68.26 | 5.38 | 36.26 | 92.39 |

| الحجم | 2788 | 22.13 | 1.31 | 19.18 | 26.54 |

| الرفع | 2788 | 0.41 | 0.19 | 0.053 | 0.93 |

| دوران الأصول | 2788 | 0.63 | 0.42 | 0 | 2.89 |

| RG | 2788 | 0.16 | 0.39 | -0.64 | 3.89 |

| Q توبين | 2788 | 1.98 | 1.29 | 0 | 10.67 |

تقييم الأداء

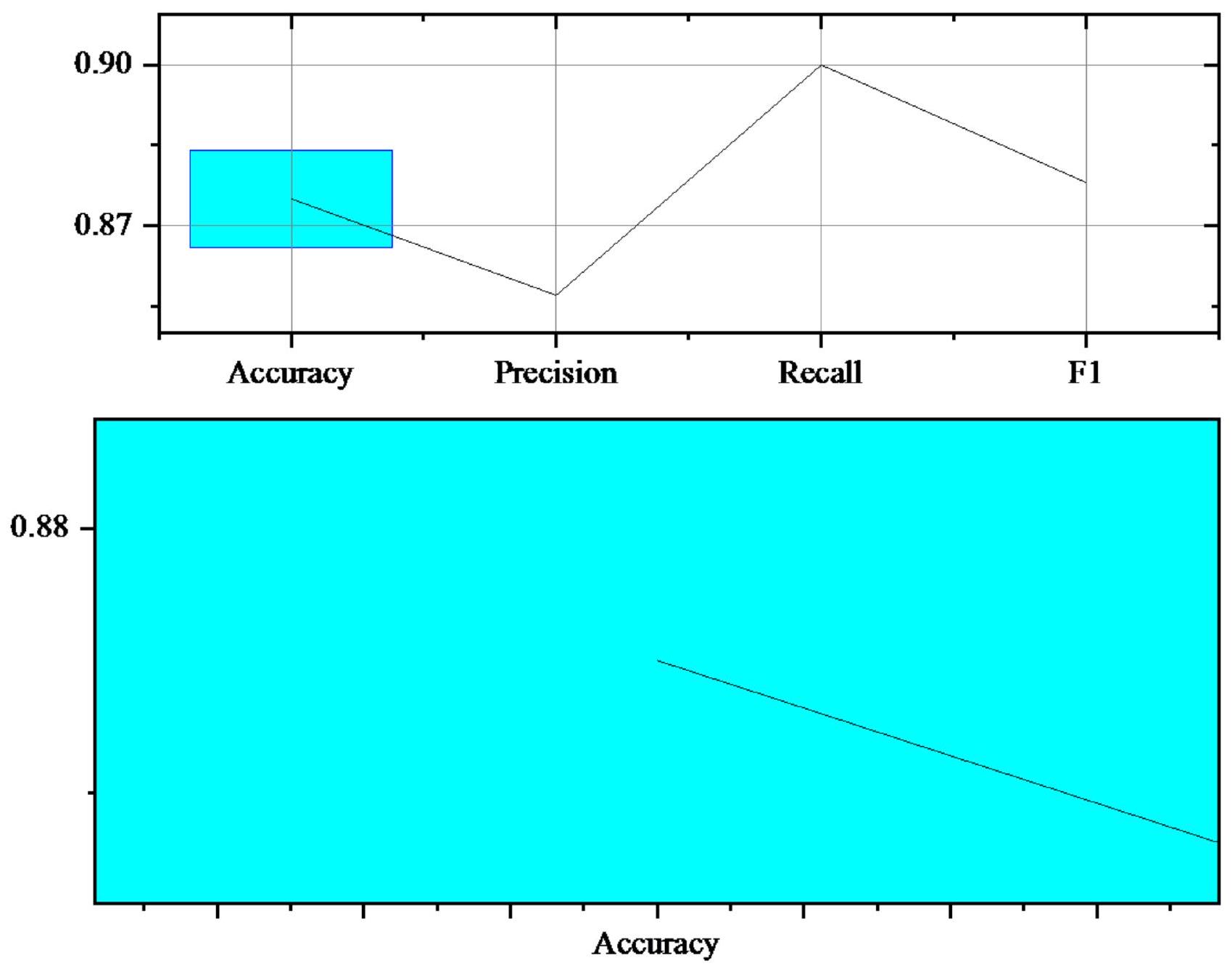

من التمثيل البياني، تبلغ درجة F1 للنموذج 0.878، مما يمثل المتوسط التوافقي للدقة والاسترجاع. توفر درجة F1 تقييمًا شاملاً من خلال تحقيق توازن بين الدقة والاسترجاع، مما يجعلها مناسبة بشكل خاص للسيناريوهات التي تتضمن بيانات غير متوازنة. في هذه الحالة، تشير درجة F1 البالغة 0.878 إلى أداء كفء للنموذج في التنبؤ بكل من الفئات الإيجابية والسلبية. بشكل عام، يظهر النموذج في هذا المثال أداءً قويًا في مهمة التنبؤ، يتميز بدقة عالية، ودقة، واسترجاع، ودرجة F1، مما يعكس تنبؤات دقيقة لكل من الفئات الإيجابية والسلبية ويشير إلى كفاءة تصنيف جديرة بالثناء.

(2) تخضع نتائج استبيان المسح لتحليل إحصائي، مع التركيز على الإحصائيات الوصفية للعينة وتحليل الفروق بين المجموعات. يتم توضيح النتائج الإحصائية الوصفية في الشكل 2A-C:

| الفئة الفعلية / الفئة المتوقعة | الفئة الإيجابية (1) | الفئة السلبية (0) |

| الفئة الإيجابية (1) | 90 | 10 |

| الفئة السلبية (0) | 15 | 85 |

| الدور | الإدارة العليا | الإدارة الوسطى | الموظفون في الخط الأمامي | الموظفون الفنيون |

| عدد المستجيبين | 7 | 26 | 109 | 58 |

| النسبة المئوية | 3.50% | 13.00% | 54.50% | 29.00% |

| أبعاد مختلفة | القيمة |

| قيمة t | -4.37 |

|

|

0.00002 |

| بعد ESG | اسم الشركة | محتوى تطبيق الذكاء الاصطناعي | نتائج التطبيق | وصف تحسين الأداء |

| بيئي | الشركة A | نظام مراقبة آلي، نظام إدارة طاقة ذكي | تقليل استهلاك الطاقة، تحسين معالجة مياه الصرف | انخفض استهلاك الطاقة بنسبة 10%، تم تقليل انبعاثات مياه الصرف بنسبة

|

| الشركة B | نظام إدارة موارد ذكي ومراقبة التلوث | تقليل انبعاثات الملوثات | تم تقليل الانبعاثات بنسبة 12%، تم تحسين نظام مراقبة تلوث الهواء، تحسن الأداء البيئي بنسبة 10% | |

| الشركة C | تقنية تحسين ذكية، تحسينات كفاءة الطاقة المدفوعة بالبيانات | توفير الطاقة وكفاءة الموارد | تم تقليل استهلاك الطاقة بنسبة 8%، زادت كفاءة استخدام الموارد بنسبة 13%، تحسن الأداء البيئي بنسبة 7% | |

| اجتماعي | الشركة D | نظام مراقبة صحة الموظفين الذكي | تحسين إدارة صحة وسلامة الموظفين | انخفضت إصابات العمل بنسبة

|

| الشركة E | منصة تحليل مزايا الموظفين المدفوعة بالذكاء الاصطناعي | تحسين رفاهية الموظفين وإدارة المسؤولية الاجتماعية | زادت مزايا الموظفين بنسبة 15%، تحسن رضا المسؤولية الاجتماعية بنسبة

|

|

| حوكمة | الشركة F | نموذج توقع المخاطر ونظام دعم القرار | تحسين شفافية القرار وإدارة المخاطر | زادت دقة تحذير المخاطر بنسبة

|

| الشركة G | نظام أتمتة التدقيق الداخلي وتوليد التقارير الذكية | تعزيز التدقيق الداخلي والشفافية | زادت تغطية التدقيق الداخلي بنسبة

|

| اسم المتغير | SDI | الذكاء الاصطناعي | ESG | الحجم | Lev | في | RG | نسبة توبين |

| SDI | 1 | |||||||

| الذكاء الاصطناعي | 0.072*** | 1 | ||||||

| البيئة والمجتمع والحوكمة | 0.239*** |

|

1 | |||||

| حجم | 0.007 |

|

|

1 | ||||

| ليف | -0.357*** |

|

-0.082*** |

|

1 | |||

| في | 0.203*** |

|

|

0.059*** |

|

1 | ||

| RG |

|

0.007 |

|

0.059*** | 0.033*** |

|

1 | |

| نسبة توبين | 0.179*** | 0.047*** |

|

|

-0.249*** | -0.007 | 0.073*** | 1 |

(3) تحليل الارتباط.

تقدم الجدول 8 نتائج تحليل الارتباط، كاشفًا عن العلاقات الخطية ومستويات الأهمية بين المتغيرات. يرتبط مؤشر التنمية المستدامة إيجابيًا مع كل من أداء الذكاء الاصطناعي وأداء البيئة والمجتمع والحوكمة، مع معاملات ارتباط تبلغ 0.072 و 0.239 على التوالي، وكلاهما ذو دلالة إحصائية عند

القدرات لتحقيق أداء أقوى في المجالات البيئية والاجتماعية والحوكمة. يظهر نسبة ليف ارتباطًا سلبيًا كبيرًا مع SDI وAI وESG، مما يعني أن مستويات الدين المرتفعة قد تعيق كل من التنمية المستدامة للشركات واعتماد تكنولوجيا الذكاء الاصطناعي. بالإضافة إلى ذلك، فإن إجمالي AT ومعدل RG مرتبطان إيجابيًا مع SDI، مع معاملات ارتباط تبلغ 0.203 و0.281 على التوالي. وهذا يشير إلى أن الاستخدام الفعال للأصول ونمو الدخل يعززان أداء التنمية المستدامة للشركات بشكل أفضل. يرتبط Q توبين إيجابيًا مع SDI وAI، ولكنه مرتبط سلبيًا مع أداء ESG (معامل الارتباط

(4) تحليل الانحدار.

(5) اختبار تأثير الوساطة لـ ESG.

تقدم الجدول 10 نتائج الانحدار لاختبار التأثير الوسيط، الذي يؤكد الدور الوسيط لـ ESG في العلاقة بين استخدام الذكاء الاصطناعي وSDI الشركات. في نموذج Path_a، معامل الانحدار لاستخدام الذكاء الاصطناعي على ESG هو 0.0007، وهو ذو دلالة إحصائية عند

| اسم المتغير | (1) SDI | (2) SDI | (3) SDI |

| الذكاء الاصطناعي | 0.002*** (11.02) | 0.002*** (11.06) | 0.001*** (6.22) |

| حجم | 0.018*** (42.74) | ||

| ليف | – 0.170*** (- 56.19) | ||

| في |

|

||

| RG | 0.040*** (25.86) | ||

| نسبة توبين | 0.010*** (21.73) | ||

| _cons | 0.022*** (11.80) | 0.012* (1.94) | – 0.350*** (- 33.89) |

| سنة | لا | نعم | نعم |

| صناعة | لا | نعم | نعم |

|

|

0.005 | 0.051 | 0.370 |

| اسم المتغير | (1) المسار_a | (2) المسار_b | (3) مسار_c |

| الذكاء الاصطناعي | 0.0007*** (5.21) | 0.204*** (16.77) | 0.0004** (2.76) |

| حجم | 0.017*** (45.14) | 1.491*** (44.63) |

|

| ليف | – 0.167*** (- 72.91) | – 6.237*** (- 30.62) | – 0.155*** (- 67.77) |

| في | 0.034*** (36.38) | 0.735*** (8.74) | 0.034*** (35.42) |

| RG |

|

– 0.227 (- 2.50) | 0.041 (41.12) |

| نسبة توبين | 0.0087*** (27.13) | – 0.086*** (- 3.01) | 0.0088*** (27.87) |

| _cons | – 0.336*** (- 36.52) | 39.47*** (47.93) | – 0.400*** (- 41.94) |

| ر

|

0.005 | 0.051 | 0.370 |

نقاش

الخاتمة

مساهمة البحث

حماية البيئة، لا سيما في مجالات مثل تحسين الموارد ومراقبة الانبعاثات. يُشجع مدراء الشركات على استغلال تقنية الذكاء الاصطناعي لتحسين الحوكمة المؤسسية وتعزيز مسؤوليتهم الاجتماعية، مما يحقق نتيجة متوازنة تفيد كل من الأداء الاقتصادي والمساهمات الاجتماعية.

الأعمال المستقبلية وقيود البحث

توفر البيانات

تم النشر عبر الإنترنت: 12 مارس 2025

References

- Aldoseri, A., Al-Khalifa, K. N. & Hamouda, A. M. Re-thinking data strategy and integration for artificial intelligence: Concepts, opportunities, and challenges. Appl. Sci. 13(12), 7082 (2023).

- Addy, W. A. et al. Predictive analytics in credit risk management for banks: A comprehensive review. GSC Adv. Res. Rev. 18(2), 434-449 (2024).

- Ibeh, C. V. et al. Business analytics and decision science: A review of techniques in strategic business decision making. World J. Adv. Res. Rev. 21(02), 1761-1769 (2024).

- Chen, P., Chu, Z. & Zhao, M. The road to corporate sustainability: The importance of artificial intelligence. Technol. Soc. 76, 102440 (2024).

- Chang, Y. L. & Ke, J. Socially responsible artificial intelligence empowered people analytics: A novel framework towards sustainability. Hum. Resour. Dev. Rev. 23(1), 88-120 (2024).

- Zhao, J. & Gómez, F. B. Artificial intelligence and sustainable decisions. Eur. Bus. Organ. Law Rev. 24(1), 1-39 (2023).

- Ye, J. et al. Investment on environmental social and governance activities and its impact on achieving sustainable development goals: Evidence from Chinese manufacturing firms. Econ. Res.-Ekonomska istraživanja 36(1), 333-356 (2023).

- Guo, Z. & He, Y. ESG and urban sustainable development. Trans. Econ. Bus. Manag. Res. 5, 250-265 (2024).

- Kozhabayev, H. et al. Possibilities of applying the Kaizen system for improving quality management in the context of ESG development. Calitatea 24(197), 24-34 (2023).

- Chung, R. K., Margolin, A. M. & Vyakina, I. V. Theory and practice of ESG transformation of management systems. Экономическая политика 18(2), 80-103 (2023).

- Oyewole, A. T. et al. Promoting sustainability in finance with AI: A review of current practices and future potential. World J. Adv. Res. Rev. 21(3), 590-607 (2024).

- Dmuchowski, P. et al. Environmental, social, and governance (ESG) model; impacts and sustainable investment-Global trends and Poland’s perspective. J. Environ. Manag. 329, 117023 (2023).

- Bhatti, U. A. et al. Artificial intelligence applications in reduction of carbon emissions: Step towards sustainable environment. Front. Environ. Sci. 11, 1183620 (2023).

- Allahham, M. et al. Big data analytics and AI for green supply chain integration and sustainability in hospitals. WSEAS Trans. Environ. Dev. 19, 1218-1230 (2023).

- Ositashvili, M. The compliance model as a catalyst for post-financial crisis efficiency in corporations. ESI Preprints 19, 150-150 (2023).

- Țîrcovnicu, G. I. & Hațegan, C. D. Integration of artificial intelligence in the risk management process: An analysis of opportunities and challenges. J. Financ. Stud. 8(15), 198-214 (2023).

- Farayola, O. A. & Olorunfemi, O. L. Ethical decision-making in IT governance: A review of models and frameworks. Int. J. Sci. Res. Arch. 11(2), 130-138 (2024).

- Hassan, M., Aziz, L. A. R. & Andriansyah, Y. The role artificial intelligence in modern banking: An exploration of AI-driven approaches for enhanced fraud prevention, risk management, and regulatory compliance. Rev. Contemp. Bus. Analyt. 6(1), 110132 (2023).

- Asif, M., Searcy, C. & Castka, P. ESG and Industry 5.0: The role of technologies in enhancing ESG disclosure. Technol. Forecast. Soc. Change 195, 122806 (2023).

- Minkkinen, M., Niukkanen, A. & Mäntymäki, M. What about investors? ESG analyses as tools for ethics-based AI auditing. AI Soc. 39(1), 329-343 (2024).

- De Villiers, C., Dimes, R. & Molinari, M. How will AI text generation and processing impact sustainability reporting? Critical analysis, a conceptual framework and avenues for future research. Sustain. Account. Manag. Policy J. 15(1), 96-118 (2024).

- Sadiq, M. et al. The role of environmental social and governance in achieving sustainable development goals: evidence from ASEAN countries. Econ. Res.-Ekonomska istraživanja 36(1), 170-190 (2023).

- Chien, F. The role of corporate governance and environmental and social responsibilities on the achievement of sustainable development goals in Malaysian logistic companies. Econ. Res.-Ekonomska istraživanja 36(1), 1610-1630 (2023).

- Xu, Y. & Zhu, N. The effect of environmental, social, and governance (ESG) performance on corporate financial performance in China: Based on the perspective of innovation and financial constraints. Sustainability 16(8), 3329 (2024).

- Rashid, A., Akmal, M. & Shah, S. M. A. R. Corporate governance and risk management in Islamic and convectional financial institutions: Explaining the role of institutional quality. J. Islam. Account. Bus. Res. 15(3), 466-498 (2024).

- Bekaert, G., Rothenberg, R. & Noguer, M. Sustainable investment: Exploring the linkage between alpha, ESG, and SDGs. Sustain. Dev. 31(5), 3831-3842 (2023).

- Doni, F. & Fiameni, M. Can innovation affect the relationship between environmental, social, and governance issues and financial performance? Empirical evidence from the STOXX200 index. Bus. Strategy Environ. 33(2), 546-574 (2024).

- Sætra, H. S. The AI ESG protocol: Evaluating and disclosing the environment, social, and governance implications of artificial intelligence capabilities, assets, and activities. Sustain. Dev. 31(2), 1027-1037 (2023).

- Wan, G. et al. Hotspots and trends of environmental, social and governance (ESG) research: A bibliometric analysis. Data Sci. Manag. 6(2), 65-75 (2023).

- David, L. K. et al. Environmental commitments and innovation in China’s corporate landscape: An analysis of ESG governance strategies. J. Environ. Manag. 349, 119529 (2024).

- Elahi, M. et al. A comprehensive literature review of the applications of AI techniques through the lifecycle of industrial equipment. Discov. Artif. Intell. 3(1), 43 (2023).

- Bharambe, U. et al. Synergies between natural language processing and swarm intelligence optimization: a comprehensive overview. In Advanced Machine Learning with Evolutionary and Metaheuristic Techniques 121-151 (Springer, 2024).

- Tchuente, D., Lonlac, J. & Kamsu-Foguem, B. A methodological and theoretical framework for implementing explainable artificial intelligence (XAI) in business applications. Comput. Ind. 155, 104044 (2024).

- Sharifani, K. & Amini, M. Machine learning and deep learning: A review of methods and applications. World Inf. Technol. Eng. J. 10(07), 3897-3904 (2023).

- Haluza, D. & Jungwirth, D. Artificial intelligence and ten societal megatrends: An exploratory study using GPT-3. Systems 11(3), 120 (2023).

- Bharadiya, J. P. A comparative study of business intelligence and artificial intelligence with big data analytics. Am. J. Artif. Intell. 7(1), 24 (2023).

- Aljohani, A. Predictive analytics and machine learning for real-time supply chain risk mitigation and agility. Sustainability15(20), 15088 (2023).

- Richey, R. G. Jr. et al. Artificial intelligence in logistics and supply chain management: A primer and roadmap for research. J. Bus. Logist. 44(4), 532-549 (2023).

- Bhima, B. et al. Enhancing organizational efficiency through the integration of artificial intelligence in management information systems. APTISI Trans. Manag. 7(3), 282-289 (2023).

- Lim, T. Environmental, social, and governance (ESG) and artificial intelligence in finance: State-of-the-art and research takeaways. Artif. Intell. Rev. 57(4), 1-64 (2024).

- Shi, X. K. & Zhang, Q. M. Understanding the mechanism of environmental, social, and governance impact on enterprise performance in the context of sustainable development. Corp. Soc. Responsib. Environ. Manag. 31(2), 784-800 (2024).

- Tse, T., Esposito, M. & Goh, D. The impact of artificial intelligence on environmental, social and governance investing: The case of Nexus FrontierTech. Int. J. Teach. Case Stud. 14(3), 256-275 (2024).

- Onyeaka, H. et al. Using artificial intelligence to tackle food waste and enhance the circular economy: Maximising resource efficiency and minimising environmental impact: A review. Sustainability 15(13), 10482 (2023).

- Hu, K. H. et al. Governance of artificial intelligence applications in a business audit via a fusion fuzzy multiple rule-based decisionmaking model. Financ. Innov. 9(1), 117 (2023).

- Nitlarp, T. & Mayakul, T. The implications of triple transformation on ESG in the energy sector: Fuzzy-set qualitative comparative analysis (fsQCA) and structural equation modeling (SEM) findings. Energies 16(5), 2090 (2023).

- Alqahtani, A. S. H. Application of artificial intelligence in carbon accounting and firm performance: A review using qualitative analysis. Int. J. Exp. Res. Rev 35, 138-148 (2023).

- Oh, H. J. et al. A preliminary study for developing perceived ESG scale to measure public perception toward organizations’ ESG performance. Public Relat. Rev. 50(1), 102398 (2024).

- Barbosa, A. S. et al. How can organizations measure the integration of environmental, social, and governance (ESG) criteria? Validation of an instrument using item response theory to capture workers’ perception. Bus. Strategy Environ. 33(4), 3607-3634 (2024).

- Murè, P. et al. “ESG score” vs. “ESG rating”: A conceptual model for the sustainability assessment and self-assessment of European SMEs. Front. Environ. Econ. 3, 1452416 (2024).

- Jing, H. & Zhang, S. The impact of artificial intelligence on ESG performance of manufacturing firms: The mediating role of ambidextrous green innovation. Systems 12(11), 499 (2024).

- Napitupulu, I. H. et al. Optimizing good corporate governance mechanism to improve performance: case in Indonesia’s manufacturing companies. Global Bus. Rev. 24(6), 1205-1226 (2023).

- Ogbeibu, S. et al. Demystifying the roles of organisational smart technology, artificial intelligence, robotics and algorithms capability: A strategy for green human resource management and environmental sustainability. Bus. Strategy Environ. 33(2), 369388 (2024).

- Lee, J. S., Deng, X. Y. & Chang, C. H. Examining the interactive effect of advertising investment and corporate social responsibility on financial performance. J. Risk Financ. Manag. 16(8), 362 (2023).

الشكر والتقدير

مساهمات المؤلف

الإعلانات

المصالح المتنافسة

الموافقة الأخلاقية

معلومات إضافية

معلومات إعادة الطبع والتصاريح متاحة على www.nature.com/reprints.

ملاحظة الناشر تظل Springer Nature محايدة فيما يتعلق بالمطالبات القضائية في الخرائط المنشورة والانتماءات المؤسسية.

© المؤلفون 2025

كلية الاقتصاد والإدارة، كلية جيانغشي المهنية للصناعة والهندسة، جيانغشي، الصين.

كلية الدراسات العليا للأعمال، جامعة UCSI، 56000 كوالالمبور، ماليزيا. جامعة آدمسون، 0900 مانيلا، الفلبين. البريد الإلكتروني: yupingxiao0312@163.com

DOI: https://doi.org/10.1038/s41598-025-93694-y

PMID: https://pubmed.ncbi.nlm.nih.gov/40074861

Publication Date: 2025-03-12

scientific reports

OPEN

The impact of artificial intelligencedriven ESG performance on sustainable development of central state-owned enterprises listed companies

Abstract

Yuping Xiao

Research background and motivations

Research objectives

Literature review

Overview of ESG performance and corporate sustainable development

Overview of the application of AI in ESG practices

monitoring and analysis of employee feedback and societal sentiments, enabling companies to promptly adjust their corporate social responsibility strategies

Overview of the analysis of AI-enhanced ESG practices from global and Chinese perspectives

Research gaps and hypotheses of the study

(1) According to the RBV theory, AI technology can assist enterprises in optimizing resource allocation and improving operational efficiency, particularly in the areas of environmental management, social responsibility, and corporate governance. For instance, AI can enhance a company’s effectiveness in resource utilization, emissions control, and other environmental areas through intelligent management systems, thereby improving environmental performance. The application of AI in employee management, health monitoring, and workplace safety can also strengthen the company’s performance in social responsibility. Moreover, AI’s role in risk management and decision support contributes to optimizing the company’s governance structure.

(2) AI technology, by driving transformation at various levels within enterprises, can not only improve ESG performance but also potentially contribute to an increase in corporate sustainable development performance. Sustainable development performance encompasses multiple aspects, including economic benefits, social responsibility, and environmental impact. By improving operational efficiency and optimizing resource allocation, AI technology may have a long-term effect on environmental, social, and governance outcomes.

(3) The relationships in Hypotheses 1 and 2 may not be solely direct and linear; corporate ESG performance may play a mediating role between the application of AI technology and corporate sustainable development performance. According to mediation effect theory, the application of AI technology, by enhancing a company’s performance in environmental, social, and governance domains, may indirectly influence its sustainable development outcomes. For example, strong ESG performance not only improves the company’s social image but may also enhance resource allocation efficiency, creating additional market opportunities and competitive advantages.

Research methodology

Qualitative research design

(1) In-depth Interviews: Conducting in-depth interviews with the management and key stakeholders of the enterprises to gather insights into their perspectives and experiences regarding the application of AI technology.

(2) Document Analysis: Analyzing annual reports, sustainability reports, and official announcements of the enterprises to obtain detailed information about the status of AI project implementation, resource allocation, and application outcomes.

Quantitative research design

| Dimension | Item no | Statement content | Strongly agree (5) | Agree (4) | Neutral (3) | Disagree (2) | Strongly disagree (1) |

| Corporate Governance | Q1 | The company’s decision-making process is transparent | |||||

| Q2 | The company utilizes AI technology for risk management | ||||||

| Q3 | The company strictly adheres to laws and regulations | ||||||

| Q4 | The board of directors is effective in overseeing company operations | ||||||

| Q5 | The company actively takes measures to enhance the efficiency of its governance structure | ||||||

| Environmental Protection | Q6 | The company uses AI technology to monitor and manage its environmental impact | |||||

| Q7 | AI technology has improved the company’s environmental performance | ||||||

| Q8 | The company utilizes AI technology to reduce waste and enhance resource efficiency | ||||||

| Q9 | The company employs AI technology for tracking and managing its carbon footprint and energy consumption | ||||||

| Q10 | The company’s policy enforcement regarding environmental protection is strong | ||||||

| Social Responsibility | Q11 | The company improves employee welfare through AI technology | |||||

| Q12 | The company performs well in community engagement and charitable activities | ||||||

| Q13 | The company utilizes AI technology to enhance the impact of its social responsibility initiatives | ||||||

| Q14 | The company ensures the fulfillment of social responsibility in supply chain management | ||||||

| Q15 | The company actively takes measures to enhance the transparency and effectiveness of its social contributions |

Construction of the regression model

| Variable type | Variable name | Symbol | Measurement method |

| Explanatory | AI usage | AI | Natural logarithm of term frequency + 1 |

| Dependent | Sustainable development performance | SDI | Measured using the SDI |

| Mediating | ESG performance | ESG | Huazheng ESG Index |

| Control | Company size | Size | Natural logarithm of total assets |

| Control | Leverage ratio | Lev | Total liabilities at year-end/total assets at year-end |

| Control | Asset turnover ratio | AT | Annual revenue/total assets |

| Control | Revenue growth rate | RG | Year-over-year growth in revenue |

| Control | Tobin’s Q | Tobin’s Q | (Market value of tradable shares + non-tradable shares * book value per share + book value of liabilities)/Total assets |

Experimental design and performance evaluation

Datasets collection

(1) Industry Representation

(2) ESG Performance Level

(3) Degree of AI Application

(4) Data Accessibility

reports. The frequency of AI-related terms is calculated to construct a quantitative indicator of AI technology usage. Control variable data is sourced from the Wind Financial Terminal, the China Securities Regulatory Commission (CSRC) database, financial statements disclosed by the Shanghai and Shenzhen stock exchanges, and other relevant sources. Descriptive statistics for all variables are provided in Table 3.

Experimental environment and parameters setting

(1) Data Preparation

(2) Feature Selection

(3) Data Preprocessing

(4) Model Training

The kernel function

| Variable name | Sample size | Mean | Standard deviation | Minimum | Maximum |

| AI | 2788 | 3.54 | 1.09 | 1.69 | 5.29 |

| SDI | 2788 | 63.02 | 4.87 | 39.82 | 90.00 |

| ESG | 2788 | 68.26 | 5.38 | 36.26 | 92.39 |

| Size | 2788 | 22.13 | 1.31 | 19.18 | 26.54 |

| Lev | 2788 | 0.41 | 0.19 | 0.053 | 0.93 |

| AT | 2788 | 0.63 | 0.42 | 0 | 2.89 |

| RG | 2788 | 0.16 | 0.39 | -0.64 | 3.89 |

| Tobin’s Q | 2788 | 1.98 | 1.29 | 0 | 10.67 |

Performance evaluation

From the graphical representation, the model’s F1 score stands at 0.878 , representing the harmonic mean of precision and recall. The F1 score offers a comprehensive assessment by balancing precision and recall, making it particularly suitable for scenarios involving imbalanced data. In this instance, an F1 score of 0.878 indicates proficient performance of the model in predicting both positive and negative classes. Overall, the model in this example demonstrates robust performance in the prediction task, characterized by high accuracy, precision, recall, and F1 score, thereby showcasing accurate predictions for both positive and negative classes and indicating commendable classification proficiency.

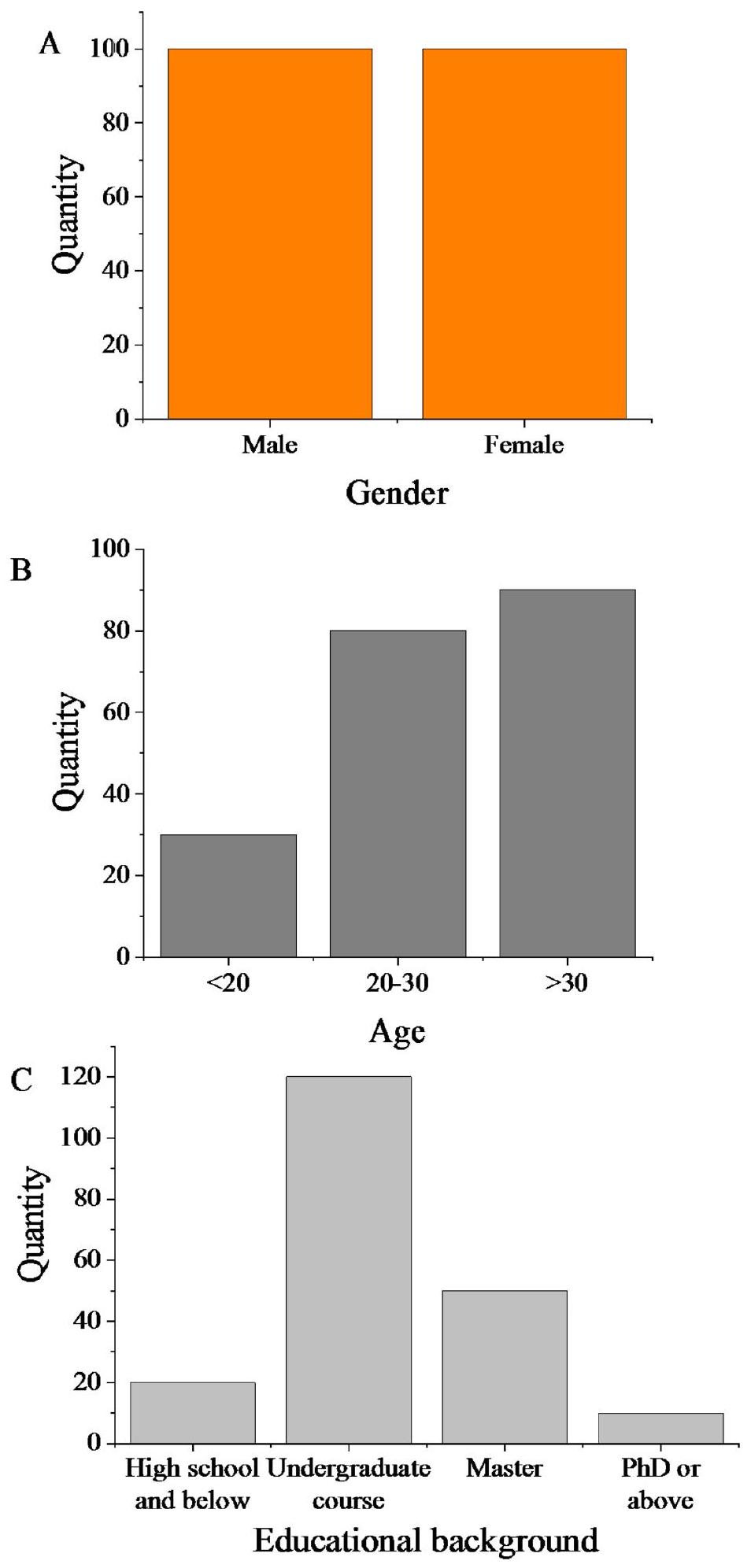

(2) The results of the questionnaire survey are subjected to statistical analysis, with an emphasis on descriptive statistics of the sample and an analysis of group differences. The descriptive statistical findings are illustrated in Fig. 2A-C:

| Actual category/predicted category | Positive category (1) | Negative category (0) |

| Positive category (1) | 90 | 10 |

| Negative category (0) | 15 | 85 |

| Role | Senior management | Middle management | Frontline employees | Technical staff |

| Number of respondents | 7 | 26 | 109 | 58 |

| Percentage | 3.50% | 13.00% | 54.50% | 29.00% |

| Different dimensions | Value |

| t -value | -4.37 |

|

|

0.00002 |

| ESG dimension | Company name | AI application content | Application outcomes | Performance improvement description |

| Environmental | Company A | Automated monitoring system, intelligent energy management system | Reduced energy consumption, optimized wastewater treatment | Energy consumption decreased by 10%, wastewater emissions reduced by

|

| Company B | Intelligent resource management and pollution control system | Reduced pollutant emissions | Emissions reduced by 12%, air pollution control system optimized, environmental performance improved by 10% | |

| Company C | Smart optimization technology, datadriven energy efficiency improvements | Energy saving and resource efficiency | Energy consumption reduced by 8%, resource utilization increased by 13%, environmental performance improved by 7% | |

| Social | Company D | Intelligent employee health monitoring system | Enhanced employee health management and safety | Workplace injuries decreased by

|

| Company E | AI-driven employee benefits analysis platform | Improved employee welfare and social responsibility management | Employee benefits increased by 15%, social responsibility satisfaction improved by

|

|

| Governance | Company F | Risk prediction model and decision support system | Improved decision transparency and risk management | Risk warning accuracy increased by

|

| Company G | Internal audit automation system and intelligent report generation | Strengthened internal audit and transparency | Internal audit coverage increased by

|

| Variable name | SDI | AI | ESG | Size | Lev | AT | RG | Tobin’s Q |

| SDI | 1 | |||||||

| AI | 0.072*** | 1 | ||||||

| ESG | 0.239*** |

|

1 | |||||

| Size | 0.007 |

|

|

1 | ||||

| Lev | -0.357*** |

|

-0.082*** |

|

1 | |||

| AT | 0.203*** |

|

|

0.059*** |

|

1 | ||

| RG |

|

0.007 |

|

0.059*** | 0.033*** |

|

1 | |

| Tobin’s Q | 0.179*** | 0.047*** |

|

|

-0.249*** | -0.007 | 0.073*** | 1 |

(3) Correlation Analysis.

Table 8 presents the correlation analysis results, revealing the linear relationships and significance levels between the variables. SDI is positively correlated with both AI and ESG performance, with correlation coefficients of 0.072 and 0.239 , respectively, both significant at the

capabilities to achieve stronger performance in environmental, social, and governance areas. The Lev ratio shows a significant negative correlation with SDI, AI, and ESG, implying that higher debt levels may hinder both corporate sustainable development and the adoption of AI technology. Additionally, total AT and RG rate are positively correlated with SDI, with correlation coefficients of 0.203 and 0.281 , respectively. This suggests that efficient asset utilization and income growth foster better corporate sustainable development performance. Tobin’s Q is positively correlated with SDI and AI, but negatively correlated with ESG performance (correlation coefficient

(4) Regression Analysis.

(5) ESG Mediating Effect Test.

Table 10 presents the regression results for the mediating effect test, which confirms the mediating role of ESG in the relationship between AI usage and corporate SDI. In Model Path_a, the regression coefficient for AI on ESG is 0.0007 , significant at the

| Variable name | (1) SDI | (2) SDI | (3) SDI |

| AI | 0.002*** (11.02) | 0.002*** (11.06) | 0.001*** (6.22) |

| Size | 0.018*** (42.74) | ||

| Lev | – 0.170*** (- 56.19) | ||

| AT |

|

||

| RG | 0.040*** (25.86) | ||

| Tobin’s Q | 0.010*** (21.73) | ||

| _cons | 0.022*** (11.80) | 0.012* (1.94) | – 0.350*** (- 33.89) |

| Year | No | Yes | Yes |

| Industry | No | Yes | Yes |

|

|

0.005 | 0.051 | 0.370 |

| Variable name | (1) Path_a | (2) Path_b | (3) Path_c |

| AI | 0.0007*** (5.21) | 0.204*** (16.77) | 0.0004** (2.76) |

| Size | 0.017*** (45.14) | 1.491*** (44.63) |

|

| Lev | – 0.167*** (- 72.91) | – 6.237*** (- 30.62) | – 0.155*** (- 67.77) |

| AT | 0.034*** (36.38) | 0.735*** (8.74) | 0.034*** (35.42) |

| RG |

|

– 0.227 (- 2.50) | 0.041 (41.12) |

| Tobin’s Q | 0.0087*** (27.13) | – 0.086*** (- 3.01) | 0.0088*** (27.87) |

| _cons | – 0.336*** (- 36.52) | 39.47*** (47.93) | – 0.400*** (- 41.94) |

| R

|

0.005 | 0.051 | 0.370 |

Discussion

Conclusion

Research contribution

environmental protection, particularly in areas such as resource optimization and emissions control. Corporate managers are encouraged to leverage AI technology to improve corporate governance and enhance their social responsibility, thereby achieving a balanced outcome that benefits both economic performance and societal contributions.

Future works and research limitations

Data availability

Published online: 12 March 2025

References

- Aldoseri, A., Al-Khalifa, K. N. & Hamouda, A. M. Re-thinking data strategy and integration for artificial intelligence: Concepts, opportunities, and challenges. Appl. Sci. 13(12), 7082 (2023).

- Addy, W. A. et al. Predictive analytics in credit risk management for banks: A comprehensive review. GSC Adv. Res. Rev. 18(2), 434-449 (2024).

- Ibeh, C. V. et al. Business analytics and decision science: A review of techniques in strategic business decision making. World J. Adv. Res. Rev. 21(02), 1761-1769 (2024).

- Chen, P., Chu, Z. & Zhao, M. The road to corporate sustainability: The importance of artificial intelligence. Technol. Soc. 76, 102440 (2024).

- Chang, Y. L. & Ke, J. Socially responsible artificial intelligence empowered people analytics: A novel framework towards sustainability. Hum. Resour. Dev. Rev. 23(1), 88-120 (2024).

- Zhao, J. & Gómez, F. B. Artificial intelligence and sustainable decisions. Eur. Bus. Organ. Law Rev. 24(1), 1-39 (2023).

- Ye, J. et al. Investment on environmental social and governance activities and its impact on achieving sustainable development goals: Evidence from Chinese manufacturing firms. Econ. Res.-Ekonomska istraživanja 36(1), 333-356 (2023).

- Guo, Z. & He, Y. ESG and urban sustainable development. Trans. Econ. Bus. Manag. Res. 5, 250-265 (2024).

- Kozhabayev, H. et al. Possibilities of applying the Kaizen system for improving quality management in the context of ESG development. Calitatea 24(197), 24-34 (2023).

- Chung, R. K., Margolin, A. M. & Vyakina, I. V. Theory and practice of ESG transformation of management systems. Экономическая политика 18(2), 80-103 (2023).

- Oyewole, A. T. et al. Promoting sustainability in finance with AI: A review of current practices and future potential. World J. Adv. Res. Rev. 21(3), 590-607 (2024).

- Dmuchowski, P. et al. Environmental, social, and governance (ESG) model; impacts and sustainable investment-Global trends and Poland’s perspective. J. Environ. Manag. 329, 117023 (2023).

- Bhatti, U. A. et al. Artificial intelligence applications in reduction of carbon emissions: Step towards sustainable environment. Front. Environ. Sci. 11, 1183620 (2023).

- Allahham, M. et al. Big data analytics and AI for green supply chain integration and sustainability in hospitals. WSEAS Trans. Environ. Dev. 19, 1218-1230 (2023).

- Ositashvili, M. The compliance model as a catalyst for post-financial crisis efficiency in corporations. ESI Preprints 19, 150-150 (2023).

- Țîrcovnicu, G. I. & Hațegan, C. D. Integration of artificial intelligence in the risk management process: An analysis of opportunities and challenges. J. Financ. Stud. 8(15), 198-214 (2023).

- Farayola, O. A. & Olorunfemi, O. L. Ethical decision-making in IT governance: A review of models and frameworks. Int. J. Sci. Res. Arch. 11(2), 130-138 (2024).

- Hassan, M., Aziz, L. A. R. & Andriansyah, Y. The role artificial intelligence in modern banking: An exploration of AI-driven approaches for enhanced fraud prevention, risk management, and regulatory compliance. Rev. Contemp. Bus. Analyt. 6(1), 110132 (2023).

- Asif, M., Searcy, C. & Castka, P. ESG and Industry 5.0: The role of technologies in enhancing ESG disclosure. Technol. Forecast. Soc. Change 195, 122806 (2023).

- Minkkinen, M., Niukkanen, A. & Mäntymäki, M. What about investors? ESG analyses as tools for ethics-based AI auditing. AI Soc. 39(1), 329-343 (2024).

- De Villiers, C., Dimes, R. & Molinari, M. How will AI text generation and processing impact sustainability reporting? Critical analysis, a conceptual framework and avenues for future research. Sustain. Account. Manag. Policy J. 15(1), 96-118 (2024).

- Sadiq, M. et al. The role of environmental social and governance in achieving sustainable development goals: evidence from ASEAN countries. Econ. Res.-Ekonomska istraživanja 36(1), 170-190 (2023).

- Chien, F. The role of corporate governance and environmental and social responsibilities on the achievement of sustainable development goals in Malaysian logistic companies. Econ. Res.-Ekonomska istraživanja 36(1), 1610-1630 (2023).

- Xu, Y. & Zhu, N. The effect of environmental, social, and governance (ESG) performance on corporate financial performance in China: Based on the perspective of innovation and financial constraints. Sustainability 16(8), 3329 (2024).

- Rashid, A., Akmal, M. & Shah, S. M. A. R. Corporate governance and risk management in Islamic and convectional financial institutions: Explaining the role of institutional quality. J. Islam. Account. Bus. Res. 15(3), 466-498 (2024).

- Bekaert, G., Rothenberg, R. & Noguer, M. Sustainable investment: Exploring the linkage between alpha, ESG, and SDGs. Sustain. Dev. 31(5), 3831-3842 (2023).

- Doni, F. & Fiameni, M. Can innovation affect the relationship between environmental, social, and governance issues and financial performance? Empirical evidence from the STOXX200 index. Bus. Strategy Environ. 33(2), 546-574 (2024).

- Sætra, H. S. The AI ESG protocol: Evaluating and disclosing the environment, social, and governance implications of artificial intelligence capabilities, assets, and activities. Sustain. Dev. 31(2), 1027-1037 (2023).

- Wan, G. et al. Hotspots and trends of environmental, social and governance (ESG) research: A bibliometric analysis. Data Sci. Manag. 6(2), 65-75 (2023).

- David, L. K. et al. Environmental commitments and innovation in China’s corporate landscape: An analysis of ESG governance strategies. J. Environ. Manag. 349, 119529 (2024).

- Elahi, M. et al. A comprehensive literature review of the applications of AI techniques through the lifecycle of industrial equipment. Discov. Artif. Intell. 3(1), 43 (2023).

- Bharambe, U. et al. Synergies between natural language processing and swarm intelligence optimization: a comprehensive overview. In Advanced Machine Learning with Evolutionary and Metaheuristic Techniques 121-151 (Springer, 2024).

- Tchuente, D., Lonlac, J. & Kamsu-Foguem, B. A methodological and theoretical framework for implementing explainable artificial intelligence (XAI) in business applications. Comput. Ind. 155, 104044 (2024).

- Sharifani, K. & Amini, M. Machine learning and deep learning: A review of methods and applications. World Inf. Technol. Eng. J. 10(07), 3897-3904 (2023).

- Haluza, D. & Jungwirth, D. Artificial intelligence and ten societal megatrends: An exploratory study using GPT-3. Systems 11(3), 120 (2023).

- Bharadiya, J. P. A comparative study of business intelligence and artificial intelligence with big data analytics. Am. J. Artif. Intell. 7(1), 24 (2023).

- Aljohani, A. Predictive analytics and machine learning for real-time supply chain risk mitigation and agility. Sustainability15(20), 15088 (2023).

- Richey, R. G. Jr. et al. Artificial intelligence in logistics and supply chain management: A primer and roadmap for research. J. Bus. Logist. 44(4), 532-549 (2023).

- Bhima, B. et al. Enhancing organizational efficiency through the integration of artificial intelligence in management information systems. APTISI Trans. Manag. 7(3), 282-289 (2023).

- Lim, T. Environmental, social, and governance (ESG) and artificial intelligence in finance: State-of-the-art and research takeaways. Artif. Intell. Rev. 57(4), 1-64 (2024).

- Shi, X. K. & Zhang, Q. M. Understanding the mechanism of environmental, social, and governance impact on enterprise performance in the context of sustainable development. Corp. Soc. Responsib. Environ. Manag. 31(2), 784-800 (2024).

- Tse, T., Esposito, M. & Goh, D. The impact of artificial intelligence on environmental, social and governance investing: The case of Nexus FrontierTech. Int. J. Teach. Case Stud. 14(3), 256-275 (2024).

- Onyeaka, H. et al. Using artificial intelligence to tackle food waste and enhance the circular economy: Maximising resource efficiency and minimising environmental impact: A review. Sustainability 15(13), 10482 (2023).

- Hu, K. H. et al. Governance of artificial intelligence applications in a business audit via a fusion fuzzy multiple rule-based decisionmaking model. Financ. Innov. 9(1), 117 (2023).

- Nitlarp, T. & Mayakul, T. The implications of triple transformation on ESG in the energy sector: Fuzzy-set qualitative comparative analysis (fsQCA) and structural equation modeling (SEM) findings. Energies 16(5), 2090 (2023).

- Alqahtani, A. S. H. Application of artificial intelligence in carbon accounting and firm performance: A review using qualitative analysis. Int. J. Exp. Res. Rev 35, 138-148 (2023).

- Oh, H. J. et al. A preliminary study for developing perceived ESG scale to measure public perception toward organizations’ ESG performance. Public Relat. Rev. 50(1), 102398 (2024).

- Barbosa, A. S. et al. How can organizations measure the integration of environmental, social, and governance (ESG) criteria? Validation of an instrument using item response theory to capture workers’ perception. Bus. Strategy Environ. 33(4), 3607-3634 (2024).

- Murè, P. et al. “ESG score” vs. “ESG rating”: A conceptual model for the sustainability assessment and self-assessment of European SMEs. Front. Environ. Econ. 3, 1452416 (2024).

- Jing, H. & Zhang, S. The impact of artificial intelligence on ESG performance of manufacturing firms: The mediating role of ambidextrous green innovation. Systems 12(11), 499 (2024).

- Napitupulu, I. H. et al. Optimizing good corporate governance mechanism to improve performance: case in Indonesia’s manufacturing companies. Global Bus. Rev. 24(6), 1205-1226 (2023).

- Ogbeibu, S. et al. Demystifying the roles of organisational smart technology, artificial intelligence, robotics and algorithms capability: A strategy for green human resource management and environmental sustainability. Bus. Strategy Environ. 33(2), 369388 (2024).

- Lee, J. S., Deng, X. Y. & Chang, C. H. Examining the interactive effect of advertising investment and corporate social responsibility on financial performance. J. Risk Financ. Manag. 16(8), 362 (2023).

Acknowledgements

Author contributions

Declarations

Competing interests

Ethical approval

Additional information

Reprints and permissions information is available at www.nature.com/reprints.

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

© The Author(s) 2025

School of Economics and Management, Jiangxi Vocational College of Industry & Engineering, Jiangxi, China.

Graduate Business School, UCSI University, 56000 Kuala Lumpur, Malaysia. Adamson University, 0900 Manila, Philippines. email: yupingxiao0312@163.com